Headlines:

- Prices are higher than in last week’s report

- Talks have so far failed to deliver peace between Ukraine and Russia

- EU Gas Storage levels remain low at 76% full

Energy Overview

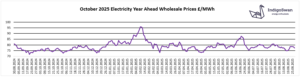

Gas and Electricity Year Ahead Wholesale costs are higher than those in last week’s report. They remain significantly lower than most of 2021 / 2022 / 2023 but are comparable to 2024. Oil is $68 a barrel, from $66.

Energy prices have moved higher, to the levels seen before the announcement that the US sanctions against Russia would be delayed and that peace talks would take place. Although it was not expected that Russian Gas would begin flowing into Europe in the short term, an agreement would likely have seen their global trade increase or at least not face additional restrictions. President Putin’s stalling may mean that the US once again threatens Russia with sanctions and indirectly by imposing tariffs against those that buy from them. They could also look to pressure Ukraine to accept terms that are seen as unreasonable and dangerous by most European leaders.

The filling of EU Gas Storage is making slow progress at 76% full. Last year injections continued until late October, reaching 96%, but this largely depends on the temperatures across Europe and the availability of Gas. We no longer have the supplies that came from Russia via Ukraine, which ended in January 2025. It is very unlikely that restrictions on supplies would need to be put in place, but forecasts of colder than average periods will probably be reflected in higher Gas and Electricity Wholesale costs.

The contribution of Wind to generation increased slightly but remained low at 14% of supplies. Gas provided 30% and

Imports via the Interconnectors with Europe 23%.

We would encourage those with energy contracts ending in the next few months and potentially further out, to

engage with Indigo Swan and monitor positions closely.

If you enjoyed reading this blog, why not try one of our others: