Headlines:

- Gas and Electricity Wholesale prices are higher than last month

- Wholesale prices are trending upward

- EU Gas Storage levels are a high 70% full

Energy Overview

As of the 3rd of June, Gas and Electricity Year Ahead Wholesale costs were higher than those in last month’s report.

The upward price trend continued through May and into June, although significantly lower than the highs we have seen in recent years.

Injections into EU Gas Storage have continued, now being 70% full, compared to 69% last year and 48% in 2022. The target is 90% by November, but as long as there are no significant issues, it is expected it should be 100% full, as we saw last year, before the higher winter demand.

Global events still add some pressure to Wholesale prices with fears that there could be disruptions to supplies. However, over the last month, it has been the planned and unplanned outages of supplies from Norway that have added concern. With Norway being the main Gas supplier to Europe following the reduced flows from Russia, we are seeing an exaggerated price reaction.

Electricity price increases are tending to be the result of Gas concerns. With it being a major and reliable source of generation, at 26% of supplies in May, it continues to dictate power price direction. This is unlikely to change in the short term, unless the government’s review of the Wholesale market reflects cheaper Renewable costs.

What does this mean for me?

The Energy Bills Discount Scheme (EBDS) ended on 31st March 2024. It was designed to give all non-domestic customers, including the voluntary sector (such as charities) and the public sector (such as schools and hospitals) access to a phased in maximum discount when the customer’s wholesale cost exceeded the defined thresholds. Suppliers automatically applied discounts. The price of Gas and Electricity has fallen considerably since the scheme’s introduction. Those companies classed as Energy and Trade Intensive Industries (ETII) and Heat Networks, had to apply to receive a more attractive discount.

Over the last few years, the energy industry has changed the way it recovers Distribution, Transmission and Balancing costs, under the Targeted Charging Review. This has resulted in moving some charges away from being based on the energy used and billed in the unit rate, to fixed charges incorporated within the Standing Charge. In theory this should give both the customer and the industry a more accurate way of managing finances, but the increases have become more noticeable within energy bills and give less scope to reduce costs through energy management. From April 2024 it is expected most customers will see a reduction in Electricity Distribution costs over the next year, but higher Transmission charges. Balancing costs will be lower for six months, before increases are expected from October 2024.

Indigo Swan are working closely with energy suppliers to help all our customers understand and manage changes.

Please contact us on 0333 320 0475 to discuss options or to get a latest update.

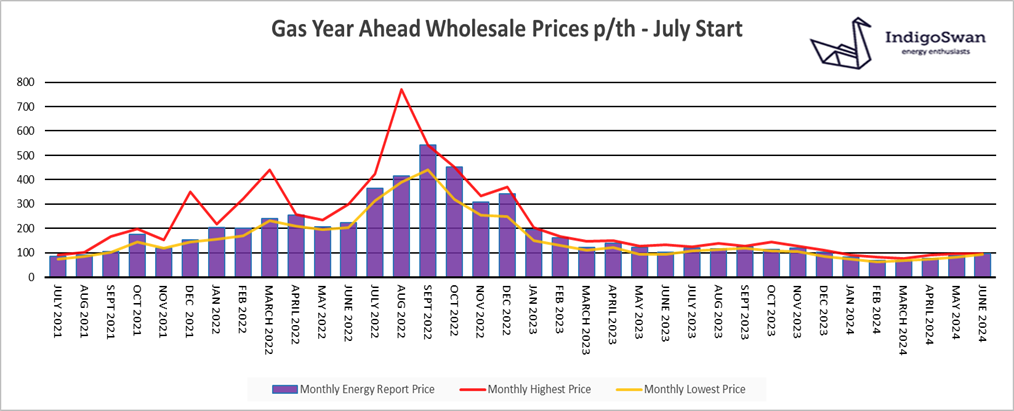

Gas market overview

On the 3rd of June, the Gas Year Ahead Wholesale cost was 97.67p/th, up from 87.79p/th in last month’s report but 5% less than 2023.

EU Gas Storage levels are a high 70% full, compared to 69% last year and 40% the previous two years, when there were concerns that a period of very cold temperatures could create shortages, resulting in targeted restrictions for some consumers. It is likely that as long as there are no significant disruptions to supplies or surges in demand, that the 90% full target will be met by November. The status of EU Gas Storage is a key price driver for both Gas and Electricity Wholesale costs.

Gas price volatility has been driven by supply concerns. In May and June we have seen both planned and unplanned Norwegian Gas supply outages. This has created an element of nervousness due to the high dependence on supplies from Norway, since Russia reduced flows into Europe. There is also the possibility that legal action could result in Austria not paying Gazprom and being cut off. So far, the EU has placed little restriction on Russian Gas supplies, but pressure is now growing to put some kind of ban in place. Initially this could involve how EU members import LNG and pass onto other European states, but Germany and the Czech Republic are seeking something more significant, which is likely to be opposed by the likes of Austria and Hungary.

Since February, Wholesale prices have shown low levels of daily volatility, followed by decreases. However, the trend has been upward movement. Therefore, we would advise discussing your options for contracts ending in 2024 or at least monitoring the position closely.

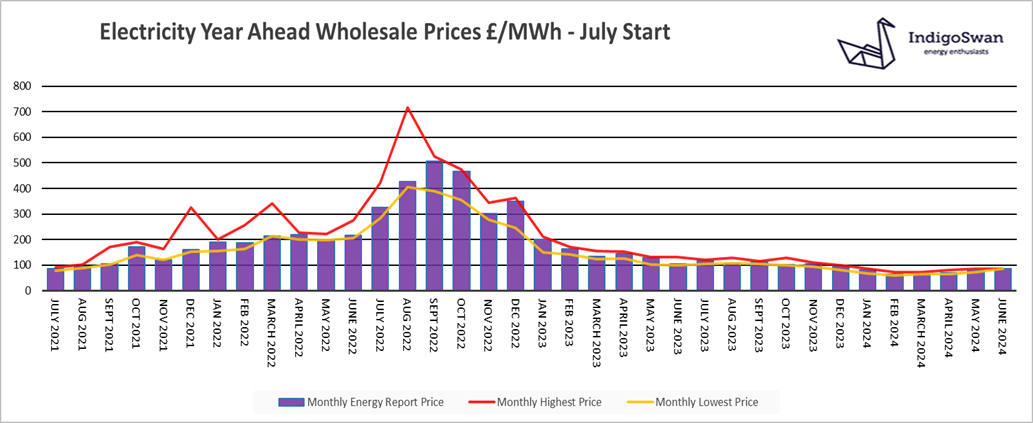

Electricity market overview

On the 3rd of June, the Electricity Year Ahead Wholesale cost was £87.39/MWh, up from £77.12/MWh in last month’s report but 18% less than 2023.

Gas contributed 26% of generation in May, up from 18% in April. With Gas costs rising, Electricity is following closely. Unplanned Norwegian Gas outages and the potential for Russian flows to be further reduced are causing concern. Gas Storage levels are healthy and it is hoped that LNG will continue to be available, despite competition from Asia.

Just 16% of Electricity came from Wind in May, down from 30%, which underlines the importance of Gas and Electricity Imports from the likes of Norway (Hydro) and France (Nuclear). Coal provided just 0.4%, but as this is due to end in 2024, we will lose what is a useful tool in balancing the network.

The UK has significant Renewable assets with many more projects in the pipeline, but connections have delays and their performance is erratic. The solution is a combination of innovative measures to help manage supply and demand and more investment, the bulk of which is being recovered through charges within Electricity bills.

Since February, Wholesale prices have shown low levels of daily volatility, followed by decreases. However, the trend has been upward movement. Therefore, we would advise discussing your options for contracts ending in 2024 or at least monitoring the position closely.

If you enjoyed reading this blog why not try one of our others: