Headlines:

- Gas and Electricity Wholesale prices are lower than last week

- We have seen a slight downturn in Wholesale prices since June

- EU Gas Storage levels are a positive 81% full

Energy Overview

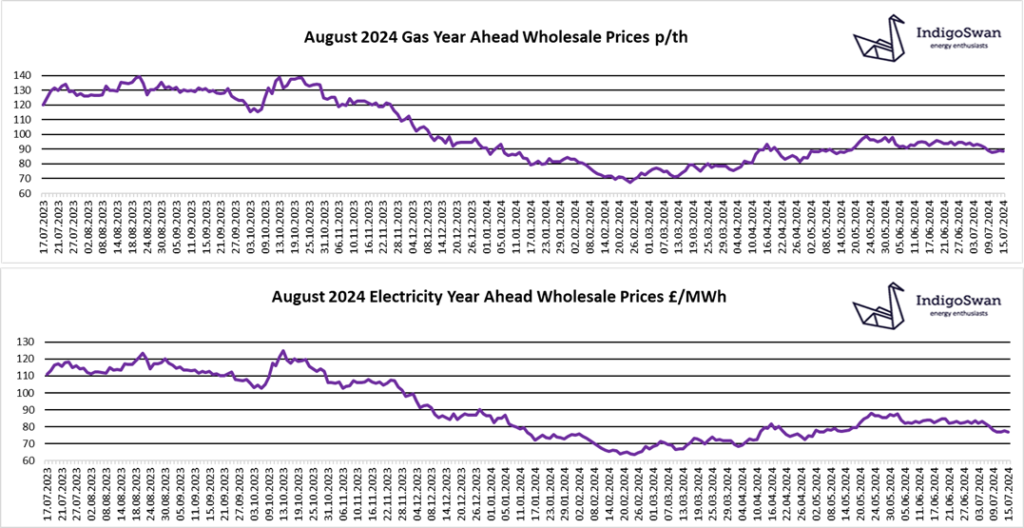

Gas and Electricity Year Ahead Wholesale costs are lower than last week. There has been a slight downturn in prices since early June, although the daily ups and downs underline the lack of clear direction. Costs remain far lower than those seen in 2021 / 2022 / 2023.

EU Gas Storage levels continue to increase, now at 81% full against a target of 90% by November. This positive position gives the industry confidence for winter 2024/2025, as Storage is expected to be required to help meet the higher heating demand.

Despite most EU nations wanting to impose more damaging sanctions on Russia’s LNG exports, the concern of tight supply margins has so far seen resistance. Lower Russian exports mean Norway is now the main supplier of Gas to the EU, which makes Europe vulnerable to Gas shortages, in the event of further supply issues. August will see Norway undertake planned maintenance of some Gas assets. As these are known events, the markets will have already built them into prices. LNG shipments are still very low as they head to Asia where there is a price premium.

We have seen a lower contribution to generation from Wind over the last week at 19%, resulting in a higher use of Gas at 25%, and imports from the Interconnectors with Europe at 23%.

We would encourage customers that have Gas or Electricity contracts ending in 2024, to discuss options with Indigo Swan and closely monitor the position.

If you enjoyed reading this blog, why not try one of our others: