Headlines:

- Gas and Electricity Wholesale prices are lower than last month

- EU Gas Storage levels are lower at 41% full compared to 64% last year

- Tariffs being applied by the US have reduced Wholesale energy prices

Energy Overview

As of the 6th of May, Gas and Electricity Year Ahead Wholesale costs were much lower than in last month’s report.

April saw quite significant falls largely due to the introduction and then partial withdrawal of tariffs by the US. The initial announcements caused losses to both the financial and energy markets, due to a likely downturn in the global economy. In response, President Trump backtracked on some, pausing their introduction, but continued to escalate retaliatory tariffs with China. Although prices have now stabilised, we await the impact as more announcements are made. OPEC+ increased Oil production above expectations which has seen it fall to $62 a barrel.

EU Gas Storage remains low at just 41% full compared to 64% last year. Less Gas is available to refill Storage due to the ending of the transit deal between Russia and Ukraine in January 2025. The summer will also see planned outages for the maintenance of Gas infrastructure. This could result in entering winter 2025/26 with tight supply margins, which may be an issue, especially if there is a period of prolonged, below average temperatures.

The improved temperatures through April saw an increase in the contribution of Solar generation, which helped reduce Gas use to 28% of supplies, from 33% last month. Wind was also down at 19% from 22%. Imports from the continent via the Interconnectors were stable at 19%.

What does this mean for me?

The energy industry has changed how it recovers Electricity Distribution, Transmission and Balancing costs, under the Targeted Charging Review. This has moved some charges away from being based on the energy used and billed in the unit rate, to fixed charges incorporated within the Standing Charge or as separate items. This should give both the customer and the industry a more accurate way of calculating budgets, but the change has become noticeable within energy bills and created concern. Over the next two years, there is a quite confused picture of increases and decreases in Transmission and Distribution charges, which energy suppliers will be billing customers.

From April 2025 customers will see an increase in Transmission costs with an expectation of further increases from April 2026. Distribution costs are a little more complicated with the average fixed annual cost decreasing across networks from April 2025, remaining similar in 2026. Another element, the Available Capacity (AC), increases significantly for most from April 2025, with small reductions in 2026. This does mean that by managing the Agreed Supply Capacity, there is an opportunity to reduce the AC cost and longer term possibly lower the Band which determines fixed charges.

Balancing costs, which pay to fine tune Electricity supplies to avoid power cuts, will increase from October 2025.

Indigo Swan works closely with energy suppliers to help all our customers understand and manage changes.

Please contact us on 0333 320 0475 to discuss options or to get a latest update.

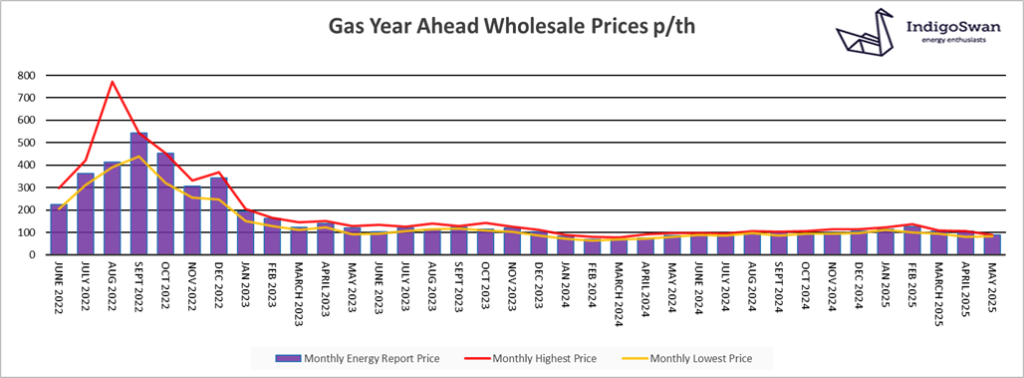

Gas market overview

On the 6th of May, the Gas Year Ahead Wholesale cost was 88.65p/th, down from 105.17p/th in last month’s report and 1% more than 2024.

President Trump’s tariff announcements on imports into the US had a significant impact on growth forecasts for the global economy and therefore the need for energy. The subsequent pausing of higher rate tariffs for the likes of the EU, stopped further losses, but the escalation with China and the potential for further measures has meant that prices remain much lower. The EU has announced plans to stop using Russian Gas by the end of 2027.

There is still likely a premium being built into Gas prices due to the low level of EU Gas Storage, currently at 41% full compared to 64% last year. This has improved, but there is still concern that stocks will be too low for winter 2025/26 and potentially (although unlikely) need measures to reduce Gas use. Large quantities of LNG are being bought to help compensate for reduced Russian supplies, and with peace talks making little progress, they are not likely to return via Ukraine in 2025, as had been hoped. The EU will probably reduce the Gas Storage target of 90% full by November and allow more flexibility to avoid having to buy when prices are higher. This could ease prices, although markets may have already factored it in.

We would encourage customers that have Gas or Electricity contracts ending in the first half of 2025 and potentially further out, to discuss options with Indigo Swan and closely monitor the position.

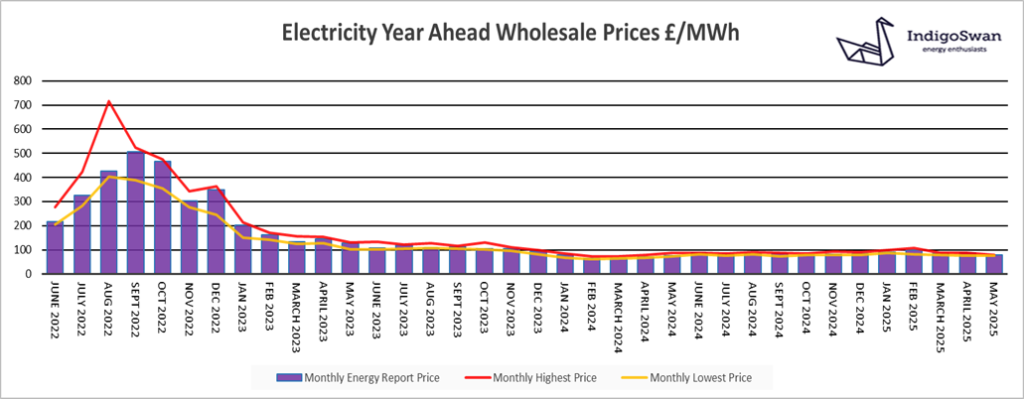

Electricity market overview

On the 6th of May, the Electricity Year Ahead Wholesale cost was £80.14/MWh, down from £87.89/MWh in last month’s report and 4% more than 2024.

The fall in prices has largely been the result of lower Gas costs, after the announcements of tariffs being imposed by the US. It is expected that these will lower forecasts for the use of Gas, Electricity and Oil. This does mean that energy markets could move again in either direction, based on any future policies.

April saw an improved contribution of Solar which helped reduce the use of Gas, which still accounted for 28% of generation, lower than the 33% in March. Electricity prices continue to follow the direction of Gas. Wind was also lower at 19% compared to 22%. Interconnectors, which allow us to import and export Electricity from the likes of Norway and France, provided 19%.

About 50% of the fully delivered Electricity price is the Wholesale element. Other charges include the investment in renewables and our infrastructure. These help to avoid power outages, similar to those in Spain and Portugal.

We would encourage customers that have Gas or Electricity contracts ending in the first half of 2025 and potentially further out, to discuss options with Indigo Swan and closely monitor the position.

If you enjoyed reading this blog why not try one of our others: