Headlines:

- Gas and Electricity Wholesale prices are similar to last week

- Low LNG deliveries due to competition from Asia

- EU Gas Storage levels are a positive 83% full

Energy Overview

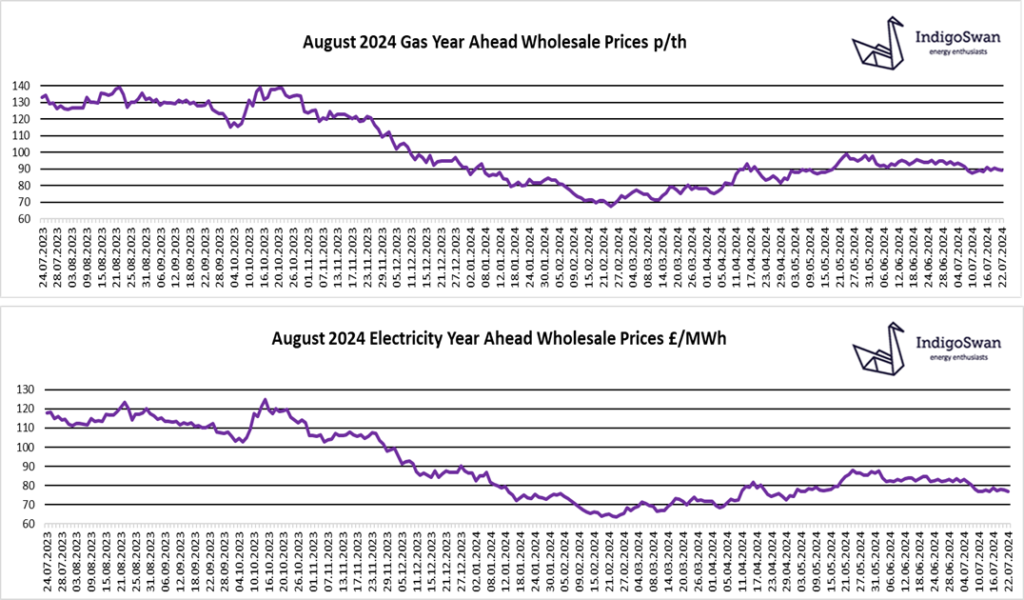

Gas and Electricity Year Ahead Wholesale costs are similar to those in last week’s report. There has been a slight downturn in prices since early June, although the daily ups and downs underline the lack of clear direction. Costs remain far lower than those seen in 2021 / 2022 / 2023.

The higher temperatures across Europe and Asia are adding pressure to energy supplies to provide air cooling. Gas Storage levels in both regions remain high, notably at 83% full in the EU against a target of 90% by November. As we saw last year, it is likely they will reach almost 100% before the start of winter 2024/2025. The US Freeport LNG plant appears to be resuming some activity after closing due to storm damage. There is currently some unplanned Norwegian Gas maintenance, with further planned in August and LNG shipments continue to be attracted to Asia where there is a price premium.

Imports of Electricity through the Interconnectors remained high at 22% of supplies over the last week. The majority came from the French Nuclear fleet, with the North Sea Link providing Hydro power from Norway. Imports are not always reliable, but with a growing number of connections from various sources, this reduces the risk of serious disruption. Wind’s contribution was lower at 15% which meant we needed large amounts of Gas at 26%, and almost 1% from Coal, which is due to end later this year.

We would encourage customers that have Gas or Electricity contracts ending in 2024, to discuss options with Indigo Swan and closely monitor the position.

If you enjoyed reading this blog, why not try one of our others: