Headlines:

- Prices are higher than in last week’s report

- There are a number of factors which could impact energy costs

- EU Gas Storage levels remain low at 79% full

Energy Overview

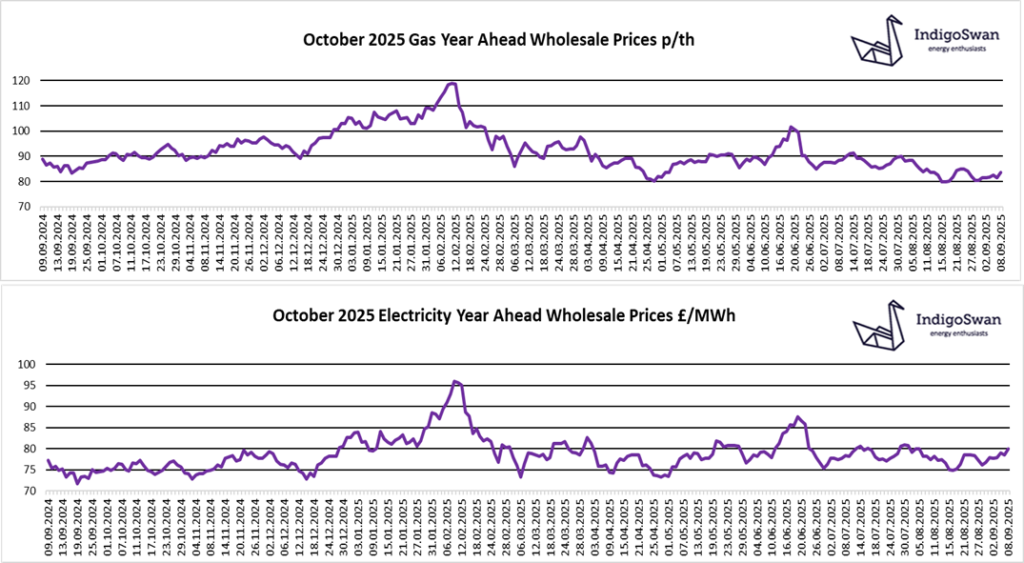

Gas and Electricity Year Ahead Wholesale costs are higher than those in last week’s report. They remain significantly lower than most of 2021 / 2022 / 2023 but are comparable to 2024. Oil is $67 a barrel, from $68. OPEC+ agreed further production increases from October 2025.

We await further developments on current issues, which could influence energy costs. The initial momentum of the peace talks between Ukraine and Russia has been lost, which is reflected in prices moving a little higher. More talks are expected but seem to exclude the key direct discussions between Presidents Putin and Zelensky. The US may finally lose patience and apply the threatened tariffs against Russia, which could add upward pressure to prices. However, China has recently been receiving sanctioned Russian LNG and has just agreed the construction of a new Gas pipeline between the two countries, so measures by the West are becoming less effective.

EU Gas Storage is still far lower than last year at 79% full compared to 93% and will likely be sufficient to meet the higher winter demand. We continue to see good levels of LNG shipments from the US, which are helping to replace lower piped supplies from Russia. Should there be indications of a prolonged colder than average spell, then prices may move higher.

The contribution of Wind to generation fell slightly over the last week to 27%, requiring more Gas at 22% and Imports via the Interconnectors at 18%.

We would encourage those with energy contracts ending in the next few months and potentially further out, to engage with Indigo Swan and monitor positions closely.

If you enjoyed reading this blog, why not try one of our others: