Headlines:

- Gas and Electricity Wholesale prices are lower

- Prices are struggling to find direction with daily swings

- EU Gas Storage levels remain high at 85% full

Energy Overview

As of the 1st of August, Gas and Electricity Year Ahead Wholesale costs were lower when compared to last month’s report.

EU Gas Storage levels are a very positive 85% full, up from 78% last month. The expectation is that the target of 90% by November will be exceeded. 2022 saw concern that there may be Gas shortages during the winter, which caused much of the price volatility. The level of confidence for winter 2023/24 remains a significant influence. Any indications of extended periods of below average temperatures or Gas supply disruptions, including those piped through Ukraine, may increase LNG competition between European and Asian markets.

Electricity prices are following Gas, as it is the main source of generation. We do have a growing diversity of supplies, which includes renewables and connections to the continent, but they are not yet able to match the scale and reliability of Gas generation.

The Oil price has increased from $75 a barrel to $85, showing that the production cuts by OPEC+, whose members include Saudi Arabia and Russia, are having an impact.

The Met Office forecast for August suggests temperatures are likely to be below seasonal norm.

What does this mean for me?

The Energy Bills Discount Scheme (EBDS) replaced the Energy Bill Relief Scheme (EBRS) on the 1st of April 2023. It is designed to give all non-domestic customers, including the voluntary sector (such as charities) and the public sector (such as schools and hospitals) access to a phased in maximum discount when the customer’s wholesale cost exceeds the defined thresholds. This lasts for 12 months until 31st of March 2024 and applies to contracts that were put in place on or after 1st of December 2021 and non-contracted arrangements. As with the EBRS, energy suppliers will automatically apply these standard discounts. The levels of assistance are less generous, but the price of Gas and Electricity is considerably lower than 2022. Those companies that are classed as Energy and Trade Intensive Industries (ETII) and Heat Networks, had to apply in July to receive a more attractive discount.

Customers may have started to see higher Standing Charges on their Electricity invoices from 1st of April 2023. There have been changes to the way some industry charges are calculated, under the Targeted Charging Review. This move is part of an attempt to recover more Electricity costs, such as Transmission and Balancing, through fixed fees. In theory this should give both the customer and the industry a more accurate way of managing finances.

Indigo Swan are working closely with energy suppliers to help all our customers understand and manage these changes.

Please contact us on 0333 320 0475 to discuss options or to get a latest update.

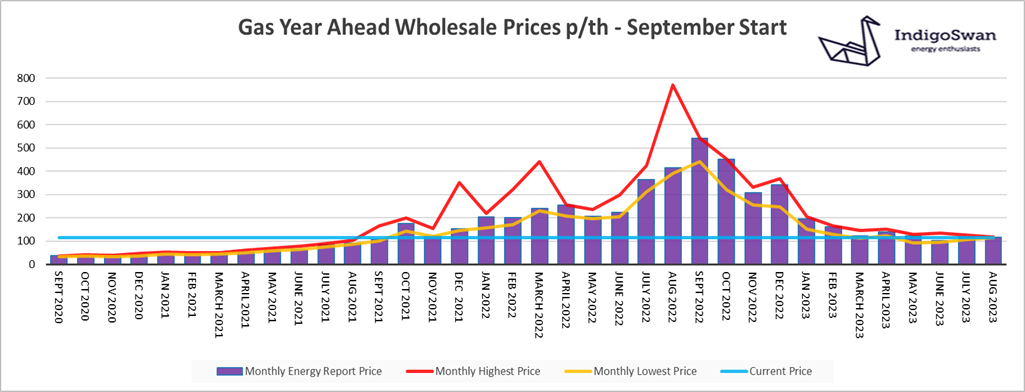

Gas market overview

On the 1st of August, the Gas Year Ahead Wholesale cost was 115.47p/th, down from 119.67p/th in last month’s report and 72% less than 2022.

Gas Wholesale prices continue to show a lack of direction, although we are seeing daily price swings. Any news which is thought may impact on winter supplies is having an exaggerated effect. Although small when compared to the extreme volatility in 2022, the impact on a company’s budgets can still be significant. It is currently being assumed that we will have normal temperatures this winter and that there are no interruptions to imports into the continent or unplanned closures of infrastructure.

EU Gas Storage is currently 85% full, higher than had been anticipated when the target of 90% was set for November. This has resulted in less demand for LNG and shipments to the UK and Europe, a position which could change should temperatures require more cooling or heating, either here or in Asia. The Groningen Gas field is closing by the 1st of October 2023, earlier than expected due to safety concerns. The Dutch government has said it could be utilised for one more year in the event of a Gas supply emergency.

Energy suppliers are now offering a wider range of contracts so we would advise discussing your options for contracts ending in 2023 or early 2024 with Indigo Swan, for both one and two years.

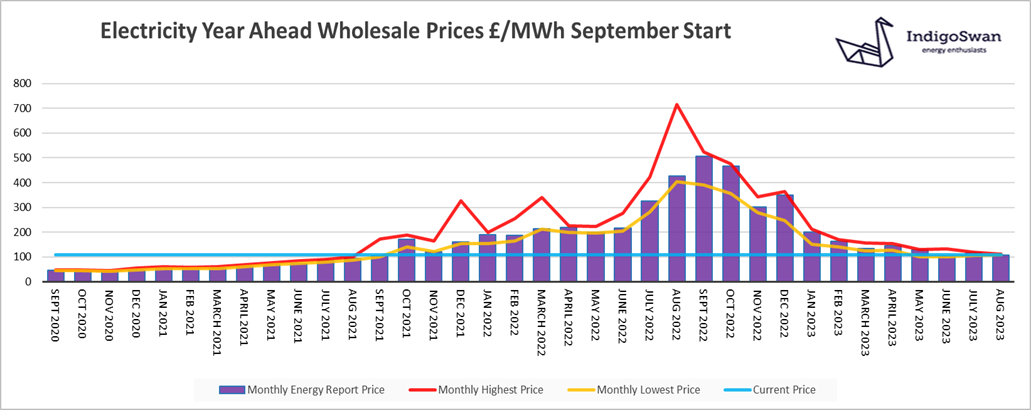

Electricity market overview

On the 1st of August, the Electricity Year Ahead Wholesale cost was £107.98/MWh, down from £118.00/MWh in last month’s report and 75% less than 2022.

Electricity demand in July was roughly 10% lower than 2022, which is partly due to the cooler temperatures and less air conditioning, although this would also mean a reduced Solar contribution. It is also likely that the lower energy use is part of the trend to reduce carbon emissions and a forced change in habits as a way of avoiding some of the impact of higher Gas and Electricity costs.

Wind accounted for an improved 24% of supplies compared to 16% in June, which allowed for a reduction in the use of expensive Gas at 32% from 39%. Electricity Imports from Europe were slightly down at 12%.

The National Grid has mechanisms in place to help avoid power shortages and has taken additional steps to secure generation on demand. These measures do come at a cost premium, in the form of higher third-party charges within bills, but provide an element of stability to prices which otherwise may react even more dramatically. Their early winter lookout report which is based on the current understanding of supply and demand, forecasts we should have enough Electricity by continuing to use some Coal and the Demand Flexibility Service.

Let us know if you would like us to research your options for one and two years, for contracts ending in 2023 or early 2024.

If you enjoyed reading this blog why not try one of our others: