Headlines:

- Gas and Electricity Wholesale prices are unchanged from last week

- EU Gas Storage levels are 56% full compared to 72% last year

- Lower Storage levels are creating nervousness for this winter and 2025/26

Energy Overview

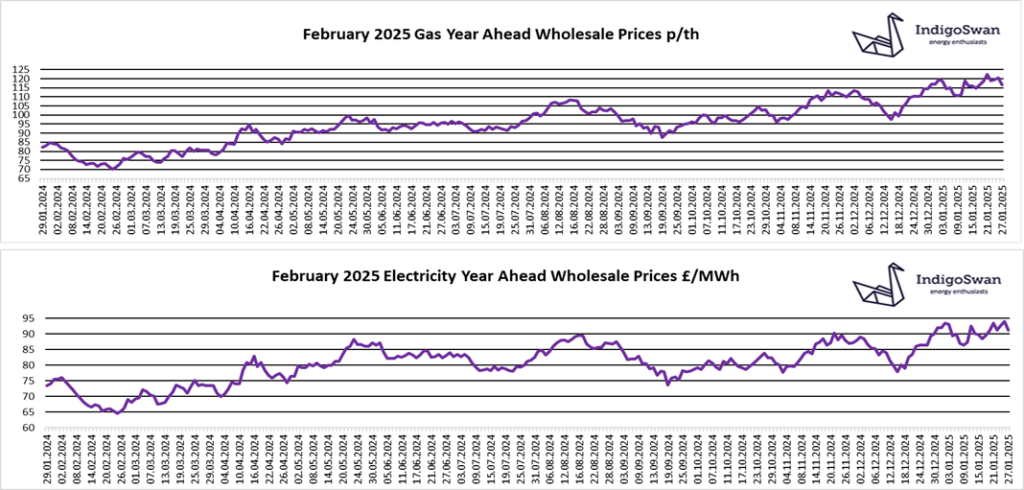

Gas and Electricity Year Ahead Wholesale costs are unchanged from last week. They are similar to 2024, showing good value compared to most of 2021 / 2022 / 2023, but are more than double 2020. The Oil price is lower at $77.

EU Gas Storage levels continue to be a big factor in the direction of Gas and Electricity costs, which hit their highest this month since late 2023. EU Storage is currently 56% full compared to 72% over the last two years. Injections should begin at the end of the winter, but if Gas costs remain high, there may be some hesitation. Also, unless alternate supplies can be found soon to replace those lost due to the end of the Ukraine / Russia transit deal, then Europe will have less surplus Gas in the warmer months. These factors could mean that EU Storage falls short of the 90% full target by November 2025, which has been exceeded for the last three years. The UK has a similar issue as stocks are significantly lower than last year, although by comparison our capacity is just a fraction of other European nations. LNG will continue to be an important source of supplies and with prices increasing, this has attracted more deliveries. There is significant global investment to provide more LNG, as demand is expected to increase. President Trump has reversed the position of the US which is now looking to capitalise by producing and exporting more Oil and Gas.

Storms across the UK have increased Wind’s contribution to generation to 26% of supplies from 16% the week before. This has also meant less demand on Gas, which has fallen to 35% from 55%. Imports of Electricity from the continent via the interconnectors rose to 14% from 6%. It is likely that temperatures will be in the region of seasonal norm over the next couple of weeks, potentially providing an opportunity to reduce the use of Gas for both heating and generation.

We would encourage customers that have Gas or Electricity contracts ending in the first half of 2025, to discuss options with Indigo Swan and closely monitor the position.

If you enjoyed reading this blog, why not try one of our others: