Headlines:

- Gas and Electricity Wholesale prices are lower than last week

- EU Gas Storage levels are a positive 64% full

- There remains the potential for price volatility

Energy Overview

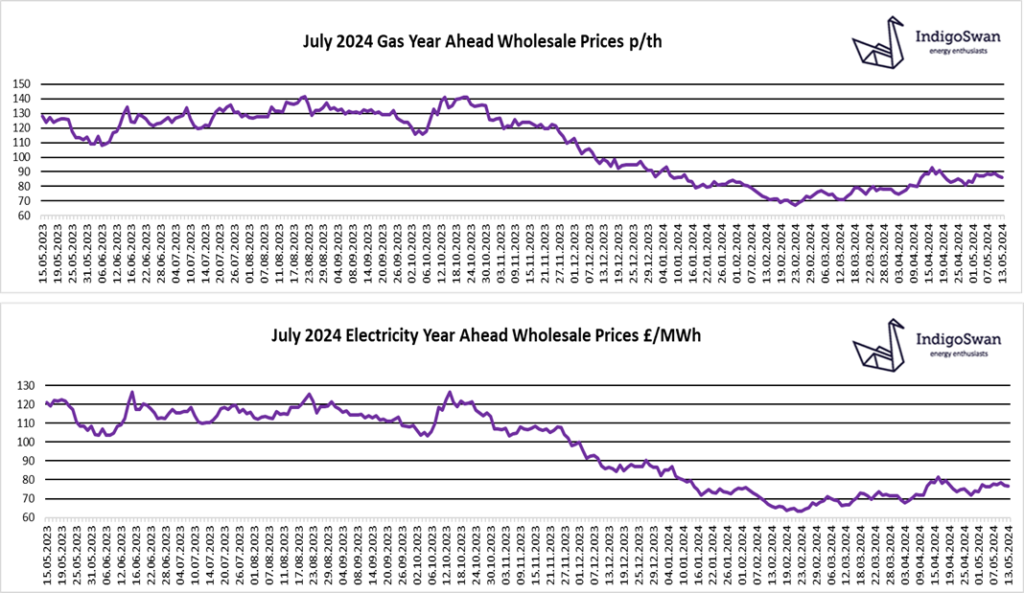

Gas and Electricity Year Ahead Wholesale costs are lower than in last week’s report.

The lack of clear direction continued through last week with further increases before easing on Friday and Monday. There was little reason for the daily spikes as the supply outlook is positive, which is reflected in the significant price reductions on recent years. This does mean there may be greater volatility in the event of further disruptions to supplies or a surge in demand from unseasonal temperatures, whether that be heating or air conditioning. It could mean that for now, the Wholesale price has little scope for decreases, although lower costs for 2026 show there is also the potential for better value.

Injections into EU Gas Storage have resumed and are currently 64% full, compared to 63% last year and 38% in 2022. This is a positive position which gives confidence that the 90% target by November can be reached and likely surpassed. Gas Storage provides additional energy security, especially for heating through the winter.

Wind contributed just 13% to generation last week, which meant the continued reliance on Gas to make up the shortfall and balance the network. Imports of Electricity through the growing number of Interconnectors with the continent, increased to 20% of supplies.

With energy markets reacting to any hint of supply or demand concerns, we would encourage customers that have Gas or Electricity contracts ending in 2024, to discuss options with Indigo Swan and closely monitor the position.

If you enjoyed reading this blog, why not try one of our others: