Headlines:

- Early trading on the 24th has seen large reductions in Wholesale prices

- Much of the risk premium, due to the Iran / Israel conflict, has been removed

- EU Gas Storage levels remain very low at just 56% full

Energy Overview

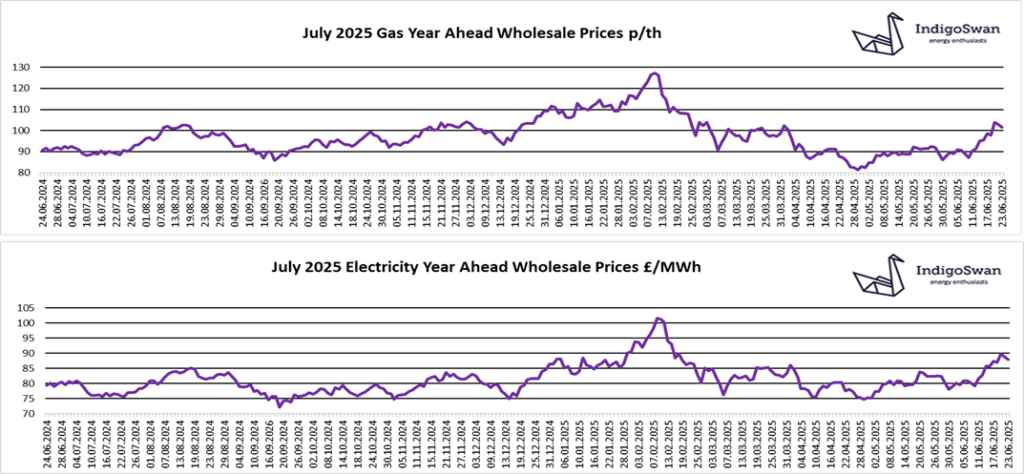

Since the close of the energy markets on the 23rd of June (which are reflected in the graphs), prices have fallen significantly in early trading on the 24th, back to the levels seen two weeks ago. They remain significantly lower than most of 2021 / 2022 / 2023, although higher than 2020. Oil is $69 a barrel from $74.

Over the last week, energy markets continued to include a premium in anticipation for the disruption to Oil and LNG supplies from the Middle East. UK Wholesale Gas costs increased in the region of 15% in two weeks, which impacted on Electricity due to its use for generation. The missile strikes by the US on Iranian Nuclear facilities made it more likely that Iran would close the Strait of Hormuz, which would drive-up global costs. However, on the evening of the 23rd of June, Iran’s retaliation was a symbolic missile attack on a US base. This had little threat, but the perception of taking action, allowed them to agree to a ceasefire with Israel, that for now has reduced much of the concern, which is being reflected in lower costs.

EU Gas Storage levels have improved slightly at 56% full, but remain considerably lower than last year’s 75%. With less supplies being available from Russia, refilling Storage will be a challenge, making LNG an important source of supply. The EU still plans to end all Imports of Russian Gas by the end of 2027.

The last week has seen 20% of Electricity come from Gas and 24% from Wind, with very high contributions of over 40% on Sunday and Monday, which meant we were net Exporters of Electricity to the continent.

We would encourage those with energy contracts ending in the next few months and potentially further out, to engage with Indigo Swan and monitor positions closely.

If you enjoyed reading this blog, why not try one of our others: