Headlines:

- Gas and Electricity Wholesale costs move higher with colder temperatures

- EU Gas Storage levels are a high 91% full.

- Still potential price volatility should there be further supply issues

Energy Overview

As of the 7th of December, Gas and Electricity Year Ahead Wholesale costs were higher, when compared to last month’s report.

Oil is lower at $79 per barrel, from $94, despite OPEC+ taking measures to keep the price inflated. The $60 price cap imposed on Russian Oil exports and a slowing economic growth forecast, are contributing factors.

Large numbers of LNG shipments continue to arrive in Europe, which has helped the EU maintain a high level of Gas Storage. There have also been efforts to reduce consumption and source supplies from elsewhere, due to the closure on Nord Stream 1 and 2 from Russia. The recent upturn in Gas costs is largely the result of colder temperatures and an increase in demand. The Met Office forecast suggests very cold spells for periods in December, with wintry showers and overnight frosts, but the possibility of a return to seasonal norm conditions towards the end of the month.

Electricity generation costs have moved higher due to the use of expensive Gas and the reduced contribution of Wind. The UK like other nations is exploring a number of solutions to avoid power shortages through the winter, including standby Coal generation, specifically to meet peak demand. Imports from France will be less likely due to large numbers of their Nuclear reactors being offline.

What does this mean for me?

The government’s, Energy Bill Relief Scheme, is providing assistance for non-domestic customers from Oct 2022 until March 2023, and being reviewed, with the option to extend it for targeted industries. This means that companies will not be fully exposed to the very high winter prices. If a contract was entered from December 2021 (previously April 2022), a Wholesale price cap of 21.1 p/kWh for Electricity and 7.5 p/kWh for Gas will be applied. The key point is that this is just Wholesale and so all other charges that make up an energy bill will be added. Those that are not contracted during the six months and choose to be exposed to supplier’s non contracted rates, will receive a Maximum Discount from the Wholesale cost of 34.5 p/kWh and 9.1 p/kWh. This could mean that the price paid is greater than that of the price cap. Energy suppliers are updating their billing to automatically incorporate these changes. The advice being given is to contract for this period and also look at contract options from April 2023.

Over the next year, the way some charges are calculated will change, under the Targeted Charging Review. Energy suppliers can choose whether to fix Electricity contract costs, pass them through or leave that decision until a later date. This does allow for the possibility of a review of the Transmission and Balancing charges in some fixed price Electricity contracts, as the pricing method is due to change from April 2023.

Indigo Swan will be working closely with energy suppliers to best help all our customers through this worrying time.

Please contact us on 0333 320 0475 to discuss options or to get a latest update.

Gas market overview

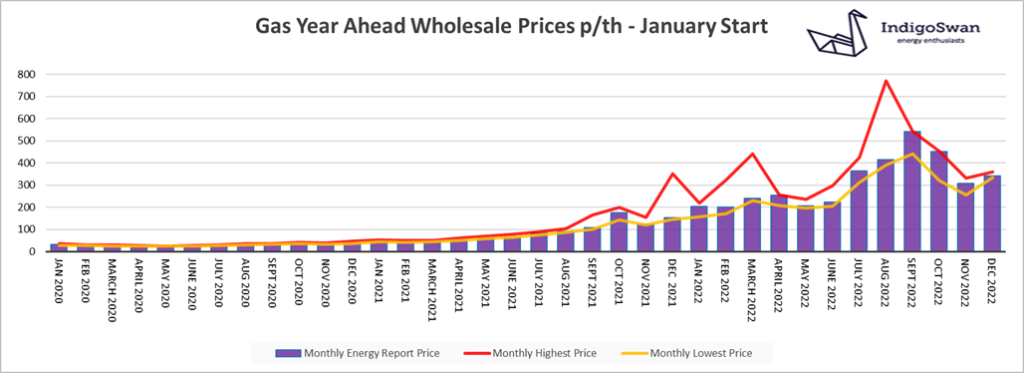

On the 7th of December, the Gas Year Ahead Wholesale cost was 342.48p/th, up from 307.61p/th in last month’s report and 124% higher than 2021. Prices for 2023 and 2024 are lower.

Although prices are still high, they are considerably lower than the peaks earlier in the year when there were concerns for Gas supplies through the winter. The initial higher target for EU Gas Storage was set at 85% full for November, with the assumption that cold temperatures would then start to drain stocks. At this time, they are 91% full, which provides markets with a degree of confidence that we will not see significant shortages. This has been achieved through energy saving measures and the sourcing of Gas at a considerable cost from around the world. LNG deliveries are high with more due in December, some of which will head towards Germany’s first LNG terminal, further removing their reliance on piped Russian Gas.

The UK has a very low Gas Storage capacity, but we have partially opened Rough for use this winter. Even when this is fully available, we will still be far behind other major European countries, which adds an element of volatility when temperatures fall and Gas demand increases.

The contribution of Gas for generation increased in November to 40% from 39% in October, although a lower Wind contribution so far in December has seen this rise to 46%, adding a burden to Gas supplies.

Let us know if you would like us to research your options for 12, 24 and 36 month contracts.

Electricity market overview

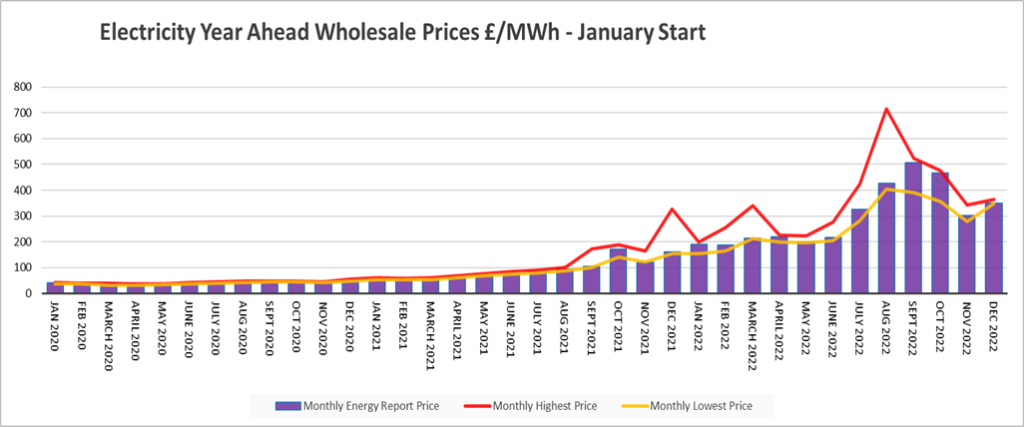

On the 7th of December, the Electricity Year Ahead Wholesale cost was £348.62/MWh, up from £301.24/MWh in last month’s report and 118% higher than 2021. Prices for 2023 and 2024 are lower.

Electricity prices closely follow Gas due to it being the main source of generation, although Gas only accounted for 40% in November, lower than the period April – September. However, a low Wind contribution over the last week of 21%, has seen the increased use of Gas at 46% and Coal in the region of 4%, adding pressure to Electricity prices.

The National Grid has mechanisms in place to help avoid power shortages and has taken additional steps to make Coal generation available on demand. These measures do come at a cost premium, in the form of higher third-party charges within bills, but provide an element of stability to prices which otherwise may react even more dramatically.

Unlike previous years there is doubt that we can rely on Electricity imports from the continent at times of peak demand, due to their own generation concerns, the main one being large numbers of offline French Nuclear reactors. Despite this, the message from the authorities remains one of optimism, that we will avoid any issues this winter, by carefully managing tools and resources.

Let us know if you would like us to research your options for 12, 24 and 36 month contracts.

If you enjoyed reading this blog why not try on of our others: