Headlines:

- Gas and Electricity Wholesale prices are slightly higher than last month

- EU Gas Storage levels are lower at 34% full compared to 59% last year

- Concern at the cost to replenish EU Gas Storage for winter 2025/26

Energy Overview

As of the 1st of April, Gas and Electricity Year Ahead Wholesale costs were slightly higher than in last month’s report.

Compared to recent months, March was more stable, showing a smaller difference between the monthly high and low prices. This follows the significant falls in February after Presidents Trump and Putin spoke regarding the war in Ukraine. Although all parties are talking, there has been little real progress, which over time may begin to be reflected in energy prices, as markets consider the likelihood, that no additional Russian Gas will be available this year.

EU Gas Storage remains very low at just 34% full compared to 59% last year. The EU has interim targets which ultimately require Storage to be 90% full by November 2025. This is creating issues as it forces Gas to be purchased regardless of the current price. EU members have asked for the relaxation of these targets and are challenging the decision to extend them for two more years.

Gas continued to be the main single source of Electricity generation in March, accounting for 33% of supplies, followed by Wind at 22%. Because of this, the price direction of Gas dictates Electricity’s and will do so until more Renewables are available, with the ability to store surplus supplies for future use. The UK is becoming more connected with Europe, which includes the Import of large volumes of Nuclear power from France and Hydro from Norway.

What does this mean for me?

The energy industry has changed how it recovers Electricity Distribution, Transmission and Balancing costs, under the Targeted Charging Review. This has moved some charges away from being based on the energy used and billed in the unit rate, to fixed charges incorporated within the Standing Charge or as separate items. This should give both the customer and the industry a more accurate way of calculating budgets, but the change has become noticeable within energy bills and created concern. Over the next two years, there is a quite confused picture of increases and decreases in Transmission and Distribution charges, which energy suppliers will be billing customers.

From April 2025 customers will see an increase in Transmission costs with an expectation of further increases from April 2026. Distribution costs are a little more complicated with the average fixed annual cost decreasing across networks from April 2025, remaining similar in 2026. Another element, the Available Capacity (AC), increases significantly for most from April 2025, with small reductions in 2026. This does mean that by managing the Agreed Supply Capacity, there is an opportunity to reduce the AC cost and longer term possibly lower the Band which determines fixed charges.

Balancing costs, which pay to fine tune Electricity supplies to avoid power cuts, will increase from October 2025.

Indigo Swan works closely with energy suppliers to help all our customers understand and manage changes.

Please contact us on 0333 320 0475 to discuss options or to get a latest update.

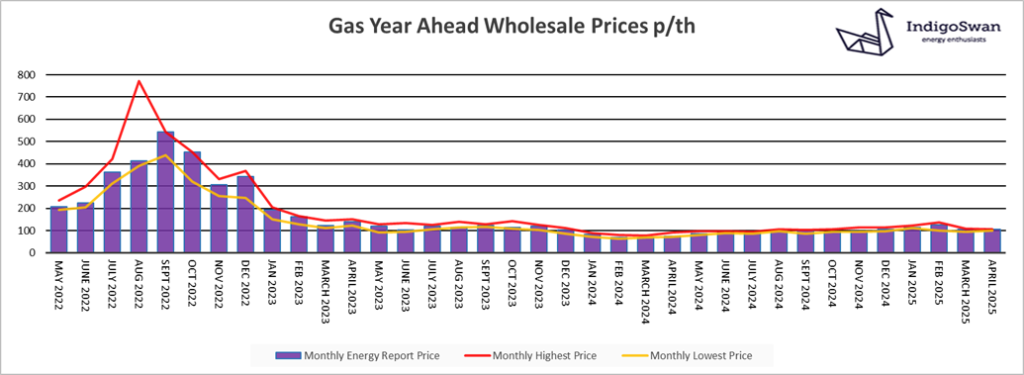

Gas market overview

On the 1st of April, the Gas Year Ahead Wholesale cost was 105.17p/th, up from 105.12p/th in last month’s report and 37% more than 2024.

There was little movement of the Gas price in March, due to the uncertainty surrounding peace talks between Ukraine and Russia. The energy market reductions in February reflected the hope that more Gas would become available from Russia to support Storage and the additional winter demand. The longer the lack of progress continues, the greater the chance that prices will start to climb. In March, large volumes of LNG were delivered, as the demand from Asia eased.

The focus of price direction is the level of EU Gas Storage, which is just 34% full compared to 59% last year and 56% in 2023. This reduction is the result of less Gas being available and winter temperatures returning to normal rather than the two previous mild seasons. The EU is trying to enforce the need for Storage to be 90% full by November for another two years and keep interim targets. This means that Gas will need to be purchased regardless of the cost, which is creating a further price pressure. Some EU member states are challenging this, asking for more flexibility.

We would encourage customers that have Gas or Electricity contracts ending in the first half of 2025 and potentially further out, to discuss options with Indigo Swan and closely monitor the position.

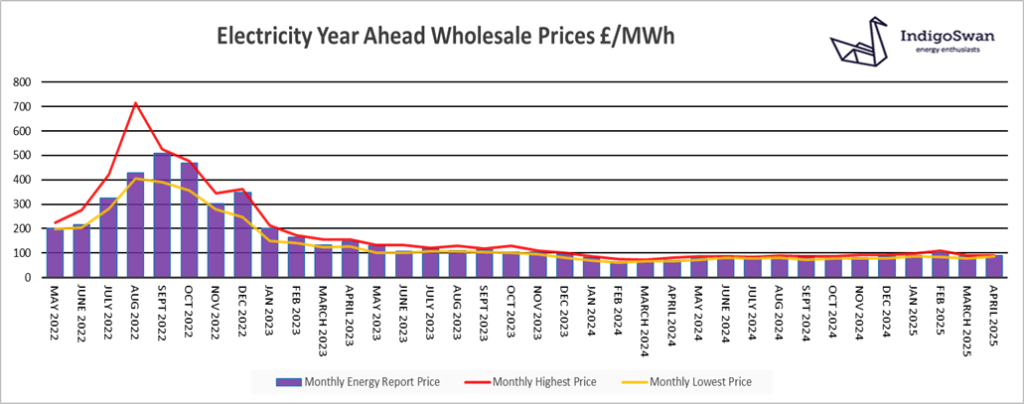

Electricity market overview

On the 1st of April, the Electricity Year Ahead Wholesale cost was £87.89/MWh, up from £85.63/MWh in last month’s report and 25% more than 2024.

Gas contributed a slightly lower 33% of generation in March, compared to 35% in February and just 25% over the last week. Wind was also down at 22% compared to 27%, with Imports from Europe via the Interconnectors at a high 19%. Although more Renewables are being added to the network, we are still very reliant on the use of expensive Gas. This means the Electricity market will follow it, unless there is some major factor that solely impacts on power demand or generation. With the concern for Gas supplies and Storage levels both in the UK and mainland Europe, there is still uncertainty as to price direction. If peace talks between Russia and Ukraine are successful, we may see additional supplies, which should then lower energy costs. However, the opposite is also a possibility.

The new Transmission and Distribution costs came into effect from 1st April 2025, which will generally see increases for most customers. Those already on fixed price contracts will see no change, but are likely to notice differences on new contracts, especially with Half Hourly meters.

We would encourage customers that have Gas or Electricity contracts ending in the first half of 2025 and potentially further out, to discuss options with Indigo Swan and closely monitor the position.

If you enjoyed reading this blog why not try one of our others: