Headlines:

- Gas and Electricity Wholesale prices are higher than last month

- A number of potential Gas supply issues are adding a premium to prices

- EU Gas Storage levels are a high 95% full

Energy Overview

As of the 4th of November, Gas and Electricity Year Ahead Wholesale costs were higher than in last month’s report.

Price volatility returned in October as energy markets anticipated a more serious escalation in the Middle East, with concern that Israel would retaliate against Iran by attacking their Nuclear and Oil infrastructure. When strikes were not made against those targets, prices began to fall back as Iran appears to want to calm the situation and avoid increasing levels of responses.

We have also seen Norwegian Gas supply outages. Europe’s dependence on Gas from Norway makes us vulnerable to potential supply issues, especially as the Russian imports via Ukraine are ending this year. There have been rumours of alternate routes, but as yet nothing has been confirmed. Despite the desire to stop using Russian Gas and end a source of their income for the Ukraine war, the reality is that Europe still uses both their piped Gas and LNG.

Although EU Gas Storage levels are very high and provide an element of confidence for supplies through the winter, at 95% they are below the 99% seen last year. We have already seen small withdrawals which are likely to increase as temperatures fall.

The National Energy System Operator (NESO) states the Electricity supply margin should be higher this winter.

What does this mean for me?

The energy industry has changed how it recovers Electricity Distribution, Transmission and Balancing costs, under the Targeted Charging Review. This has moved some charges away from being based on the energy used and billed in the unit rate, to fixed charges incorporated within the Standing Charge or as separate items. This should give both the customer and the industry a more accurate way of calculating budgets, but the change has become noticeable within energy bills and created concern. Over the next two years, there is a quite confused picture of increases and decreases in Transmission and Distribution charges, which energy suppliers will be billing customers.

From April 2024 most customers saw a decrease in Transmission which is likely to be followed by an increase in this fixed charge from April 2025, almost completely replacing what used to be recovered through Triads. Distribution costs are a little more complicated with the average fixed annual cost increasing across networks from April 2024 but decreasing from April 2025. Another element, the Available Capacity (AC), has already seen small increases but is due for a more significant rise from April 2025. This does mean that by managing the Agreed Supply Capacity, there is an opportunity to reduce the AC cost and longer term, potentially lower the Band which determines fixed charges.

There is an expectation that Balancing costs will continue to increase.

Indigo Swan works closely with energy suppliers to help all our customers understand and manage changes.

Please contact us on 0333 320 0475 to discuss options or to get a latest update.

Gas market overview

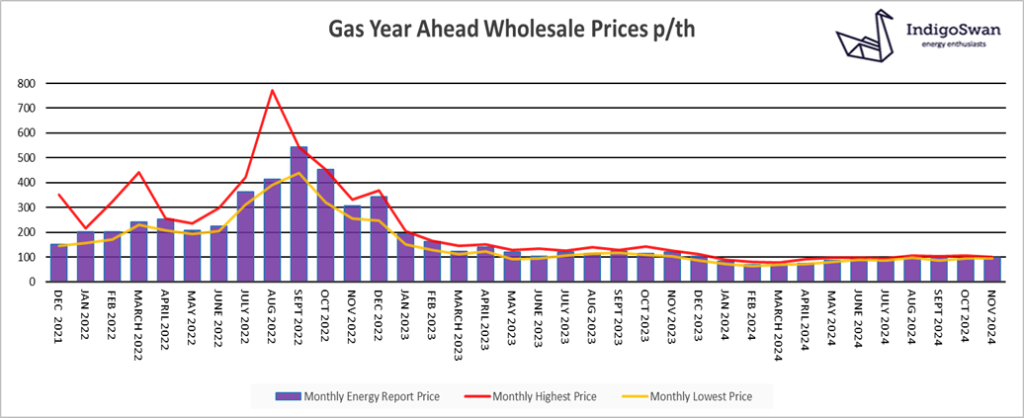

On the 4th of November, the Gas Year Ahead Wholesale cost was 98.24p/th, up from 95.97p/th in last month’s report and 18% less than 2023.

Norwegian Gas supply outages have impacted on prices, but there are other concerns.

As a result of the conflict with Russia, Ukraine will not renew the Gas transit deal with them, which ends this year. Although it currently provides Ukraine with revenue, the benefits favour Russia. Rumours of other routes have soon been dismissed, but the noticeable price reactions demonstrate how much risk is being built into costs. Europe believes they can manage without those supplies, but in the event of a prolonged period of cold weather or further supply issues, then we will be forced to compete on the global market for LNG shipments. It is not clear at this time what the USA’s position will be regarding LNG investment, as previous comments suggested a scaling back.

With reduced supplies coming into Europe, how far will Storage levels be depleted this winter and how much Gas will be available to replace it for winter 2025/26? Levels are currently 95% full compared to 99% last year.

The direction of Wholesale prices is uncertain with a number of events potentially either reducing Gas supplies or increasing demand. We would advise discussing your options for contracts ending in 2024 and early 2025 or at least monitoring the position closely.

Electricity market overview

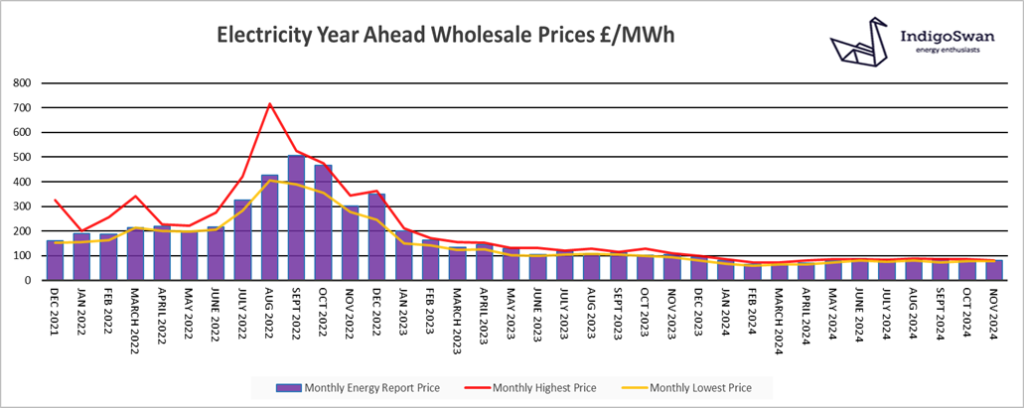

On the 4th of November, the Electricity Year Ahead Wholesale cost was £80.41/MWh, up from £79.33/MWh in last month’s report and 23% less than 2023.

Gas continues to dictate Electricity’s price direction due to its scale and cost, being a flexible and reliable source of generation when Renewables are erratic. It is expected that we will have more spare generation capacity this winter.

The end of the transit deal between Russia and Ukraine will see a reduction of Gas imports in 2025, which is adding pressure to prices. It is hoped that an alternate arrangement can be found, or else supply margins will be tighter, and EU Gas Storage may struggle to be replenished. There is also continued concern that the tensions in the Middle East could restrict exports of Oil and Gas from the region.

In October, 26% of generation was from Wind, 31% from Gas and 14% Imports from Europe via the Interconnectors. Over the last week, Wind has been significantly lower at just 11%, with Gas and Imports compensating.

The direction of Wholesale prices is uncertain with a number of events potentially either reducing Gas supplies or increasing demand. We would advise discussing your options for contracts ending in 2024 and early 2025 or at least monitoring the position closely.

The 2024 Budget

The Labour government’s first budget saw little that directly impacts on Gas and Electricity supplies but focused on investment to secure generation and help achieve Net Zero.

Some notable points include:

- The Climate Change Levy (CCL) for Gas and Electricity will increase in line with RPI in 2026-27.

- The confirmation that the Energy Profits Levy will increase from 35% to 38% as of 1st November 2024 for Oil and Gas companies and is being extended until 31st March 2030. This brings the headline rate of taxation to 78%. This is dependant on prices remaining above historic normal levels for a sustained period.

- An increase in the Air Passenger Duty for 2026-27.

- Provided a budget to Great British Energy which will be located in Aberdeen.

- Maintaining tax incentives to purchase electric cars through Vehicle Excise Duty First Year Rates and Company Car Tax regimes.

- Extending the 100% First Year Allowance for electric cars and charge points, for a further year.

- The investment of £200mn in 2025-26 to accelerate EV charge point rollout with a grant to support local authorities to install on-street charge points across England.

- The one-year extension of the Advanced Fuels Fund, to support the development and production of innovative fuels to decarbonise aviation.

- Supporting existing firms to decarbonise and grow through the £163mn Industrial Energy Transformation Fund.

- The support of local energy schemes with £1bn funding over three years through the Public Sector Decarbonisation Scheme.

- £3.4bn over three years towards the Warm Homes Plan, including £1.8bn to support fuel poverty schemes.

- Increased funding for the Boiler Upgrade Scheme in England and Wales and funding to grow heat pump manufacturing supply chains in the UK.

- £3.9bn in 2025-26 for Carbon Capture, Usage and Storage to decarbonise industry.

- £134mn to support the delivery of port infrastructure to facilitate floating offshore wind.

- The continued development of Sizewell C through 2025-26 with £2.7bn of funding, with a decision on if to proceed with the project to be made at Phase 2 of the Spending Review.

If you enjoyed reading this blog why not try one of our others: