Headlines:

- Gas and Electricity Wholesale prices are lower than last month

- Tight Gas supply margins are adding to the risk of price volatility

- EU Gas Storage levels are a high 77% full

Energy Overview

As of the 1st of July, Gas and Electricity Year Ahead Wholesale costs were lower than those in last month’s report, avoiding what would have been a fifth consecutive month of increases.

Injections into EU Gas Storage have continued, now being 77% full, comparable to 2023 but significantly higher than 2022 at 58%. The target is 90% by November and unless there are significant issues, are expected to reach 100%, as we saw last year.

Some of the risks for potential supply disruptions from Russia and the Middle East are being factored into prices as is the maintenance of Norwegian Gas assets from August. Europe has seen reduced LNG deliveries which have headed to Asia due to high temperatures and air-cooling demand, which look set to continue. Should European nations need more LNG they will likely need to pay a premium.

An upturn in Wind in June meant we used less Gas, which is an expensive but reliable source of generation and dictates the price direction for Wholesale Electricity. Consultations are ongoing as to how consumers can access lower Renewable costs, rather than paying the high market price set by Gas. There are various options being considered, which may become clearer after the general election.

What does this mean for me?

The energy industry has changed how it recovers Electricity Distribution, Transmission and Balancing costs, under the Targeted Charging Review. This has moved some charges away from being based on the energy used and billed in the unit rate, to fixed charges incorporated within the Standing Charge or as separate items. This should give both the customer and the industry a more accurate way of calculating budgets, but the change has become noticeable within energy bills and created concern. Over the next two years, there is a quite confused picture of increases and decreases in Transmission and Distribution charges, which energy suppliers will be billing customers.

From April 2024 most customers saw a decrease in Transmission which is likely to be followed by an increase in this fixed charge from April 2025, almost completely replacing what used to be recovered through Triads. Distribution costs are a little more complicated with the average fixed annual cost increasing across networks from April 2024 but decreasing from April 2025. Another element, the Available Capacity (AC), has already seen small increases but is due for a more significant rise from April 2025. This does mean that by managing the Agreed Supply Capacity, there is an opportunity to reduce the AC cost and longer term, potentially lower the Band which determines fixed charges.

Balancing costs were lower from April 2024, with increases expected from October 2024.

Indigo Swan work closely with energy suppliers to help all our customers understand and manage changes.

Please contact us on 0333 320 0475 to discuss options or to get a latest update.

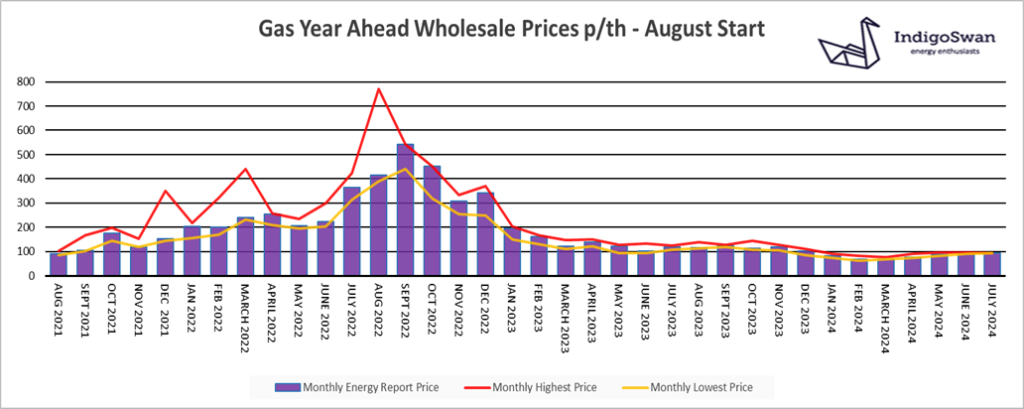

Gas market overview

On the 1st of July, the Gas Year Ahead Wholesale cost was 93.24p/th, down from 97.67p/th in last month’s report and 22% less than 2023.

EU Gas Storage levels continue to increase, currently at 77% full, the same as last year and much higher than 2022. The price volatility we saw in 2021 through to 2023 came from the concern that Europe would not have enough Gas to meet a high winter demand, following the reduction of flows by Russia. Through a combination of reducing demand and by sourcing Gas from elsewhere, some EU nations are now looking to place their own restrictions on Russian supplies. Although a complete EU ban on LNG is unlikely due to opposition, Finland’s state-owned company announced they will end Russian imports and pressure is growing from the likes of France for others to follow. This action may place further pressure on global resources.

The forecast for further high temperatures in Asia is attracting LNG deliveries due to their price premium. Norway, which is now Europe’s largest Gas supplier will see some scheduled maintenance in August which may force us to compete with Asia for LNG shipments.

Although the upward trend in Wholesale prices has stalled, there is still little evidence that we will see a significant downturn. It is more likely that, as we saw last summer, prices will continue to show low levels of volatility but avoid the price spikes seen in recent years. However, due to the tight global supply / demand relationship, any new event has the potential to impact on prices and so we would advise discussing your options for contracts ending in 2024 or at least monitoring the position closely.

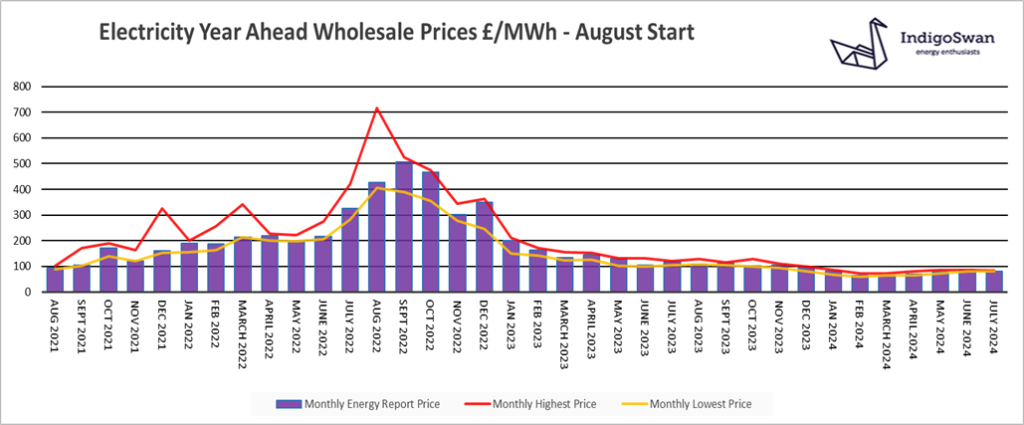

Electricity market overview

On the 1st of July, the Electricity Year Ahead Wholesale cost was £82.07/MWh, down from £87.39/MWh in last month’s report and 30% less than 2023.

The price of Gas remains the biggest influence on Electricity Wholesale prices and contributed 21% of generation in June, down from 26% in May. With EU Gas Storage being 77% full, this is providing an optimistic outlook for Gas supplies and has eased costs, but with Norwegian Gas supply outages in August and competition for LNG with Asia, there are potential pressures.

Wind provided an improved 20% last month, but this is still much lower than previous months which have seen in the region of 30%. This underlines the importance of Gas to be a flexible and reliable replacement for Renewables. Imports from the continent remained high at 22%. Coal provided just 0.1%, but as this is due to end in 2024, we will lose what is a useful tool in balancing the network.

Although the upward trend in Wholesale prices has stalled, there is still little evidence that we will see a significant downturn. It is more likely that, as we saw last summer, prices will continue to show low levels of volatility but avoid the price spikes seen in recent years. However, due to the tight global supply / demand relationship any new event has the potential to impact on prices and so we would advise discussing your options for contracts ending in 2024 or at least monitoring the position closely.

If you enjoyed reading this blog why not try one of our others: