Headlines:

- Gas and Electricity Wholesale prices are lower than last month

- Little progression in the peace talks between the US and Iran

- EU Gas Storage remains a low 50% full

Energy Overview

As of the 6th of July, Gas and Electricity Year Ahead Wholesale costs were lower than last month. Oil was lower at $72 from $94.

As of the 7th of July, prices are increasing with reports of another attack on shipping in the Strait of Hormuz.

In recent weeks, Gas Wholesale costs have generally shown little direction, after the initial reductions when the peace deal between the US and Iran was announced.

Wholesale prices for the year starting August 2026 are higher than before the conflict but are much lower than during the early stages of the war between Russia and Ukraine.

Gas and Electricity Wholesale prices further out are showing much better value, potentially providing an opportunity to dilute costs with longer-term energy contracts.

Other Industry Costs

April 2026 saw a large increase in Electricity Transmission costs with an expectation of further annual increases. Distribution costs are a little more complicated, made up of Time of Use, Available Capacity and Fixed charges. Some of these charges are now based on a meter’s Band, which is related to a Half Hourly meter’s kVA Capacity. This means that by managing demand and reviewing the Capacity, there is an opportunity to reduce costs. Indigo Swan can provide you with guidance through this process.

The cost to Balance the network is increasing as is the Energy Intensive Industries (EII) charge, which provides relief from various industry costs for EII customers. This moved from 60% to 90% for the Network costs from April 2026.

Please contact us on 0333 320 0475 to discuss options or to get a latest update.

Gas Market Overview

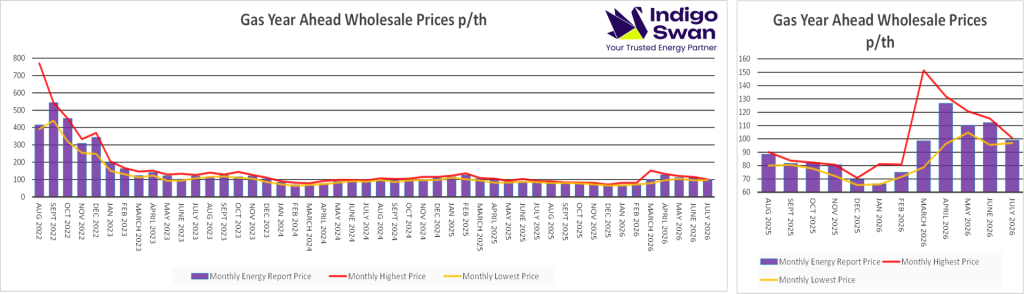

On the 6th of July, the Gas Year Ahead Wholesale cost was 98.87p/th, down from 112.07p/th in last month’s report and 17% higher than 2025.

Today, the 7th of July, is seeing prices move higher following reports of another attack on shipping through the Strait of Hormuz.

The peace deal between the US and Iran is holding, despite some military activity and the ongoing threat of attacks against Oil and LNG shipments.

LNG Exports from the region have been lower than had been hoped for, due to security concerns and the damage sustained to infrastructure.

EU Gas Storage levels remain very low at just 50% full compared to 60% year and 79% in 2024. Low Storage heading into winter 2026/2027 creates nervousness, especially as Russian LNG was partially banned from April 2026, with a full ban from January 2027.

In the event that European Gas prices do fall, then global competition will likely see some LNG diverted to the likes of Japan, China, South Korea and India.

High temperatures across Europe are creating an increase in energy demand for air cooling.

We would encourage any customer with a contract that ends in the next few months, to discuss your renewals with us and we will look to provide additional market intelligence, guidance and support as required.

Electricity Market Overview

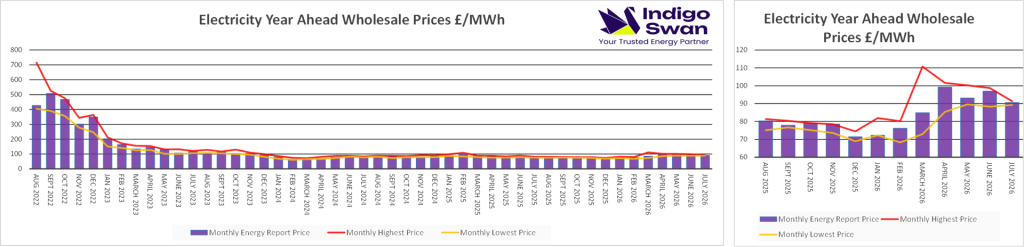

On the 6th of July, the Electricity Year Ahead Wholesale cost was £90.59/MWh, down from £96.96/MWh in last month’s report and 19% higher than 2025.

Today, the 7th of July, is seeing prices move higher following reports of another attack on shipping through the Strait of Hormuz.

Electricity Wholesale costs are still heavily influenced by events in the Middle East due to the use of Gas for generation and how our markets operate. This means there is still considerable uncertainty regarding the direction of prices.

The huge investment in the network to allow more Renewables to be connected and to allow Electricity to be transported further, to avoid regional disparity, means customers should expect increases to the non-Wholesale cost elements.

The above average temperatures both in the UK and on mainland Europe have increased the need for air cooling. The heat can also adversely impact on the performance of some generation, notably French Nuclear, which it exports to the UK and to Solar Panels, which become less efficient as they overheat.

In June, Wind contributed 23% of supplies and Gas 28%, up from 24% in May. The Interconnectors with mainland Europe, which allow both Imports and Exports, provided 17%.

We would encourage any customer with a contract that ends in the next few months, to discuss your renewals with us and we will look to provide additional market intelligence, guidance and support as required.

If you enjoyed reading this blog why not try one of our others: