Headlines:

- Very high Gas and Electricity Wholesale costs.

- Further disruption to Gas imports from Russia.

- EU Gas Storage levels are an improved 82% full, compared to 69% last year.

Energy Overview

As of the 5th of September, Gas and Electricity Year Ahead Wholesale costs were higher, when compared to last month’s report. The Oil price is lower at $96 per barrel, from $110.

Prices continue to increase as Russia takes measures to reduce Gas supplies into Europe, creating concern and instability. The assumption is that this is in response to sanctions and the assistance being provided to Ukraine.

On the 19th of August Russia announced a further three-day shutdown of Nord Stream 1. Both Gas and Electricity Wholesale prices began to increase, hitting record highs, before falling back. However, as suspected, the closure has now been extended for the foreseeable future, with disputed claims of further issues found during the maintenance. It is more likely their action is directly linked to the G7 announcement of an intention to place a price cap on Russian Oil exports.

Electricity prices are impacted by Gas due to its use for generation. The hot dry spell across Europe has also influenced costs due to low water levels to transport fuel, cool reactors and generate Hydro power.

The Met Office forecast suggests we will generally see seasonal norm temperatures in September. Conditions will be unsettled with some showers and the potential for stronger winds.

What does this mean for me?

Wholesale prices for 2022 remain very high when compared to recent years. Prices for 2023 and 2024 show better value. Generally, the Wholesale element makes up in the region of just 40% of the total cost of an Electricity bill and 60% for Gas, but these percentages are currently much higher, estimated at 90%.

Increasing third-party costs are noticeable in Electricity contracts. These include Transmission, Distribution, Balancing and government policy levies, which ensure we have enough energy to meet demand and provide investment.

Over the next year, the way these charges are calculated will change, under the Targeted Charging Review. Energy suppliers can choose whether to fix Electricity contract costs, pass them through or leave that decision until a later date. This does allow for the possibility of a review of the Transmission and Balancing charges in some fixed price Electricity contracts, as the pricing method is due to change from April 2023.

Indigo Swan will be working closely with energy suppliers to best help all our customers through this worrying time, where there is a great deal of uncertainty as to developments in Ukraine and the impact they have on energy costs. Some suppliers are still hesitant to provide contract offers and they may be withdrawn at short notice.

We would advise looking at your options for contracts ending 2022. There is an opportunity to contract for two or three years to dilute the impact of the higher short-term costs.

Please contact us on 0333 320 0475 to discuss options or to get a latest update.

Gas market overview

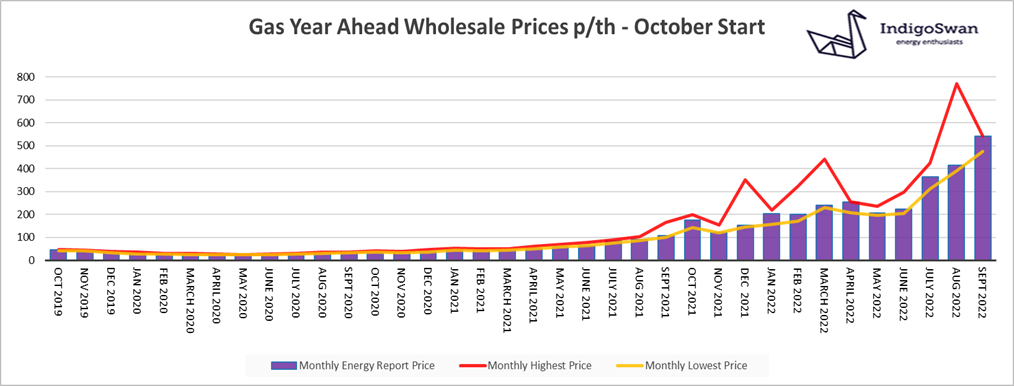

On the 5th of September, the Gas Year Ahead Wholesale cost was 543.04p/th, up from 414.27p/th in last month’s report and 410% higher than 2021. Prices for 2023 and 2024 are considerably lower.

August saw record high Gas prices as Russia announced the closure of Nord Stream 1 for three days. The concern that flows would not return were justified as on the 2nd of September they claimed there were issues, requiring it to be offline for the foreseeable future. This action is a demonstration as to why the EU put in place a requirement for their Storage levels to be at least 80% full by November, with a preferred target of 85%. At this time, they are 82% full, from 70% last month. News of the extension did create a significant initial price increase, before markets factored in the more positive fundamentals and fell back.

The EU has a voluntary 15% reduction in Gas consumption up until March 2023, which may become mandatory, requiring state intervention to restrict Gas use by non-essential users. LNG deliveries remain high, which has provided some relief, despite the US Freeport LNG facility’s return being delayed until November.

The use of Gas for generation remains very high, adding an additional pressure. This is due to a low Renewables contribution and supply issues across Europe, which includes the closure of a number of Nuclear reactors in France due to safety concerns.

Let us know if you would like us to research your options for 12, 24 and 36 month contracts.

Electricity market overview

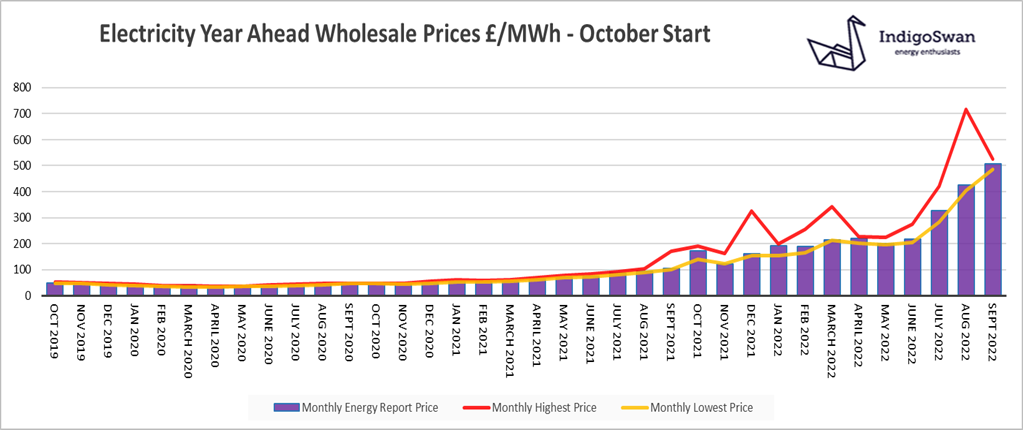

On the 5th of September, the Electricity Year Ahead Wholesale cost was £507.28/MWh, up from £426.60/MWh in last month’s report and 379% higher than 2021. Prices for 2023 and 2024 are considerably lower.

Electricity prices continue to be driven by the cost of Gas generation, which accounted for an extremely high 50% of supplies in August. Wind’s contribution fell to just 13%, the lowest since July 2021. This reliance on Gas and the concern that supplies may be stopped by Russia, will continue to inflate prices, especially if there are forecasts for very low temperatures this winter, which would increase demand.

Due to our connectivity with Europe through Interconnectors, we are exporting large amounts of power. They currently have generation issues caused by the lack of rain over the summer and large numbers of the French Nuclear reactors being offline due to safety concerns.

The National Grid has mechanisms in place to secure additional supplies or reduce demand. These do come at a cost premium, in the form of higher third-party charges within Electricity bills, but provide an element of stability to prices which otherwise may react even more dramatically. An example has been the securing of Coal generation this winter if required to meet any spikes in demand.

Let us know if you would like us to research your options for 12, 24 and 36 month contracts.

If you enjoyed reading this blog why not try on of our others: