Headlines:

- Gas and Electricity Wholesale prices are higher than last month

- EU Gas Storage levels are 70% full compared to 86% last year

- Potential US sanctions and tariffs from the 8th August, could impact on costs

Energy Overview

As of the 4th of August, Gas and Electricity Year Ahead Wholesale costs were higher than in last month’s report but comparable to last week.

Over the last month, there has been little price movement. The potential outcomes from the recent threats by the US against Russia and third-party countries, have yet to have a significant impact on prices. If Russia does not enter a ceasefire agreement with Ukraine by the 8th of August, they risk sanctions, and those countries doing trade with them, will likely face additional tariffs. India is being highlighted as a target, as they have been buying large volumes of energy from Russia, whereas other nations have chosen to look for other sources, in support of Ukraine. Switches to non-Russian Oil, Coal and Gas will add pressure to supplies and prices.

The contribution of Wind to generation was a low 16% in July, increasing the need for Gas at 26%. Over the last week Wind has increased to 21%, exceeding 40% on the 4th of August.

A meeting of OPEC+ members on the 3rd of August will result in a further increase of Oil production in September. The monthly increases have been reversing large decreases, which aimed at supporting prices. The target seems to be to achieve a stable cost in the region of $70 a barrel, with $71 being the average so far in 2025 and $80 in 2024.

Other Industry Costs

The energy industry has changed how it recovers Electricity Distribution, Transmission and Balancing costs, under the Targeted Charging Review. This has moved some charges away from being based on the energy used and billed in the unit rate, to fixed charges incorporated within the Standing Charge or as separate items. This should give both the customer and the industry a more accurate way of calculating budgets, but the change has become noticeable within energy bills and created concern. Over the next two years, there is a quite confused picture of increases and decreases in Transmission and Distribution charges, which energy suppliers will be billing customers.

From April 2025 customers will have seen an increase in Transmission costs with an expectation of further increases from April 2026. Distribution costs are a little more complicated with the average fixed annual cost decreasing across networks from April 2025, remaining similar in 2026. Another element, the Available Capacity (AC), increases significantly for most from April 2025, with small reductions in 2026. This does mean that by managing the Agreed Supply Capacity, there is an opportunity to reduce the AC cost and longer term possibly lower the Band which determines Transmission and Distribution fixed charges.

Balancing costs, which pay to fine tune Electricity supplies to avoid power cuts, will increase from October 2025.

Indigo Swan works closely with energy suppliers to help all our customers understand and manage changes.

Please contact us on 0333 320 0475 to discuss options or to get a latest update.

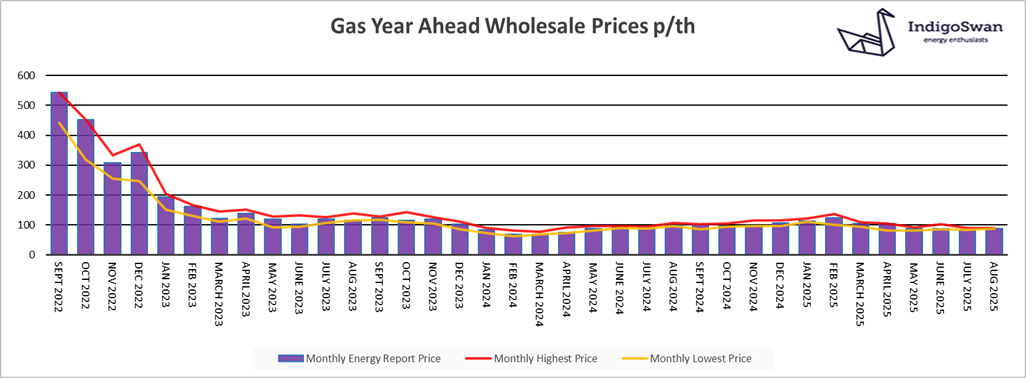

Gas Market Overview

On the 4th of August, the Gas Year Ahead Wholesale cost was 88.46p/th, up from 84.81p/th in last month’s report and 11% less than 2024.

The revised deadline issued by the US, for Russia to enter a ceasefire agreement with Ukraine, is the 8th of August. Potentially Russia will face more sanctions and third-party nations could be penalised with additional tariffs, if they continue to buy energy from Russia. If India for example, chooses to buy Oil and Coal from other sources, this would add pressure to supplies and global prices. They currently buy little LNG.

As part of the tariff negotiations with the US, the EU has committed to buying very large volumes of LNG over the next 3 years. This sends positive signals to investors of LNG infrastructure and energy markets, as it is an important source of Gas. The US is already the largest exporter, replacing some of the piped Gas that Russia previously supplied to Europe. Russia has increased sales to China and is targeting India.

EU Gas Storage levels remain very low at just 70% full compared to 86% last year. This could create a nervousness should there be forecasts of below average temperatures in Europe this winter, with prices likely to increase.

We would encourage those with Gas and Electricity contracts that are due to end in the next few months and potentially further out, to engage with Indigo Swan and monitor positions closely.

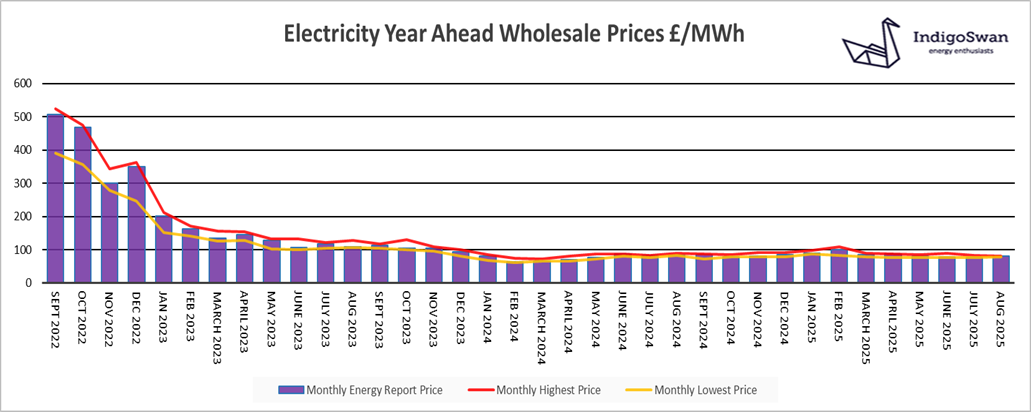

Electricity market overview

On the 4th of August, the Electricity Year Ahead Wholesale cost was £80.30/MWh, up from £76.00/MWh in last month’s report and 4% less than 2024.

Global issues have a big impact on the price of our Electricity. With Gas providing 26% of our generation in July, up from 19% in June, its high cost continues to largely dictate the direction of Wholesale Electricity. Wind fell to just 16%, although in recent days it has increased significantly. A strong Wind contribution is good, but due to the issues with transporting it to the areas of demand, generators are sometimes paid to not supply, in order to protect the network. This adds large Balancing costs to consumer’s bills. Imports from Europe via the Interconnectors accounted for 20% of supplies.

The Gas Storage levels in the EU remain low at just 70% full compared to 86% in 2024. This could add a further pressure to global prices as we approach the winter and then have an impact on Electricity. LNG prices could increase depending on the outcome of the sanctions and tariffs which the US may impose on Russia and third-party countries. LNG is also subject to regional demand fluctuations, for example, with Asia’s need for generation for air cooling.

We would encourage those with Gas and Electricity contracts that are due to end in the next few months and potentially further out, to engage with Indigo Swan and monitor positions closely.

If you enjoyed reading this blog why not try one of our others: