Headlines:

- Gas and Electricity Wholesale prices are higher than last week

- Low LNG deliveries due to competition from Asia

- EU Gas Storage levels are a positive 84% full

Energy Overview

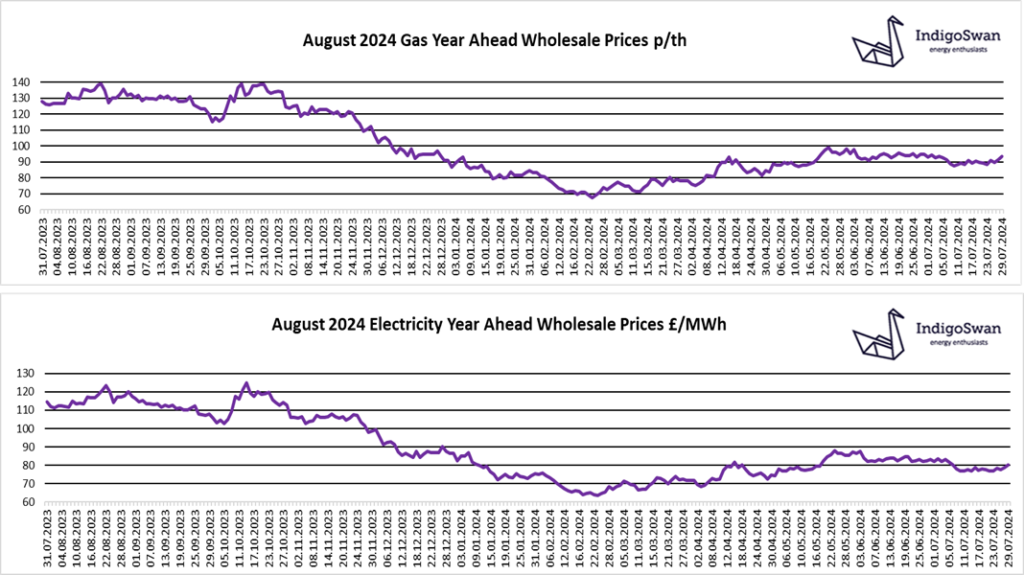

Gas and Electricity Year Ahead Wholesale costs are higher than those in last week’s report. They remain far lower than most of 2021 / 2022 / 2023, but still more than double those in 2020.

With EU Gas Storage being 84% full and well on track to exceed the 90% target before the start of the higher winter demand, this is supressing energy price volatility. We saw peak prices in 2022 when Storage was just 68% and Russia was reducing Gas supplies into Europe. Since then, Norway has replaced Russia as the main Gas supplier and investment has been made to increase the capacity to receive LNG shipments. Competition is increasing for LNG which has seen more going to Asia where they are currently paying a premium, compared to Europe. Unfortunately, this reliance from global sources means we are more likely to see the effects from regional issues, such as conflicts, storms, maintenance and industrial action.

Over the last week, 22% of our Electricity came from Europe via the Interconnectors, with the majority coming from France but with notable contributions by Norway, Denmark and Belgium. Wind fell further to just 13% with low levels expected in the short term. Gas remains a reliable and flexible source of generation and at 28% of supplies it continues to set the direction of Electricity prices. The use of Coal is due to end in 2024 and provided just under 1%, helping to balance the network.

We would encourage customers that have Gas or Electricity contracts ending in 2024, to discuss options with Indigo Swan and closely monitor the position.

If you enjoyed reading this blog, why not try one of our others: