Headlines:

- Gas and Electricity Wholesale prices are lower than last week

- Trade tariffs are reducing economic and energy demand forecasts

- EU Gas Storage remains very low

Energy Overview

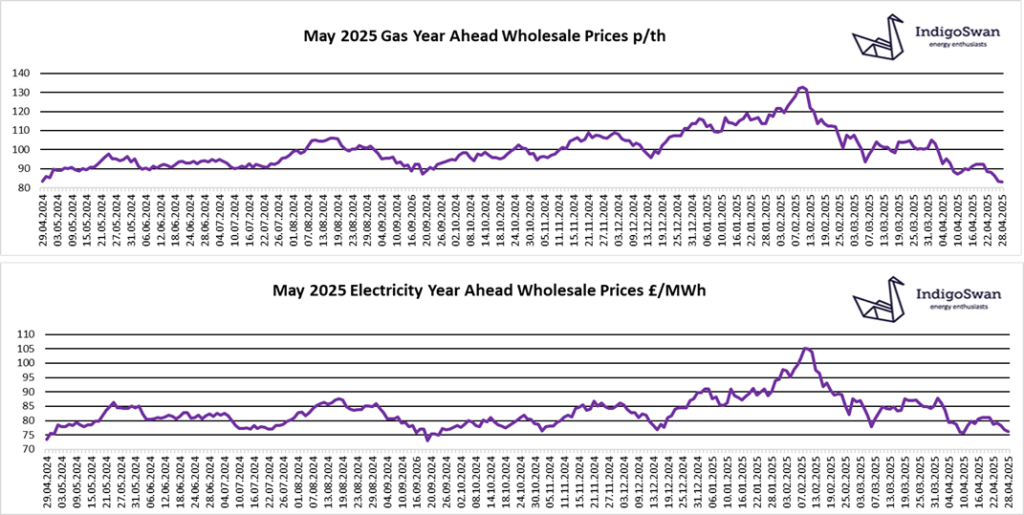

Gas and Electricity Year Ahead Wholesale costs are lower than in last week’s report and significantly lower than most of 2021 / 2022 / 2023, but still higher than 2020. The Oil price is $66 from $67.

EU Gas Storage remains very low at 39% full compared to 62% in 2024 and 59% in 2023. Some progress has been made since the start of April, in an attempt to achieve the interim and the final target of 90% full by November 2025. There have been appeals asking for some flexibility in the targets, to avoid having to buy Gas for Storage when prices are not favourable. Following developments last week, it would appear likely that there will be some concessions, which have potentially been a factor in Gas prices falling further. The hope that Russian Gas flows will resume through Ukraine this year are fading, which means the continued reliance on supplies from Norway and LNG shipments, largely from the US.

The impact of the trade tariffs applied by the US and specifically the higher rates between the US and China, will likely be the slowing of the global economy and a reduction in forecast energy use. OPEC+ has also surprisingly increased Oil production beyond expectations.

The last week saw a lower Wind contribution to generation at 15%, down from 21%, which meant Gas was a higher 34% from 26%. Imports from Europe via the Interconnectors were 19% from 20%.

It is not clear how a number of factors will influence prices, which include peace talks, Gas storage levels and tariffs. We would encourage those with Gas and Electricity contracts that are due to end in the next few months and potentially further out, to engage with Indigo Swan and monitor positions closely.

If you enjoyed reading this blog, why not try one of our others: