Headlines:

- Gas and Electricity Wholesale prices are lower than last week

- Some of the price pressures are easing

- EU Gas Storage levels are a positive 93% full

Energy Overview

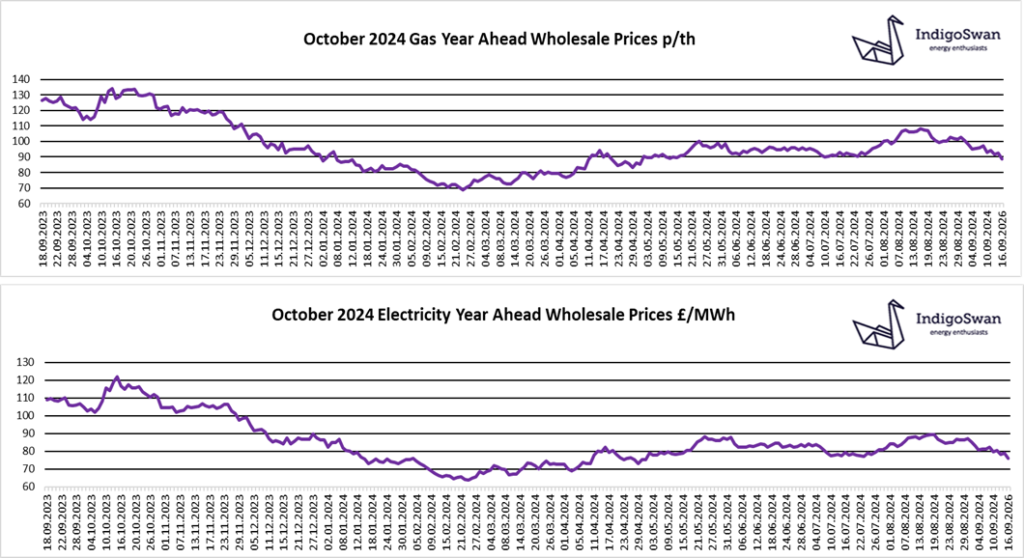

Gas and Electricity Year Ahead Wholesale costs are lower than those in last week’s report, continuing a downward trend, showing good value compared to most of 2021 / 2022 / 2023 but still double those in 2020.

There remains concern that should Europe require additional Gas either due to a supply issue or an increased demand beyond that normally expected, then we would have to compete with Asia for LNG deliveries. EU Gas Storage is a positive 93% full and should go higher as Norwegian Gas maintenance eases.

It is expected that the contract allowing Russian Gas to pass through Ukraine will not be renewed at the end of the year, which will mean another route or source will need to be found. However, the EU could take this opportunity to significantly reduce Russian Imports, as member states have been unable to agree effective sanctions. The tensions in the Middle East and the possibility of disruption to Gas from the region seems to have less of an impact on prices, which is highlighted with the price of Oil recently falling to an almost three-year low.

The last week saw Wind generation increase to 25% of supplies compared to 17% the week before. This meant that the use of Gas decreased to 22% and Imports from Europe via the Interconnectors provided 16%.

Some of the threats to supplies may not materialise and the more positive outlook may continue, but due to the risks, we would encourage customers that have Gas or Electricity contracts ending in 2024 and potentially early 2025, to discuss options with Indigo Swan and closely monitor the position.

If you enjoyed reading this blog, why not try one of our others: