Headlines:

- Gas and Electricity Wholesale prices are unchanged from last week

- EU Gas Storage levels are a high 64% full

- Global events may still create price volatility

Energy Overview

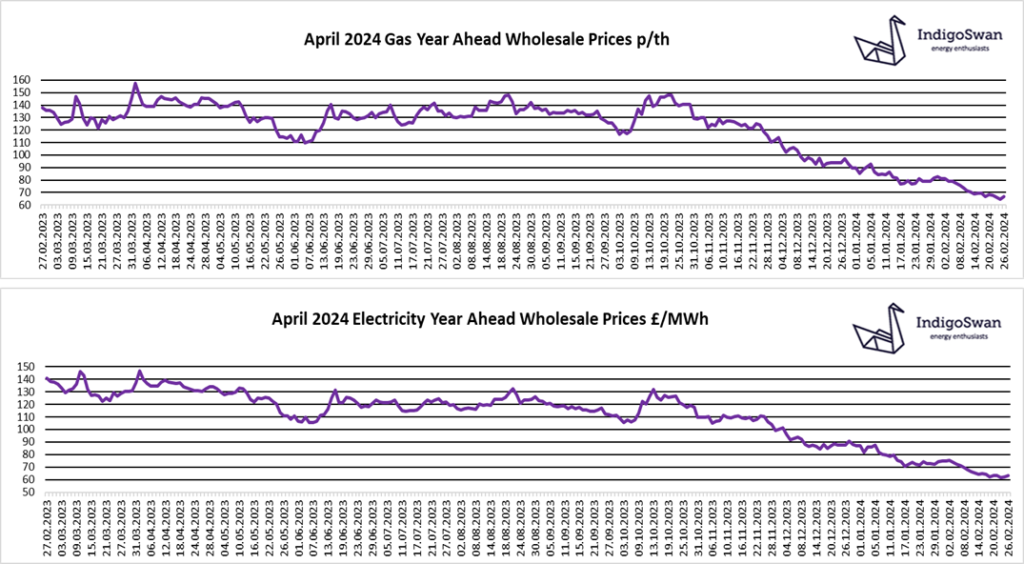

Gas and Electricity Year Ahead Wholesale costs are the same as last week despite initial losses. There is a small premium for longer term contracts due to various uncertainties.

EU Gas Storage levels remain high at 64% full, which is a small improvement on last year. Based on historic trends and assuming there is no prolonged period of low temperatures or supply disruptions, we would expect Storage to be in the region of 56% full, before injections begin mid to late March, with the target of 90% by November. This positive position is reflected in the steady decline of Gas prices, which are now at their lowest in almost three years, prior to the reduction of Gas flows from Russia into Europe.

Our continued reliance on Gas for generation, means that Electricity prices follow very closely. Gas contributed 28% last week compared to 38% in January. Wind was 26%, although we saw a daily low of 3%, which underlines the erratic nature of Renewables. With an increased demand due to the cold spell, we imported a very high 20% from the continent through the interconnectors.

The tensions in the Middle East still have the potential to disrupt Oil and Gas supplies. So far this has been restricted to longer delivery times as ships avoid the shorter route through the Red Sea and the Suez Canal. Any supply reductions could see the return of price volatility.

We would advise discussing your options for contracts ending in 2024 or at least monitoring the position closely.

If you enjoyed reading this blog, why not try one of our others: