Headlines:

- Gas and Electricity Wholesale prices are lower than last week

- A number of potential issues are adding pressure to prices

- EU Gas Storage levels are a positive 93% full

Energy Overview

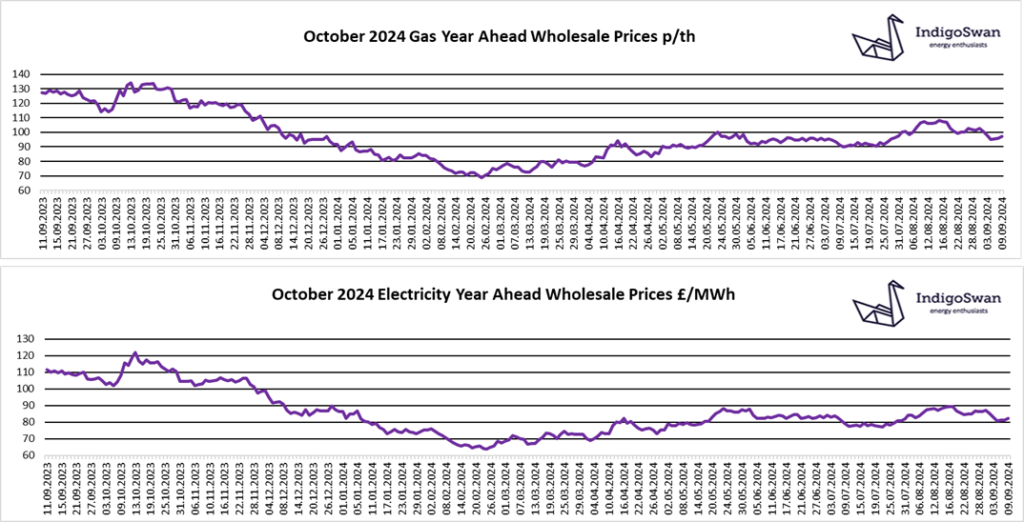

Gas and Electricity Year Ahead Wholesale costs are lower than those in last week’s report. They continue to show good value compared to most of 2021 / 2022 / 2023 but are still double those in 2020.

The last week saw some easing of prices due to a more positive outlook, but concern remains that if additional Gas is needed due to a prolonged cold spell or there are more disruptions, then we will have to compete for LNG. Other concerns are that tensions in the Middle East could result in lower Gas supplies from the region and it is likely that Ukraine will not renew the current Gas transit deal with Russia at the end of the year, which allows Gas to be piped into Europe. Other routes will likely be found but there may be reduced flows.

LNG deliveries to Europe remain low as they are attracted to Asia where there is a price premium and Norwegian Gas maintenance is also impacting on supplies. Despite these, EU Gas Storage has increased to 93% full, against the target of 90% by November. Storage is expected to be used through the winter to support periods of higher demand.

The last week saw Wind generation fall to just 17% of supplies compared to 21% the week before. This meant that the use of Gas increased to 28% and Imports from Europe via the Interconnectors provided 19%.

Some of the threats to supplies may not materialise and a positive outlook could return, but due to the risks, we would encourage customers that have Gas or Electricity contracts ending in 2024 and potentially early 2025, to discuss options with Indigo Swan and closely monitor the position.

If you enjoyed reading this blog, why not try one of our others: