Headlines:

- Gas and Electricity Wholesale prices are lower

- EU Gas Storage levels are 58% full

- Large numbers of LNG shipments to Europe

Energy Overview

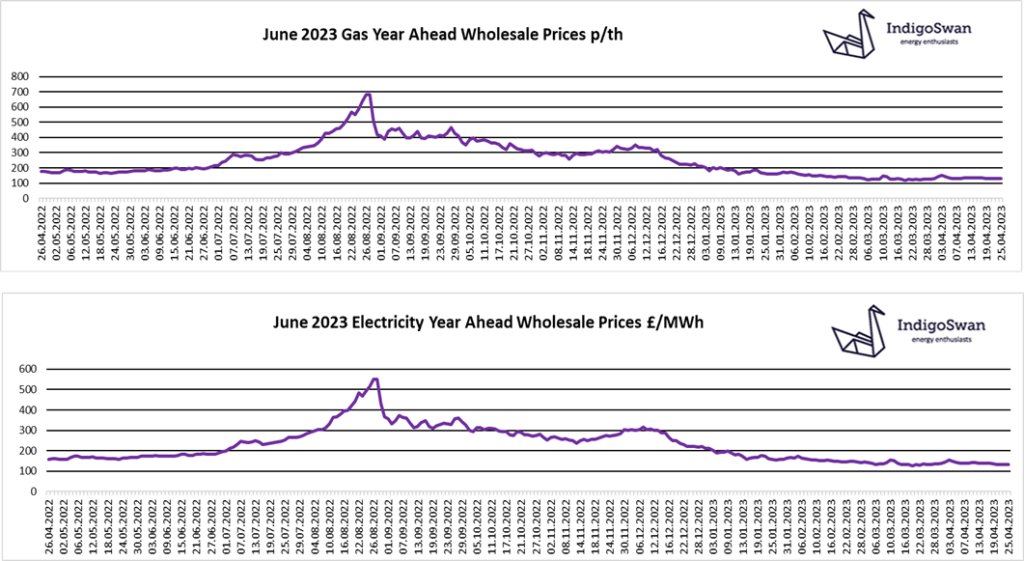

Since our last Energy Report, Gas and Electricity Year Ahead Wholesale prices are lower.

The supply position for Gas across the EU continues to be positive, with Storage levels at 58% full against a target of 90% by November 2023, and compared to just 30% the last two years. During the warmer months when Gas demand should be lower, there will be a conscious effort to divert supplies into Storage, providing an additional upward price pressure. Large numbers of LNG shipments continue to arrive in Europe to replace the reduced Russian Gas flows. Some of these may begin to head towards Asia as the Chinese economy grows beyond expectations.

The cost of Gas as a fuel for generation remains the most influential driver for Electricity’s price direction. Over the last week we have seen a reduced need for Gas, as Wind’s contribution increased to 26% from 19% the week before, and Electricity Imports from the continent were also up at 15% from 11%. There is an ongoing concern as to the reliability of imports from France, with industrial action threatening to delay the maintenance of their Nuclear reactors, where issues continue to be found.

Wholesale prices are currently in the region of a fifth of the peaks we saw in 2022, but still show a premium against 2020 and early 2021. It is generally considered unlikely that we will see those low levels for some time. There has been little price movement over the last four months, although there is a downward trend. Concern remains that an unexpected event, which has not been factored into costs, could once again see increases. Therefore, we would advise discussing your options for contracts ending in 2023 with Indigo Swan.

If you enjoyed reading this blog, why not try one of our others: