Headlines:

- Gas and Electricity Wholesale prices are higher than last month

- The Ukraine / Russia Gas transit deal has ended

- EU Gas Storage levels are lower at 70% full compared to 85% last year

Energy Overview

As of the 6th of January, Gas and Electricity Year Ahead Wholesale costs were higher than in last month’s report.

Following a period of higher prices in November and early December, they initially began to fall as some positivity returned. However, as we approached the end of the year it started to become clear that any optimism that a deal may be done between Ukraine and Russia to extend the Gas transit deal, was unfounded. Ukraine’s decision was made to deprive Russia of billions of pounds which could be used to support their war effort. In response, Slovakia has threatened to stop supplying Ukraine with Electricity, which is required due to the attacks on their energy infrastructure. Although alternate Gas transit options had been rumoured, which would likely involve a country buying Russian Gas and selling it to Europe, nothing materialised. From January, Europe has imported less Gas, increasing the rate of Storage withdrawals, which are already significantly lower than last year at only 70% full. It is hoped that a period of milder weather and an increase in LNG deliveries will help stabilise the decline in Storage levels and in turn, ease Gas and Electricity prices.

In December 2024 Gas generation contributed 31% of our Electricity, higher than 2023, despite more Wind assets being available. Supplies via the Interconnectors with Europe were also higher as Coal is no longer available and Nuclear was lower.

What does this mean for me?

The energy industry has changed how it recovers Electricity Distribution, Transmission and Balancing costs, under the Targeted Charging Review. This has moved some charges away from being based on the energy used and billed in the unit rate, to fixed charges incorporated within the Standing Charge or as separate items. This should give both the customer and the industry a more accurate way of calculating budgets, but the change has become noticeable within energy bills and created concern. Over the next two years, there is a quite confused picture of increases and decreases in Transmission and Distribution charges, which energy suppliers will be billing customers.

From April 2024 most customers saw a decrease in Transmission which is likely to be followed by an increase in this fixed charge from April 2025, almost completely replacing what used to be recovered through Triads. Distribution costs are a little more complicated with the average fixed annual cost increasing across networks from April 2024 but decreasing from April 2025. Another element, the Available Capacity (AC), has already seen small increases but is due for a more significant rise from April 2025. This does mean that by managing the Agreed Supply Capacity, there is an opportunity to reduce the AC cost and longer term possibly lower the Band which determines fixed charges.

There is an expectation that Balancing costs will continue to increase.

Indigo Swan works closely with energy suppliers to help all our customers understand and manage changes.

Please contact us on 0333 320 0475 to discuss options or to get a latest update.

Gas market overview

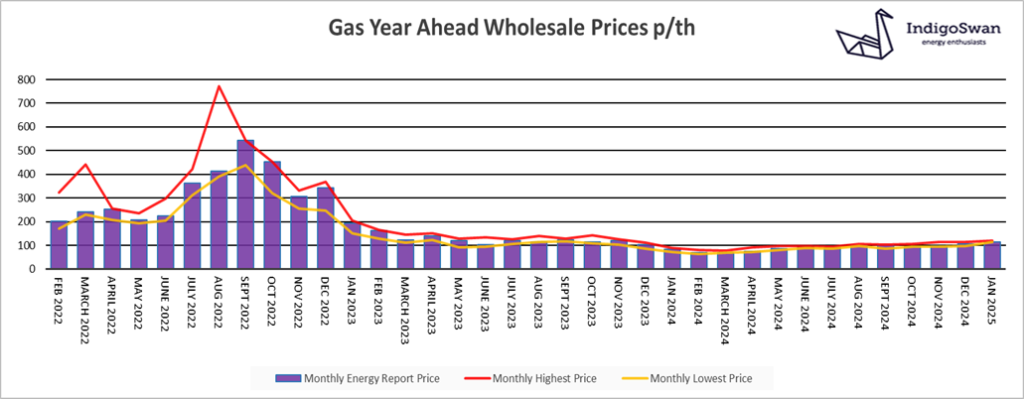

On the 6th of January, the Gas Year Ahead Wholesale cost was 114.38p/th, up from 107.29p/th in last month’s report and 37% more than 2024. Although an increase, there has been a small reduction as it peaked at 120p/th earlier in the month.

A period of price volatility returned in December and continued into January, due to the reduced Gas imports into Europe following the end of the Ukraine / Russia transit deal and no alternate arrangement being available. The recent slight easing of prices is an adjustment following the exaggerated market reaction to an event that was always likely and partially already factored into costs.

The cold spell both here and in Europe has increased the need for Gas to meet the additional heating demand. EU Gas Storage levels are now 70% full compared to an average of almost 85% over the last two years. The withdrawals are a concern not only for this winter but also 2025/26, as injections may begin from a very low starting point and with less surplus supplies being available and at a higher cost. The increase in LNG deliveries may help alleviate the problem.

The direction of Wholesale prices is uncertain, with a number of events potentially either reducing Gas supplies or increasing demand. We would advise discussing your options for contracts ending early 2025 or at least monitoring the position closely.

Electricity market overview

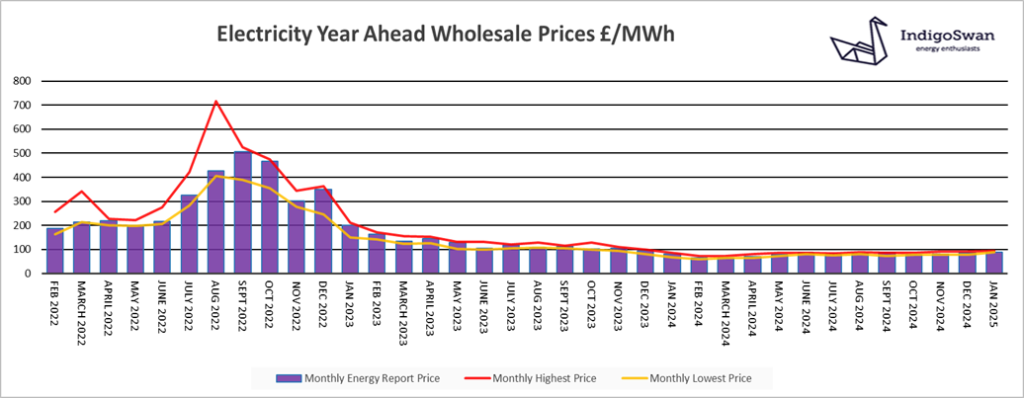

On the 6th of January, the Electricity Year Ahead Wholesale cost was £89.38/MWh, up from £85.25/MWh in last month’s report and 12% more than 2024. Although an increase, there has been a small reduction as it peaked at £93/MWh earlier in the month.

Electricity costs have followed Gas due to our reliance on it as a flexible and reliable form of generation. The pressure on Gas prices remains with the reduction of Russian supplies into Europe. Factors influencing costs will be, the amount of Gas required for heating across Europe, the number of LNG shipments and the level of EU Gas Storage, which is significantly lower than the last two years.

The contribution of Gas for generation fell to 31% of supplies in December from 40% in November and have fallen further to 26% over the last week. Electricity imports from Europe remain high at 14% and Wind 33%. With the closure of our Coal fuelled generation in 2024, imports will be an important tool in balancing the network, as will tools such as the new look Demand Flexibility Service.

The direction of Wholesale prices is uncertain, with pressure potentially from increased Gas costs or with markets being so sensitive, from any unplanned Electricity generation outages. We would advise discussing your options for contracts ending early 2025 or at least monitoring the position closely.

If you enjoyed reading this blog why not try one of our others: