Headlines:

- Increased Gas and Electricity Wholesales costs.

- Delay approving the Nord Stream 2 Gas pipeline.

- European Gas Storage levels at just 56% compared to 73% last year.

Energy Overview

As of the 4th of January, Gas and Electricity Year Ahead Wholesale costs were higher, when compared to last month’s report. The Oil price is $80 per barrel, from $73, recovering due to reduced fears as to the severity of Omicron.

During December there was extreme price volatility, with already high prices doubling in the space of two weeks, peaking on the 22nd of December. A number of concerns contributed but could possibly be seen as the market losing sight of the fundamentals, and prices have since fallen back.

Russia continues to dominate price direction. Their refusal to provide Europe with additional Gas supplies through existing routes means European Storage levels are just 56% full compared to 73% last year. The use of the new Nord Stream 2 pipeline would allow Russia to export large volumes of Gas and avoid transit fees through Ukraine. Germany has refused their approval until conditions have been met, with the US and allies questioning the wisdom of its use due to the leverage it gives Russia. The pipeline is also being used as a tool to persuade Russia not to invade Ukraine. Presidents Biden and Putin have had dialogue, but the threat of military action and subsequent sanctions remain a real possibility. With Gas being the main source of generation, Electricity prices have seen a similar price movement.

The Met Office forecast for the next month suggests temperatures generally at seasonal norm with periods of strong winds and the potential for snow on higher ground and overnight frosts.

What does this mean for me?

Wholesale prices for 2022 remain very high when compared to recent years. Prices for later in 2022 and 2023 show better value. Generally, the Wholesale element makes up in the region of just 40% of the total cost of an Electricity bill and 60% for Gas, but these percentages are currently much higher, estimated in excess of 60% and 80%.

Increasing third-party costs are noticeable in Electricity contracts. These include Transmission, Distribution, Balancing and government policy levies, which ensure we have enough energy to meet demand and provide investment.

Over the next year or two, the way some of these charges are calculated will change, under the Targeted Charging Review. Energy suppliers can choose whether to fix Electricity contract costs, pass them through or leave that decision until a later date. This does allow for the possibility of a review of the Distribution charges in some fixed price Electricity contracts from April 2022. It is understood the Transmission element will be delayed until at least April 2023.

The direction of prices will likely depend on European Gas Storage levels. Should there be prolonged periods of cold temperatures this Winter and if Russia does not provide additional supplies, there is the potential for continued price volatility. If Russia invades Ukraine, the sanctions will have the potential for an extreme price reaction.

We would advise looking at your options for contracts ending Q1 of 2022 and monitoring closely, those remaining in 2022. There is an opportunity to contract for two or three years to dilute the impact of the higher short-term costs.

Please contact us on 0333 320 0475 to discuss options or to get a latest update.

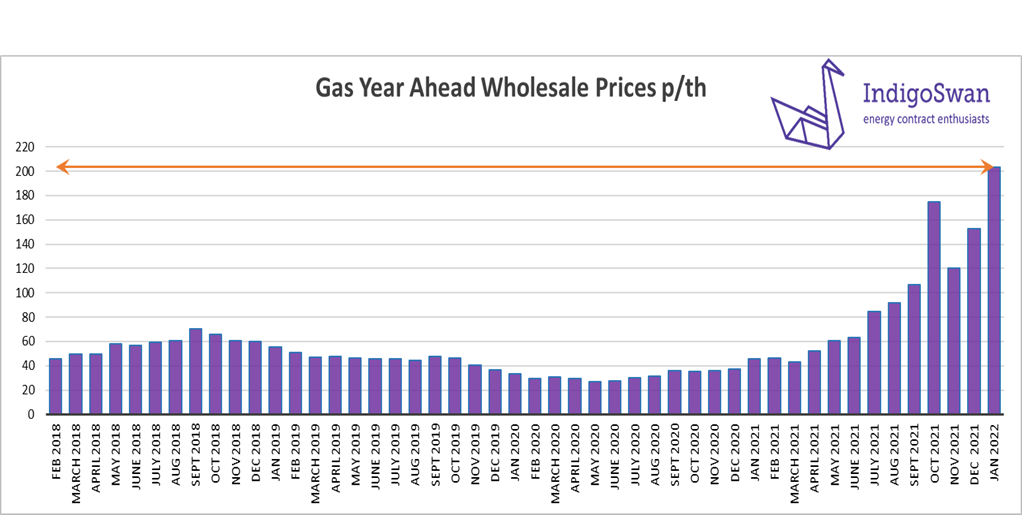

Gas market overview

On the 4th of January, the Gas Year Ahead Wholesale cost was 203.37p/th, up from 152.60p/th in last month’s report and 345% higher than 2021. Prices later in the year and 2023, are considerably lower.

Germany will not sign off Russia’s use of the Nord Stream 2 Gas pipeline until the operating company complies with German law. Russia’s condition for providing much needed supplies appears to be through this pipeline rather than existing routes. This continues to cause concern due to European Gas Storage levels being just 56% full compared to 73% last year. There is added nervousness at the prospect of Russia invading Ukraine and the subsequent sanctions, which would include Nord Stream 2.

The UK’s Gas Storage is almost full, with good supplies from the North Sea and Norway, topped up by improved LNG shipments. However, as Gas is a global commodity, our Gas Wholesale price has been pressured upwards.

Temperatures will likely remain in the region of seasonal norm in January, reducing the likelihood of a period of sustained heating demand.

Let us know if you would like us to research your options for 12, 24 and 36 month contracts.

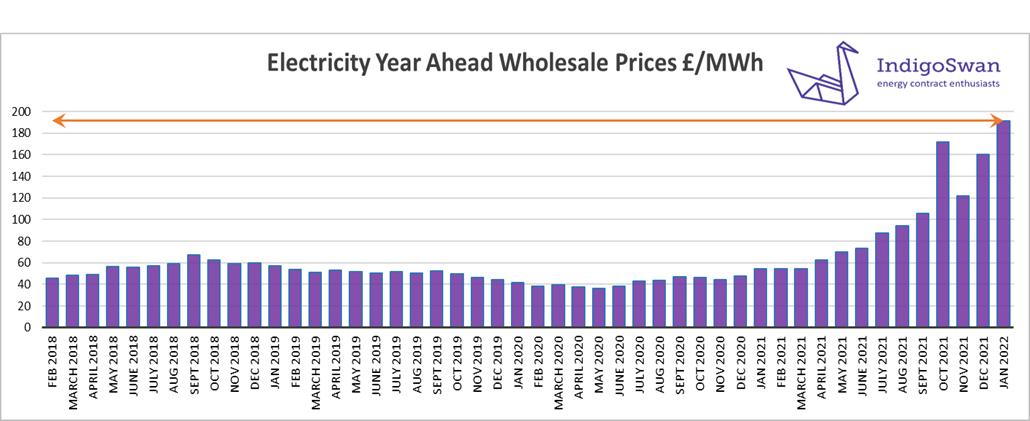

Electricity market overview

On the 4th of January, the Electricity Year Ahead Wholesale cost was £191.26/MWh, up from £160.05/MWh in last month’s report and 253% higher than 2021. Prices later in the year and 2023, are considerably lower.

Gas provided 39% of our generation in December, meaning the Electricity price closely followed the cost of Gas, which has been extremely volatile over the last month. Although there has been some easing, prices remain very high.

Wind’s contribution was just 22% in December. The forecast for January looks higher and has so far provided 40%, which does ease pressure on Gas supplies and prices. Our Electricity Interconnectors with Europe play an increasingly important role in balancing our network, providing 9% of our supplies in December. The partial outage with France in September 2021, is returning late 2022. More recently, some French Nuclear generation went offline due to safety concerns which may restrict Imports. The new, North Sea Link with Norway, is providing almost 2% of our Electricity.

Despite the planned closure of Coal generation in the UK by 2024, it still regularly contributes 2% of supplies.

The National Grid has mechanisms in place, to secure additional supplies or reduce demand. These do come at a cost, in the form of higher third-party charges within Electricity bills, but provide an element of stability to prices which otherwise may react even more dramatically.

Let us know if you would like us to research your options for 12, 24 and 36 month contracts.