Headlines:

- Gas and Electricity Wholesale prices are higher than last week

- EU Gas Storage levels are a high 59% full

- Any new supply concerns may still create price volatility

Energy Overview

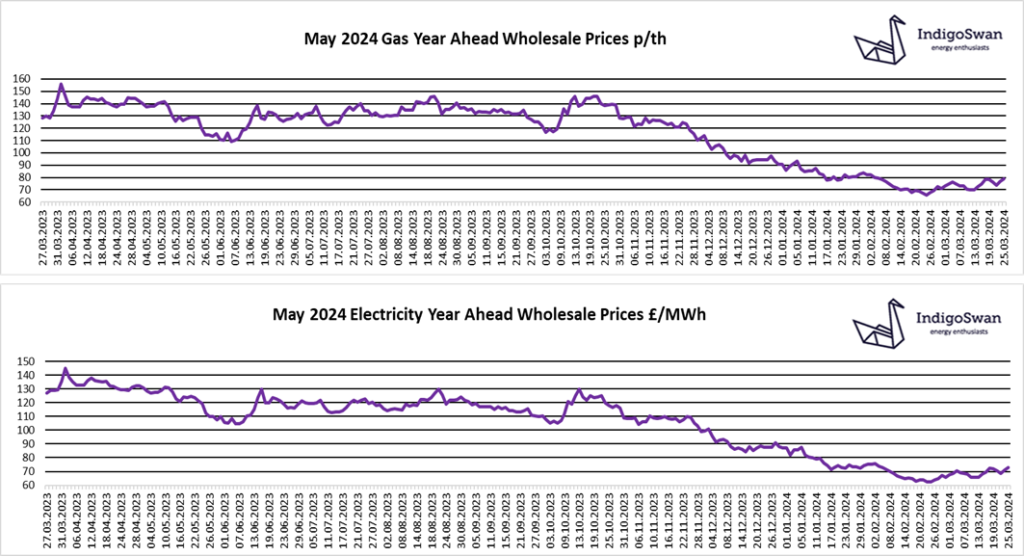

Gas and Electricity Year Ahead Wholesale costs are higher than in last week’s report. There is a small premium for longer term contracts due to various uncertainties.

Since prices hit their low point towards the end of February, they have struggled to find direction, showing up to 4% daily swings. These have been triggered by small supply issues, either from LNG, Gas imports from Norway or Nuclear outages. Any forecast of a cold spell is also seeing a market reaction. This level of nervousness does mean that a larger event could see the return of more volatility.

EU Gas Storage levels are a high 59% full compared to 56% last year, which is a significant reason why prices have fallen to an almost three year low. Gas will soon start to be injected into Storage, aiming to reach and likely exceed the EU’s 90% target by November, in readiness for winter’s demand.

Over the last week, the contribution of Gas for generation has been suppressed at 25% of supplies, by high levels of Wind at 30% and Imports from Europe at 18%. As we rely so heavily on Gas to help meet baseload demand and also be available to replace unreliable renewables, it dictates the price direction of Electricity.

Electricity Distribution and Transmission charges are changing from April 2024, showing both increases and decreases, which may overall have little impact for many.

We would advise discussing your options for contracts ending in 2024 or at least monitoring the position closely.

If you enjoyed reading this blog, why not try one of our others: