Headlines:

- Gas and Electricity Wholesale prices are slightly higher than last month

- Prices continue to react to small changes in supply and demand

- EU Gas Storage levels are a high 61% full

Energy Overview

As of the 11th of March, Gas and Electricity Year Ahead Wholesale costs were higher than those in last month’s report.

A downward price trend saw prices reach an almost three year low in February, before a small amount of volatility returned in March as evening temperatures fell, creating an additional heating demand. The current milder weather has seen prices ease again, which demonstrates the nervousness that the industry feels as thoughts turn to winter 2024/25 and the availability of Gas.

The EU’s Gas Storage levels are 61% full, an improvement on the 57% last year, and far higher than 2021 and 2022 when there were fears that shortages could result in supply restrictions to business customers and Electricity generators. LNG deliveries continue to arrive in Europe from global sources, compensating for the reduced Russian Gas flows since tensions began in 2021.

Although Renewable assets are increasing, there is still a heavy reliance on Gas as a flexible form of generation. It can react to additional peak demand or replace lower contributions from the likes of Wind or Nuclear. In February the use of Gas for generation fell to just 28% of Electricity supplies, down from 38% in January. This was due to higher Wind and Interconnector contributions.

What does this mean for me?

The Energy Bills Discount Scheme (EBDS) replaced the Energy Bill Relief Scheme (EBRS) on the 1st of April 2023. It is designed to give all non-domestic customers, including the voluntary sector (such as charities) and the public sector (such as schools and hospitals) access to a phased in maximum discount when the customer’s wholesale cost exceeds the defined thresholds. This scheme lasts for 12 months until 31st of March 2024 and applies to contracts that were put in place on or after 1st of December 2021 and non-contracted arrangements. As with the EBRS, energy suppliers will automatically apply these standard discounts. The levels of assistance are less generous, but the price of Gas and Electricity is considerably lower than 2022. Those companies that are classed as Energy and Trade Intensive Industries (ETII) and Heat Networks, need to apply to receive a more attractive discount.

Since April 2023, customers may have seen higher Standing Charges on their Electricity invoices. There have been changes to the way some industry charges are calculated, under the Targeted Charging Review. This move is part of an attempt to recover more Electricity costs, such as Transmission and Balancing, through fixed fees. In theory this should give both the customer and the industry a more accurate way of managing finances. More changes are due.

Indigo Swan are working closely with energy suppliers to help all our customers understand and manage changes.

Please contact us on 0333 320 0475 to discuss options or to get a latest update.

Gas market overview

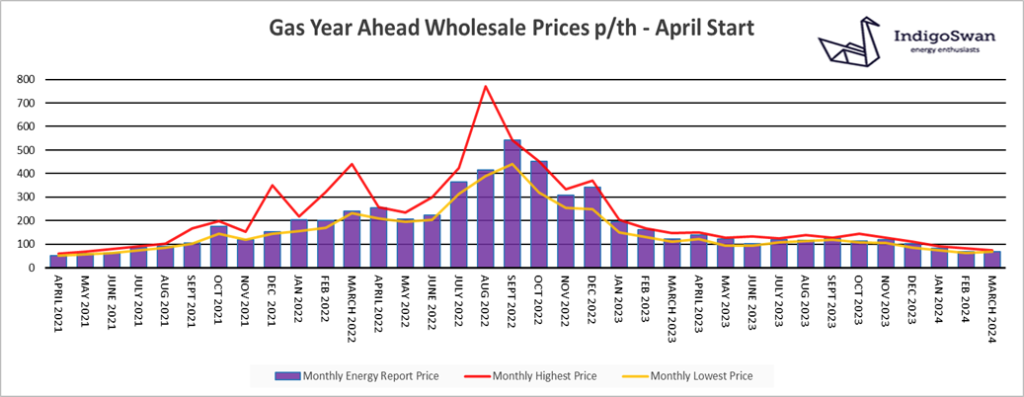

On the 11th of March, the Gas Year Ahead Wholesale cost was 69.43p/th, up from 69.00p/th in last month’s report and 43% less than 2023.

The availability of LNG supplies will continue to be a key price driver for Gas and Electricity. The tensions in the Middle East threaten shipping passing through the Suez Canal via the Red Sea. So far this has just been an inconvenience for LNG, with delays due to a longer route to avoid a major incident. The US is now the largest exporter of LNG, which Europe has become heavily reliant on. However, their high production costs compared to Qatar has forced a large US Gas producer to announce supply cuts due to falling prices. There is also the potential for US government intervention for any new export projects, to consider the impact on domestic energy costs and carbon emissions. Qatar has outlined plans to increase production to capitalise on a growing global demand.

The high levels of EU Gas Storage at 61% full is providing a degree of optimism that the target to replenish stocks to 90% full by November can be met, in readiness for winter 2024/25. With the delicate balance between supply and demand, any number of events could still have an impact on prices, such as further developments in the Middle East, resulting in the cancellation of Gas shipments. Europe has been extremely fortunate that since Gas shortages began in 2021, there has not been a period of prolonged extremely cold temperatures, which still has the potential to create price spikes.

We would advise discussing your options for contracts ending early 2024 or at least monitoring the position closely.

Electricity market overview

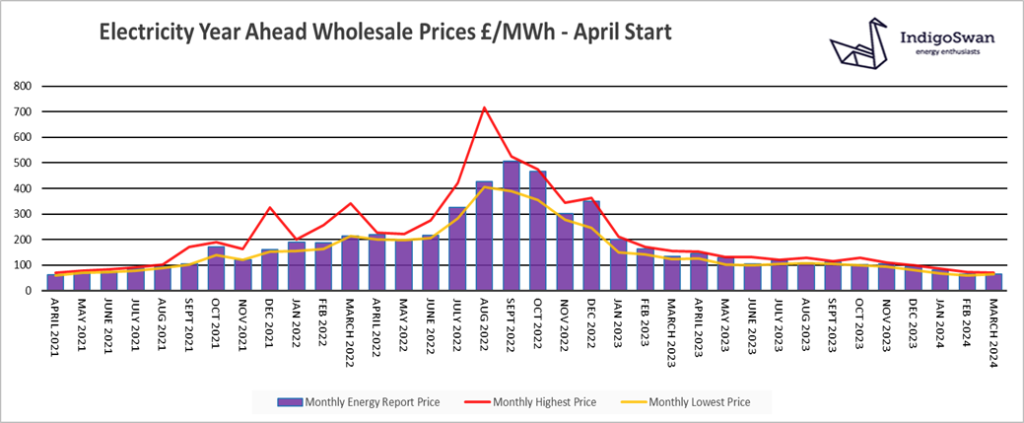

On the 11th of March, the Electricity Year Ahead Wholesale cost was £65.06/MWh, up from £64.39/MWh in last month’s report and 51% less than 2023.

Electricity prices continue to follow Gas as it contributed 28% of generation in February and 29% over the last week, which is low when compared to previous periods. This is partly due to an increase in Wind at 30% in February and the growing availability of Electricity through the Interconnectors with Europe. Coal is still being used to help balance the network, although we are looking to close the last power station by October 2024. With the erratic nature of Renewables, the government has highlighted the need to build new Gas generation to replace ageing assets, despite objections.

Within the last month we did see a small amount of volatility, which underlines the potential for price increases in 2024. Due to the close relationship between Gas and Electricity, any disruption to LNG supplies resulting from tensions in the Middle East or further production issues in the US, will impact on Electricity prices. There have also been historic issues with imported French Nuclear supplies, although the number of Interconnectors from various sources now means this should have less of an impact on us.

Wholesale prices are near a three year low and having recently seen market nervousness and price increases, we would advise discussing your options for contracts ending in 2024 or at least monitoring the position closely.

If you enjoyed reading this blog why not try one of our others: