Headlines:

- Gas and Electricity Wholesale prices are higher than last month

- Wholesale prices are trending upward

- EU Gas Storage levels are a high 64% full

Energy Overview

As of the 7th of May, Gas and Electricity Year Ahead Wholesale costs were higher than those in last month’s report.

Through April and into early May, prices have continued to show volatility with a swing of 25% for Gas, which although significant, they are still much lower than we have seen in recent years.

The filling of EU Gas Storage stalled in April due to a period of lower temperatures, requiring additional heating demand. Injections have since resumed and Storage is currently 64% full, compared to 61% last year and against a 90% target by November.

Some of the price pressures have eased. The risk of further military action between Iran and Israel has lowered, which had the potential to cause disruptions to Gas and Oil supplies from the region. Russia has also been targeting Ukraine’s energy industry, but the huge new US aid package for Ukraine may have an impact.

Despite there being more Renewable assets, there remains a need for Gas to provide a reliable source of generation and has the flexibility to react to peak demand or replace lower Wind and Solar. In April, Gas use for generation reduced to just 18% of Electricity supplies, down from 26% in March. This was due to the high contributions from various other sources.

What does this mean for me?

The Energy Bills Discount Scheme (EBDS) ended on 31st March 2024. It was designed to give all non-domestic customers, including the voluntary sector (such as charities) and the public sector (such as schools and hospitals) access to a phased in maximum discount when the customer’s wholesale cost exceeded the defined thresholds. Suppliers automatically applied discounts. The price of Gas and Electricity has fallen considerably since the scheme’s introduction. Those companies classed as Energy and Trade Intensive Industries (ETII) and Heat Networks, had to apply to receive a more attractive discount.

Over the last few years, the energy industry has changed the way it recovers Distribution, Transmission and Balancing costs, under the Targeted Charging Review. This has resulted in moving some charges away from being based on the energy used and billed in the unit rate, to fixed charges incorporated within the Standing Charge. In theory this should give both the customer and the industry a more accurate way of managing finances, but the increases have become more noticeable within energy bills and give less scope to reduce costs through energy management. From April 2024 it is expected most customers will see a reduction in Electricity Distribution costs over the next year, but higher Transmission charges. Balancing costs will be lower for six months, before increases are expected from October 2024.

Indigo Swan are working closely with energy suppliers to help all our customers understand and manage changes.

Please contact us on 0333 320 0475 to discuss options or to get a latest update.

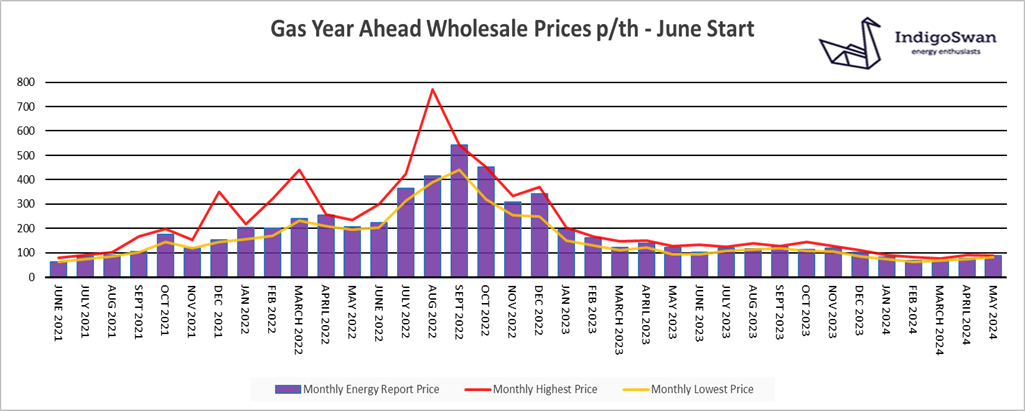

Gas market overview

On the 7th of May, the Gas Year Ahead Wholesale cost was 87.79p/th, up from 76.54p/th in last month’s report and 27% less than 2023.

EU Gas Storage levels are a high 64% full, compared to 61% last year and 30% the previous two years when there were concerns that a period of very cold temperatures could create shortages, resulting in targeted restrictions for some consumers. It is likely that as long as there are no significant disruptions to supplies or surges in demand, that the 90% full target will be met by November. The status of EU Gas Storage is a key price driver for both Gas and Electricity Wholesale costs.

LNG deliveries continue to arrive although at lower levels. This is partly due to an outage at the US Freeport LNG plant and increased piped flows from elsewhere, but also the healthy Gas Storage levels in the EU which reduce the appetite to compete with the Asian market, where demand has increased. As countries look to move away from burning Coal and use less reliable Renewables, their need for LNG is expected to increase. Therefore, the policies and investments of exporters such as the US, Qatar and Australia will influence prices, similar to OPEC+ for Oil.

The EU has already given member states the right to ban imports of Gas from Russia, but they are considering sanctions to ban LNG imports for all, where the Gas is resold outside the EU. There could well be opposition from Hungary, which has close ties with Russia.

We would advise discussing your options for contracts ending in 2024 or at least monitoring the position closely.

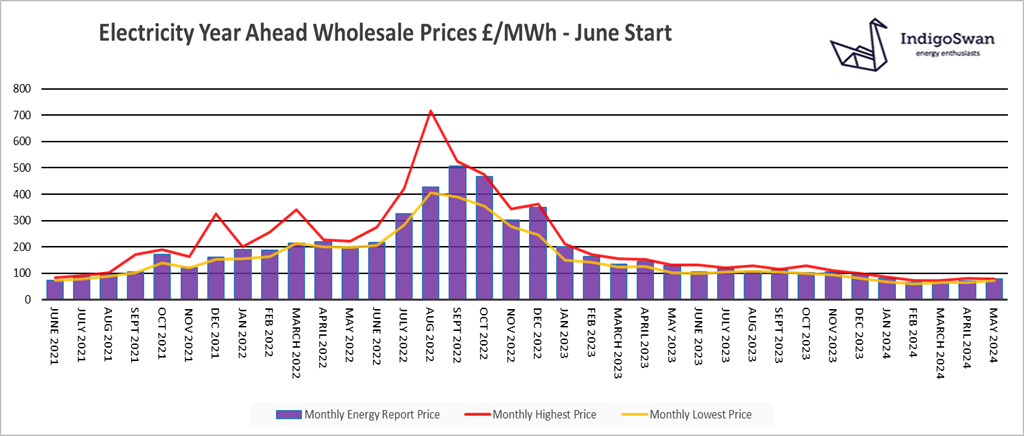

Electricity market overview

On the 7th of May, the Electricity Year Ahead Wholesale cost was £77.12/MWh, up from £70.07/MWh in last month’s report and 40% less than 2023.

April saw a lower contribution from Gas for generation at 18%, down from 26% in March. Wind increased to 30% from 28% and imports from Europe were down slightly at 17%. The last week has seen reduced Wind and an increase in the use of Gas.

With Gas being a large source of our Electricity and one which can be used to balance the network, increasing or decreasing depending on the performance of Renewables, it dictates the price of Electricity. This means that in most cases, price movement is related to global events. These include the reduced Gas flows from Russia, tensions in the Middle East with the potential impact on LNG, and also the levels of Gas Storage in both the UK and EU, which supports the additional winter demand.

To help reduce the need for Gas, significant investment will be needed to move power across the UK, linking Wind and Solar farms to areas of high demand. Ideally, we should be able to store surplus Renewables to provide another option to help at times of peak use, but at this time the projects are small scale.

We would advise discussing your options for contracts ending in 2024 or at least monitoring the position closely.

If you enjoyed reading this blog why not try one of our others: