Headlines:

- Gas and Electricity Wholesale prices are higher than last week

- EU Gas Storage levels are a high 60% full

- Global events may still create price volatility

Energy Overview

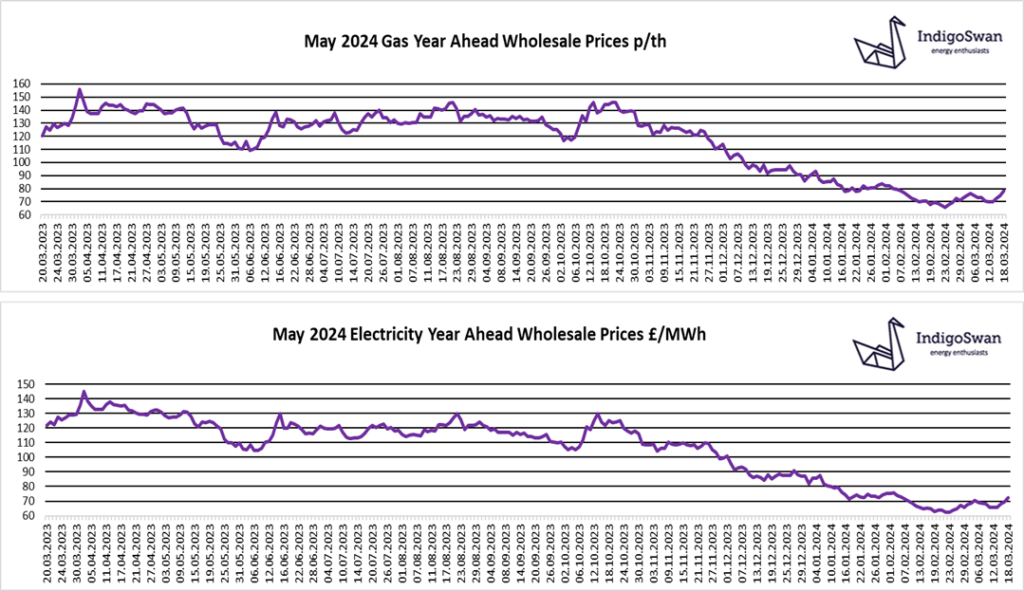

Gas and Electricity Year Ahead Wholesale costs are higher than in last week’s report. There is a small premium for longer term contracts due to various uncertainties.

Since the reduction of Gas flows from Russia into Europe, there has been pressure to find alternate sources and reduce energy use. Despite the price volatility which peaked late 2022, the mild winters have meant that there has not been the disruption to customers that had been feared. LNG shipments have helped compensate for the shortfall of Gas, allowing the EU to fill Storage to near capacity before peak winter demand. However, the position does mean there is little to spare and any actual or potential threat to supplies is having an exaggerated impact on Wholesale markets.

EU Gas Storage levels are currently a high 60% full, compared to 56% last year and 26% in 2022. Their target is 90% by November 2024. This has given the industry confidence, and prices are in the region of three-year lows. Wind has contributed 29% of our Electricity so far this year, but its erratic nature means we are still reliant on Gas for baseload generation and to meet any shortfalls. The growing number of Electricity Interconnectors with Europe allows us to Import and Export, providing us with 21% of supplies over the last week.

Recent unplanned Gas outages and the possibility of a colder spell have resulted in a small price spike, which underlines how sensitive the industry is to global events. We would advise discussing your options for contracts ending in 2024 or at least monitoring the position closely.

If you enjoyed reading this blog, why not try one of our others: