Headlines:

- Gas and Electricity Wholesale prices are lower than last week

- EU Gas Storage levels are a high 65% full

- Global events may still create price volatility

Energy Overview

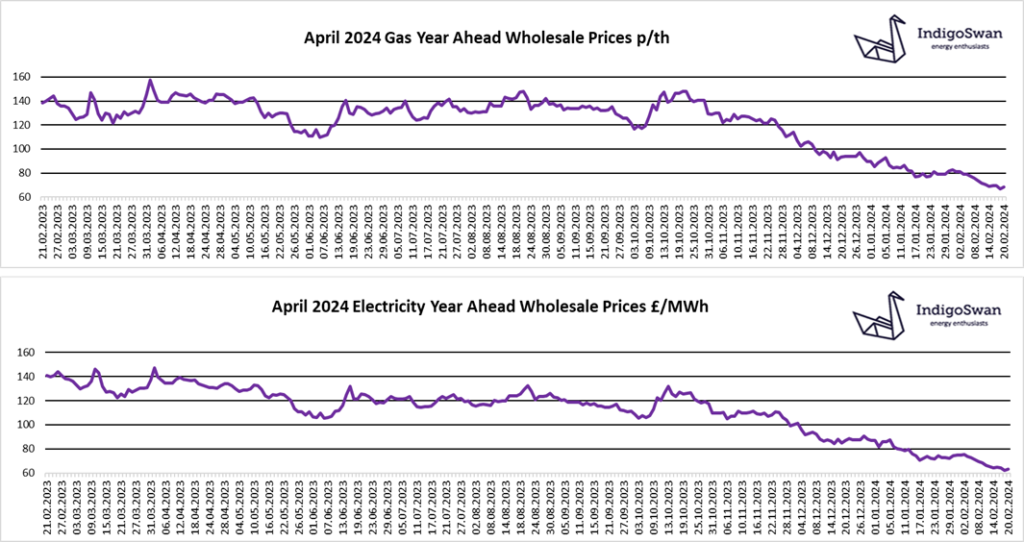

Gas and Electricity Wholesale costs are lower than last week.

Although EU Gas Storage levels have declined, they are still 65% full as we head towards the end of the winter period. This is a positive position, which is comparable to last year but significantly higher than 2021 and 2022. As heating demand reduces, Gas will be diverted to Storage for this coming winter, with an EU target of 90% full by November. LNG deliveries continue to arrive, although some are delayed due to the longer journey, which avoids the Red Sea and the threat to shipping. The recent milder temperatures have meant a lower Gas demand, but they are dropping below seasonal norm this week.

Gas for generation was lower last week at 27% from 33% the previous, partly due to a higher Wind contribution at 29% and an increase of imports from the continent through the Electricity Interconnectors. This has allowed for less use of Coal, which will be coming to an end shortly, nearly 150 years after first producing power in the UK.

Wholesale prices for a twelve-month contract are almost at a three-year low and approaching what would now be regarded as the norm, prior to the start of reduced Gas flows from Russia into Europe. There is a small premium for longer term contracts due to various uncertainties. We have been fortunate that with tighter Gas supplies, we have not yet had a prolonged period of very cold temperatures, and the possibility remains that the tensions in the Middle East could yet impact on Oil and LNG shipments from the region. We would advise discussing your options for contracts ending in 2024 or at least monitoring the position closely.

If you enjoyed reading this blog, why not try one of our others: