Headlines:

- Gas and Electricity Wholesale prices are lower than last month

- Prices are increasing today due to renewed military strikes

- Pressure on prices as disruption to Oil and LNG supplies continue

Energy Overview

As of the 4th of May, Gas and Electricity Year Ahead Wholesale costs were lower than last month. Oil was also lower at $114 from $118. In April the UAE announced they are leaving OPEC, to avoid restrictions on their Oil production.

Today, Gas prices are moving higher as both the US and Iran have carried out strikes. The US against Iranian military boats, and Iran against their neighbours and shipping.

Over the last month energy costs eased due to the ceasefire and hopes that negotiations could end the conflict, but there appears to be significant areas of disagreement. The US seems hesitant to carry out threats of more attacks against Iran’s energy and wider infrastructure, due to the impact on civilians and energy prices. This has created a stalemate where the Strait of Hormuz is still effectively closed, despite US attempts to escort ships and blockading Iran’s ports. This means continued disruption to about 20% of global Oil and LNG. Markets prices are increasing again as buyers of energy from the Middle East look to secure deliveries from other sources.

The effect on customer’s contract renewals is currently significant when compared to more recent prices, although they are still far lower than we saw in 2022 and 2023. The eventual scale of these increases and over what period is very much an unknown, but we will continue to be available to discuss options and provide guidance.

Other Industry Costs

The energy industry has changed how it recovers Electricity Distribution, Transmission and Balancing costs, under the Targeted Charging Review. This has moved some charges away from being based on the energy used and billed in the unit rate, to fixed charges incorporated within the Standing Charge or as separate items. This should give both the customer and the industry a more accurate way of calculating budgets, but the change has become noticeable within energy bills and created concern.

From April 2026 customers will have seen a large increase in Transmission costs with an expectation of further annual increases at least for the next five years. Distribution costs are a little more complicated, made up of Time of Use, Available Capacity and Fixed charges. Some of these charges are now based on a meter’s Band, which is related to a Half Hourly meter’s kVA Capacity. This means that by managing demand and reviewing the Capacity, there is an opportunity to reduce costs. Indigo Swan can provide you with guidance through this process.

The cost to Balance the network is increasing as is the Energy Intensive Industries (EII) charge, which provides relief from various industry costs for EII customers. This moves from 60% to 90% for the Network costs from April 2026.

Indigo Swan works closely with energy suppliers to help all our customers understand and manage changes.

Please contact us on 0333 320 0475 to discuss options or to get a latest update.

Gas Market Overview

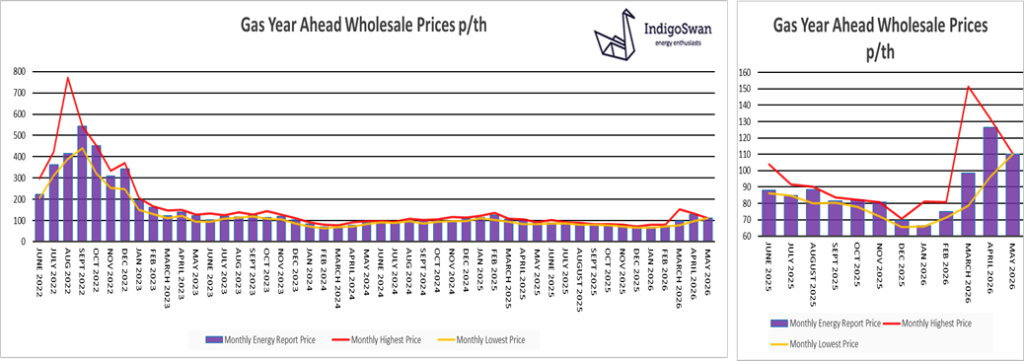

On the 4th of May, the Gas Year Ahead Wholesale cost was 110.15p/th, down from 126.58p/th in last month’s report and 24% higher than 2025. Today, the 5th of May, is seeing prices move higher as attacks by the US and Iran have resumed.

The extension of the ceasefire and negotiations meant that costs fell for much of April, with the realisation that military strikes were unlikely to end the war but continue to push energy prices higher. Even when the conflict does end, there will still be supply issues due to the damage sustained to Oil and LNG facilities.

The EU’s Gas Storage is just 34% full compared to 41% in 2025 and 63% in 2024. As LNG supplies from the Middle East have been impacted, which typically head to Asia, demand has increased from other sources. This could mean that the EU struggles to replace Gas for use in winter 2026/2027 due to high demand and costs, with the added concern that they have already banned some Russian LNG deliveries, with a complete ban due from January 2027. This will likely create a price pressure through the summer, hoping that there are no supply issues from our main Gas suppliers, Norway and the US.

We would encourage any customer with a contract that ends in the next few months, to discuss your renewals with us and we will look to provide additional market intelligence, guidance and support as required.

Electricity Market Overview

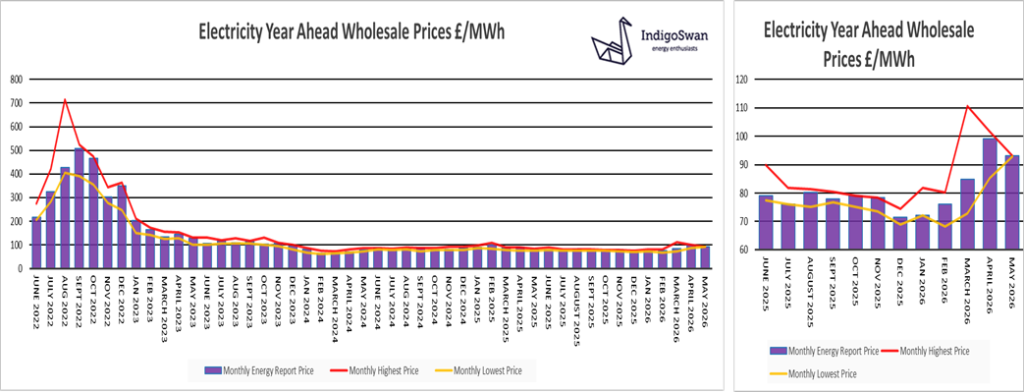

On the 4th of May, the Electricity Year Ahead Wholesale cost was £93.12/MWh, down from £99.24/MWh in last month’s report and 16% higher than 2025. Today, the 5th of May, is seeing prices move higher as attacks by the US and Iran have resumed.

With the UK’s Electricity Wholesale prices tracking the direction of Gas, due to its high cost and use for generation, the conflict in the Middle East continues be a significant influence. Global Gas costs are increasing once again as the Strait of Hormuz is effectively closed due to fear of attacks by Iran, despite the US attempt to escort ships. The low EU Gas Storage levels and concern for supplies through winter 2026/2027 are impacting on Electricity prices.

In April the UK government announced plans to pressure some generation that benefits from the high market prices, onto other schemes or agreements, in order to lower costs for consumers. In April, Wind accounted for 26% of supplies and Gas 17%, down from 24% in March. The Interconnectors with mainland Europe, which allow both Imports and Exports, provided 16%.

We would encourage any customer with a contract that ends in the next few months, to discuss your renewals with us and we will look to provide additional market intelligence, guidance and support as required.

If you enjoyed reading this blog why not try one of our others: