Headlines:

- Gas and Electricity Wholesale prices are lower than last week

- EU Gas Storage levels are a healthy 76% full

- LNG deliveries continue to arrive in Europe

Energy Overview

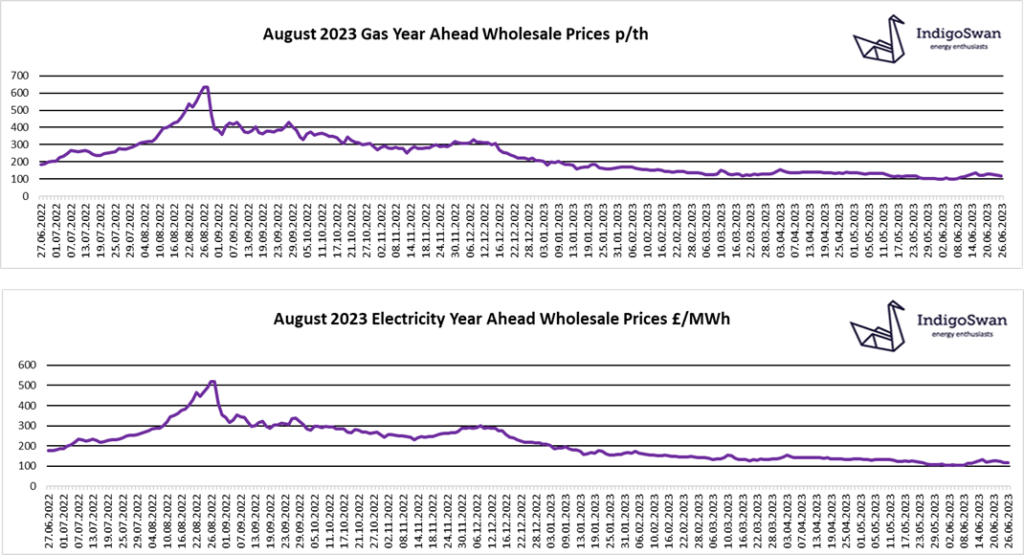

Over the last week Gas and Electricity Wholesale prices are down slightly, although up since early June.

We are in a much more positive position than this time last year, when there were concerns that a shortage of Gas, due to reduced flows from Russia, may mean some restrictions in use through the winter. With the EU setting a target for Gas Storage levels to be 90% full by November and currently being a high 76%, energy markets are assuming supplies will be sufficient, unless there are further issues. Less LNG deliveries are being made to the UK due to our low Storage capacity, but they continue to head to Europe despite competition from Asia.

The recent period of high temperatures increased Electricity demand due to the need for cooling. We have also seen periods of very low Wind contribution, requiring more Gas generation as well as Coal. Imports from the continent are an important part of our energy supply mix, but these can be unreliable as we have seen over the last year, with French Nuclear reactors being taken offline due to safety issues and low water levels potentially restricting Hydro supplies from Norway via the North Sea Link.

Wholesale prices are in the region of 60% lower than June 2022 but we continue to see large daily % swings, which underlines the high degree of uncertainty. There is a premium against 2020 and early 2021 prices and it is generally considered unlikely that we will see those low levels for some time. With little price movement in recent months, concern remains that an unexpected event, which has not been factored into costs, could once again see increases. Therefore, we would advise discussing your options for contracts ending in 2023 with Indigo Swan.

If you enjoyed reading this blog, why not try one of our others: