Headlines:

- Gas and Electricity Wholesale prices are similar to last month

- EU Gas Storage levels are just 60% full compared to 70% last year

- The increasing availability of LNG is reducing pressure on energy costs

Energy Overview

As of the 5th of January, Gas Year Ahead Wholesale costs were lower than last month, but Electricity was slightly higher. Oil remains stable, in the region of $62 a barrel, with OPEC+ once again pausing the series of production increases which followed previous cuts. OPEC+ will monitor the position in Venezuela and review output from April 2026.

EU Gas Storage levels have fallen to just 60% full compared to 70% last year. They are comparable to the lows in 2022 which saw a significant increase to Gas and Electricity Wholesale prices, with fears of supply shortages. However, with supplies from Norway and LNG shipments replacing Russian Gas, there is now more confidence. The EU’s ban on Russian LNG from January 2027 and flows from 2028, means supplies may become tighter, and replacing the low winter levels during the summer could be more of a challenge.

There is still hope that a peace deal can be agreed between Russia and Ukraine, which would likely reduce some of the current restrictions on Russian supplies and lower costs.

Wind’s contribution to generation was a high 33% in December and 37% in the last week. This has reduced the need to use Gas.

Other Industry Costs

The energy industry has changed how it recovers Electricity Distribution, Transmission and Balancing costs, under the Targeted Charging Review. This has moved some charges away from being based on the energy used and billed in the unit rate, to fixed charges incorporated within the Standing Charge or as separate items. This should give both the customer and the industry a more accurate way of calculating budgets, but the change has become noticeable within energy bills and created concern.

From April 2025 customers will have seen an increase in Transmission costs with an expectation of further increases from April 2026. Distribution costs are a little more complicated with the average fixed annual cost decreasing across networks from April 2025, remaining similar in 2026. Another element, the Available Capacity (AC), increased significantly for most from April 2025, with small reductions in 2026. This does mean that by managing the Agreed Supply Capacity, there is an opportunity to reduce the AC cost and potentially lower the Band which determines Transmission and Distribution fixed charges.

Balancing costs, which pay to avoid power cuts are increasing and the Energy Intensive Industries (EII) charge, which currently provides relief from various industry costs for EII customers at 60%, is increasing to 90% from April 2026.

Indigo Swan works closely with energy suppliers to help all our customers understand and manage changes.

Please contact us on 0333 320 0475 to discuss options or to get a latest update.

Gas Market Overview

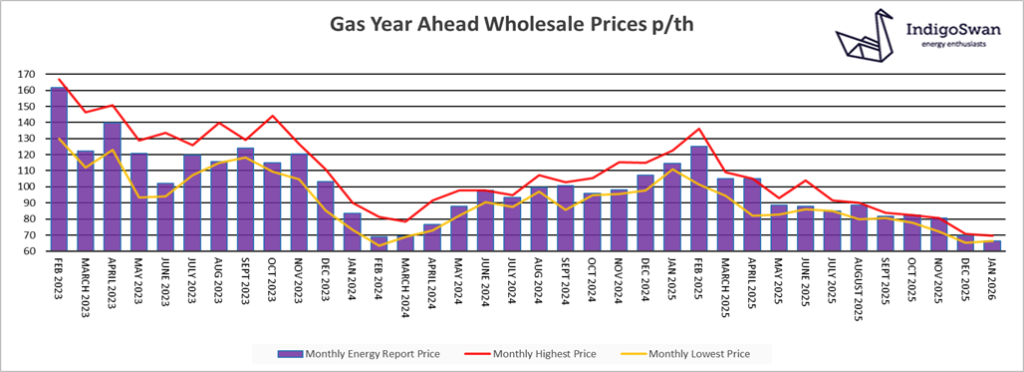

On the 5th of January, the Gas Year Ahead Wholesale cost was 66.26p/th, down from 69.53p/th in last month’s report and 42% less than 2025. Prices are lower than last week.

The recent cold spell added pressure to prices over the last month, as EU Gas Storage fell further to 60% full compared to 70% last year. With Storage being so low, it would have been expected that Gas Wholesale prices would be far higher than they are. Having experienced supply concerns in recent years and with other sources of Gas now replacing most Russian supplies, there is less concern than in 2022, when Wholesale prices reached record highs.

The US continues to supply large quantities of LNG to Europe, which are set to increase with more investment and new facilities. Although Russian Gas to the EU is lower, they are supplying more to China. As we have seen in the last month, if Gas prices are too low, LNG deliveries will slow down and wait for margins to improve. Gas Storage will need to be replaced through the warmer months, so pressure continues throughout the year, even when consumer demand is lower. The EU is banning Russian LNG from January 2027 and all flows in 2028.

We would encourage those with Gas and Electricity contracts that are due to end in the next few months and possibly further out, to potentially take advantage of the competitive prices and to engage with Indigo Swan to monitor positions closely.

Electricity Market Overview

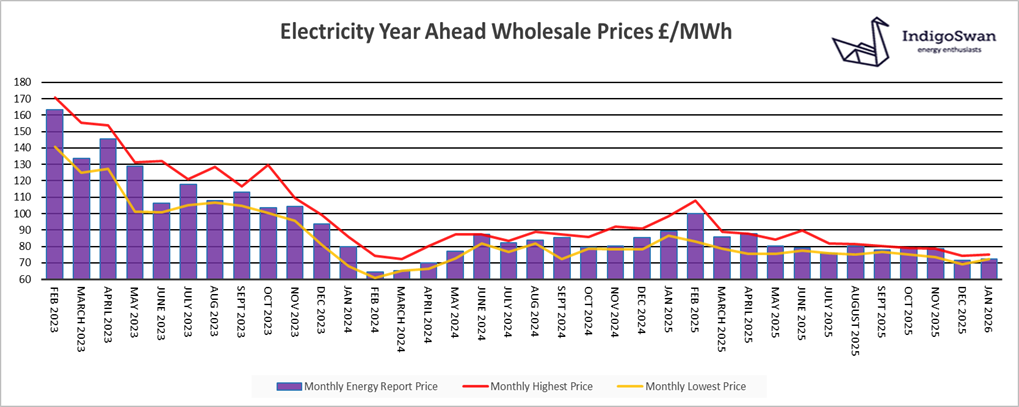

On the 5th of January, the Electricity Year Ahead Wholesale cost was £72.27/MWh, up from £71.39/MWh in last month’s report and 19% less than 2025. Prices are lower than last week.

The contribution of Wind to generation increased from 32% in November to 33% in December, which helped reduce the use of Gas from 29% to 27%. Imports via the Interconnectors with Europe were up from 12% to 16%. Over the last week Wind has been a very high 37% of supplies.

Electricity prices closely follow Gas due to its high cost. With more sources of Gas being available and less focus on EU Gas Storage levels, this is being reflected in low Wholesale prices. The delivered cost of Electricity continues to be pressured higher due to other charges. These pay to secure generation, especially when demand is higher, but also to provide investment for the upgrade of the network, to allow more Renewables to be connected and transported. This will help reduce the high Balancing costs which at times pay Wind to stop generating in one region and Gas to be available in another.

We would encourage those with Gas and Electricity contracts that are due to end in the next few months and possibly further out, to potentially take advantage of the competitive prices and to engage with Indigo Swan to monitor positions closely.

If you enjoyed reading this blog why not try one of our others: