Headlines:

- Gas and Electricity Wholesale prices have fallen further

- EU Gas Storage levels are a reduced 70% full

- More LNG shipments should be available from February with Freeport due to reopen

Energy Overview

As of the 6th of February, Gas and Electricity Year Ahead Wholesale costs were lower, when compared to last month’s report and back to levels seen in 2021.

Oil struggles to find price direction and has fallen from $82 to $81 per barrel, hitting a high of $88. It is thought the members of OPEC+ are unlikely to change the current productions levels, in an attempt to inflate the price.

Although EU Gas Storage levels have reduced from 84% to 70% over the last month, it remains a positive position compared to the concerns through 2022, when it was feared restrictions on use may need to be enforced. Thoughts are already turning to the requirements for winter 2023/24. LNG deliveries continue to be made and can now be shipped direct to the new German facilities. Additional supplies are also expected soon as the US Freeport LNG terminal is due back online shortly, following the fire last year.

Gas is an expensive form of Electricity generation and sets the Wholesale price, despite the high contribution of much cheaper Wind. A market review is looking at how Renewables could be priced separately, but in the meantime has seen the government increase Green generator’s tax, to help fund some of the support measures in place.

The Met Office forecast is for seasonal norm temperatures and regional windy conditions at times in February.

What does this mean for me?

The Energy Bills Discount Scheme (EBDS) will be the replacement of the Energy Bill Relief Scheme (EBRS), effective 1st April 2023. It is designed to give all non-domestic customers, including the voluntary sector (such as charities) and the public sector (such as schools and hospitals) access to a phased in maximum discount when the customer’s wholesale cost exceeds the defined thresholds. This will last for 12 months until 31st March 2024 and will apply to contracts that were put in place on or after 1st December 2021 and non-contracted arrangements. Those companies that are classed as Energy and Trade Intensive Industries (ETII) will receive a more attractive discount once applied for. As with the EBRS, energy suppliers will automatically apply these standard discounts. Although the levels of assistance are lower and are based on a high wholesale cost, the price of Gas and Electricity has fallen recently. Please see our Blog for more details.

Over the next year, the way some charges are calculated will change, under the Targeted Charging Review. Energy suppliers can choose whether to fix Electricity contract costs, pass them through or leave that decision until a later date. This does allow for the possibility of a review of the Transmission and Balancing charges in some fixed price Electricity contracts, as the pricing method is due to change from April 2023.

Indigo Swan will be working closely with energy suppliers to help all our customers through this worrying time.

Please contact us on 0333 320 0475 to discuss options or to get a latest update.

Gas market overview

On the 6th of February, the Gas Year Ahead Wholesale cost was 161.63p/th, down from 194.63p/th in last month’s report and down 20% on 2022. 2024 prices are similar.

Prices are significantly lower than 2022 as much of the negative sentiment has been removed. EU Gas Storage levels remain high, despite falling to 70% full, as cold spells finally start to impact on supplies. Record numbers of LNG shipments will be added to, as the Freeport LNG terminal is due to come online in February, following a number of delays. With China ending lockdown measures there could be renewed demand from Asia. The UK’s smaller Gas Storage facilities are still well stocked. Our largest, Rough, which was only recently reopened at 20% of working capacity, continues to have an uncertain future as investment is discussed between the government and Centrica.

On the 19th of December the EU agreed a cap on Gas costs at €180/MWh, from 15th of Feb 2023 for 12 months. It will be triggered should the price exceed this for three days and be €35/MWh higher than the price of LNG. This is designed to prevent prices reacting with the extreme volatility that we saw in 2022, which has created considerable global economic issues and provided Russia with resources for their war effort.

The contribution of Gas for generation was very low in January at 30% and with milder temperatures forecast and periods of high winds, it is hoped demand for power and heating will be low in February.

Let us know if you would like us to research your options for 12, 24 and 36 month contracts.

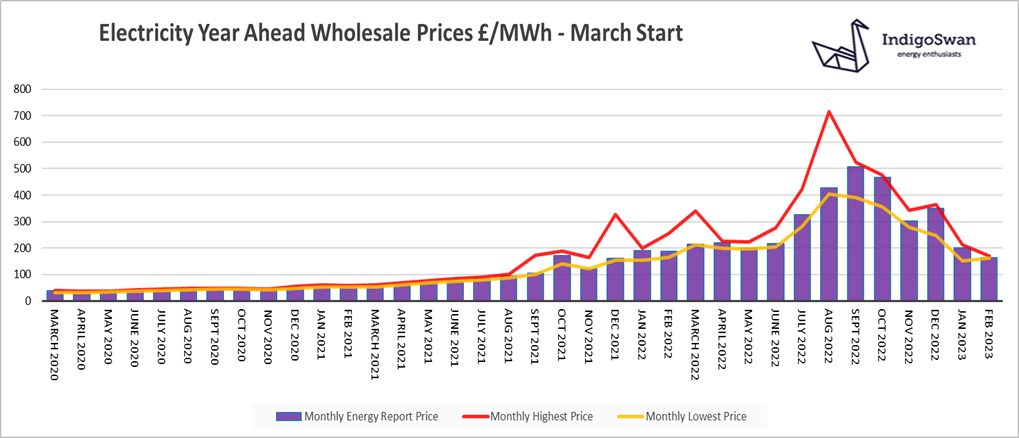

Electricity market overview

On the 6th of February, the Electricity Year Ahead Wholesale cost was £163.24/MWh, down from £201.84/MWh in last month’s report and down 13% on 2022. 2024 prices are similar.

Wind provided a very high 32% of supplies in January, higher than Gas at 30%. However, with Gas being the more reliable and expensive form of generation, its price determines the wholesale cost. The weather forecast does indicate periods of strong Wind at times in February, and has so far accounted for 32%.

Imports from the continent increased to 11% of supplies in January, with the availability of returning French Nuclear reactors and Electricity from Norway, Netherlands and Belgium. This was despite strike action in France which is likely to continue and may potentially restrict additional supplies to the UK at times of peak demand, requiring expensive interventions.

The National Grid has mechanisms in place to help avoid power shortages and has taken additional steps to make Coal generation available on demand. These measures do come at a cost premium, in the form of higher third-party charges within bills, but provide an element of stability to prices which otherwise may react even more dramatically.

Let us know if you would like us to research your options for 12, 24 and 36 month contracts.

If you enjoyed reading this blog why not try on of our others: