Overview

As of the 7th September, Gas and Electricity Year Ahead Wholesale costs are higher when compared to last month’s report.

The price of Oil is lower at $42 a barrel, from $44. OPEC+, which includes Saudi Arabia and Russia, reduced the extent of their production cuts in August, in anticipation of a global economic recovery. However, rising coronavirus cases and poor growth data from the US, would indicate a subdued demand.

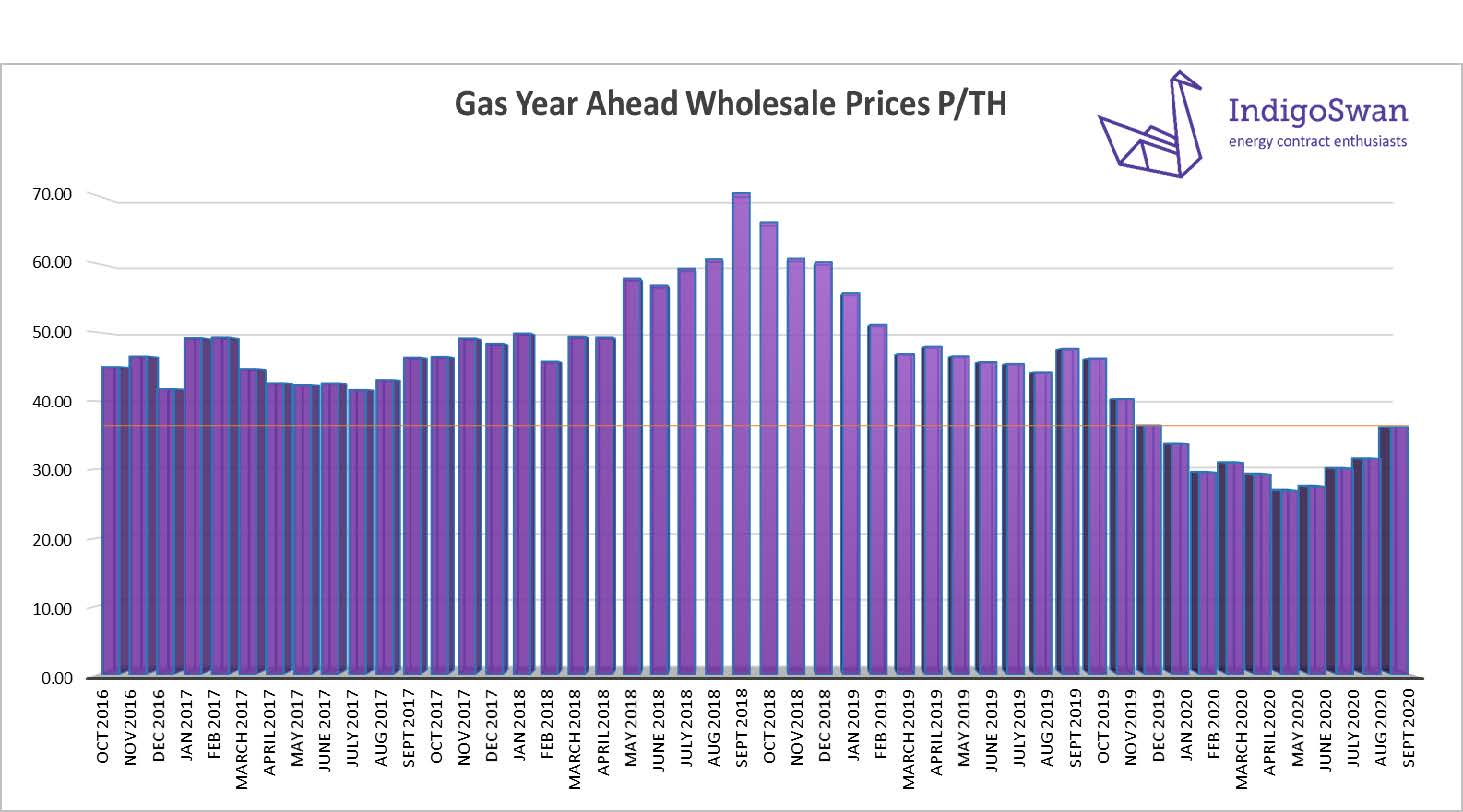

Gas Wholesale costs are higher but remain competitive, as illustrated by our graph. There has recently been a high use of Gas for Electricity generation as well as supply disruptions. August saw eight LNG deliveries, up from six in July, but still far lower than previous months. This is not likely to change in September, with high levels of Gas storage and a low cost, giving LNG producers little incentive to sell.

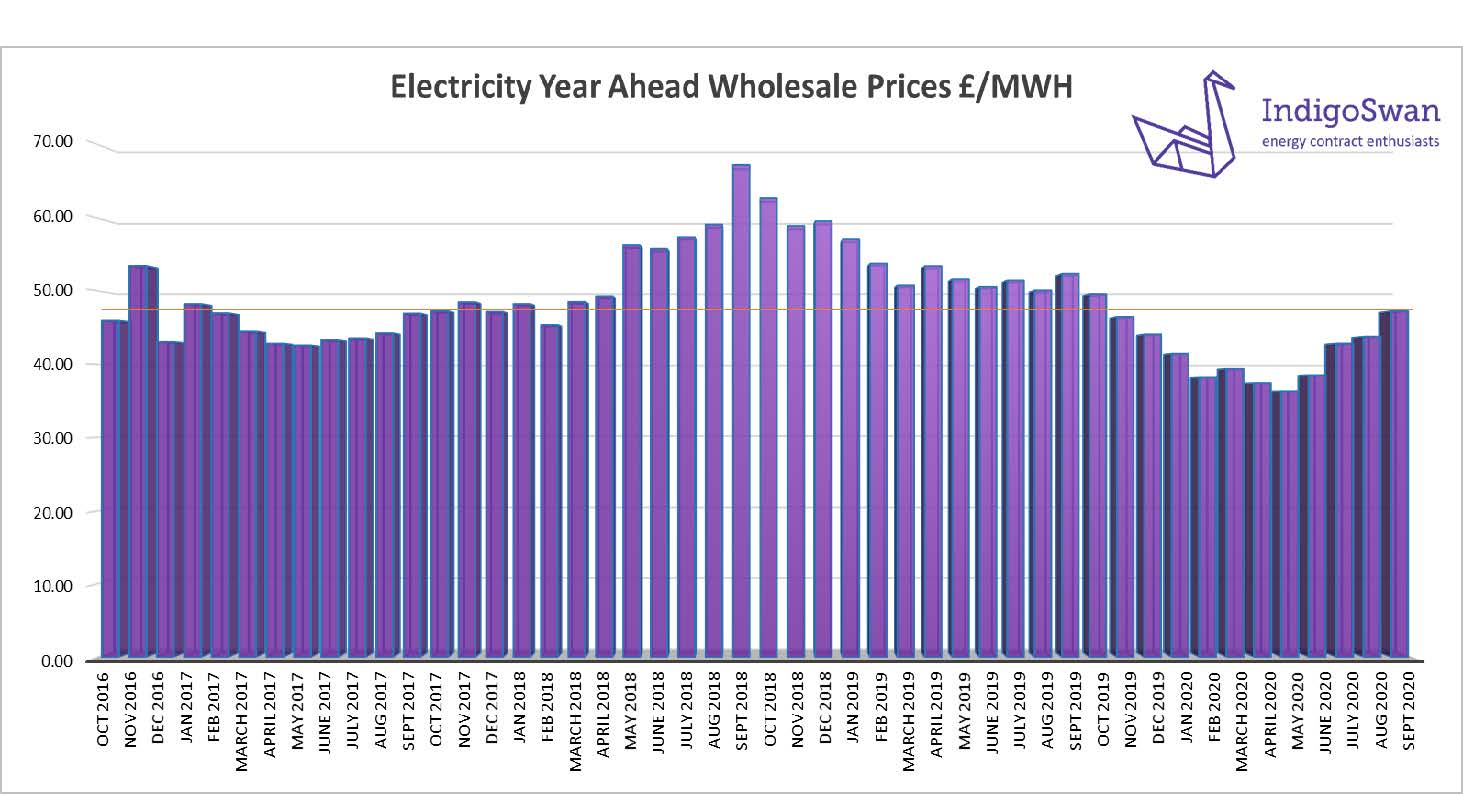

Electricity Wholesale prices are less competitive but are still lower than 2018 and most of 2019. Modest levels of Renewable and Nuclear generation has meant a greater use of Gas and Coal, which increases costs. Another factor has been the rise in Carbon prices, due to an increase in fossil fuel generation in Europe. This is an added cost for our generators.

The Met Office forecast for the next month suggests average temperatures and changeable conditions, including rain and gales in some regions. Cooler temperatures will likely place a further demand on Gas, which could, if still heavily supporting Electricity generation, push both prices higher.

What does this mean for me…?

Wholesale prices still show good value. It should be remembered that this element makes up in the region of just 40% of the total cost of an Electricity bill and roughly 60% for Gas.

The influence of increasing third-party costs is noticeable in Electricity contracts. These include, Transportation, Distribution, and government policy levies.

Over the next few years, the way some of these charges are calculated will change, under the Targeted Charging Review, although the details are not yet available. Initially the first change to Transportation costs was due April 2021, but with delays issuing price guidelines to energy suppliers, this has been postponed until April 2022. The planned change to Distribution charges is still set for April 2022. This does mean that the expected opening of some fixed priced contracts should not take place until 2022.

We advise requesting supplier offers for all 2020 and early 2021 start contracts to compare against your current prices. Be aware that suppliers are tightening their credit requirements and reducing their risk appetite, but good forward contract options can still be negotiated.

Please contact us on 0333 320 0475 to discuss options or to get a latest update.

Gas Markets

On the 7th September, the Gas Year Ahead Wholesale cost was 36.07 (p/th), from 31.48 (p/th) in last month’s report and 24% lower than 2019.

Gas supply outages have put some pressure on the system at times, although our Storage levels remain high. LNG deliveries were higher at eight, but still far short of the twenty plus previously seen. If Gas prices increase, we would expect more LNG deliveries.

The added demand for Gas to be used for Electricity generation is another contributing factor to the price rise. Both Renewables and Nuclear have underperformed in recent weeks, with Gas providing 45% in August compared to 35% in 2019 and 44% so far in September.

Oil has some historic contractual links with Gas prices, but in this case, other factors have outweighed the slightly reduced Oil price.

Let us know if you would like us to research your options for 12, 24 and 36 month contracts.

Electricity Market

On the 7th September, the Electricity Year Ahead Wholesale cost was 47.27 (£/MWh), from 43.77 (£/MWh) in last month’s report and 10% lower than 2019.

There was little change in Electricity demand in August when compared to July. This was just 3% lower than 2019, which could be attributed to a general trend of lower energy use.

Wind, Solar and Nuclear generation have all been low and so required a greater use of Gas, which itself has been under some pressure due to supply disruptions and cooler temperatures. This has increased Electricity Wholesale costs. We have also needed to use Coal, which is an expensive substitute, although this did account for less than 1% of the fuel mix.

Nuclear shutdowns in France and the subsequent use of fossil fuel generation, has increased the cost of the required Carbon levy, that our generators must pay, due to their higher emissions.

Third Party Charges continue to increase regardless of how the Wholesale element changes. These charges typically pay for the mechanisms, securing generation at peak periods.

Let us know if you would like us to research your options for 12, 24 and 36 month contracts.