Headlines:

- Prices are slightly higher than in last week’s report

- New US tariffs are due to start from the 1st of August

- The government has abandoned Electricity Zonal pricing

Energy Overview

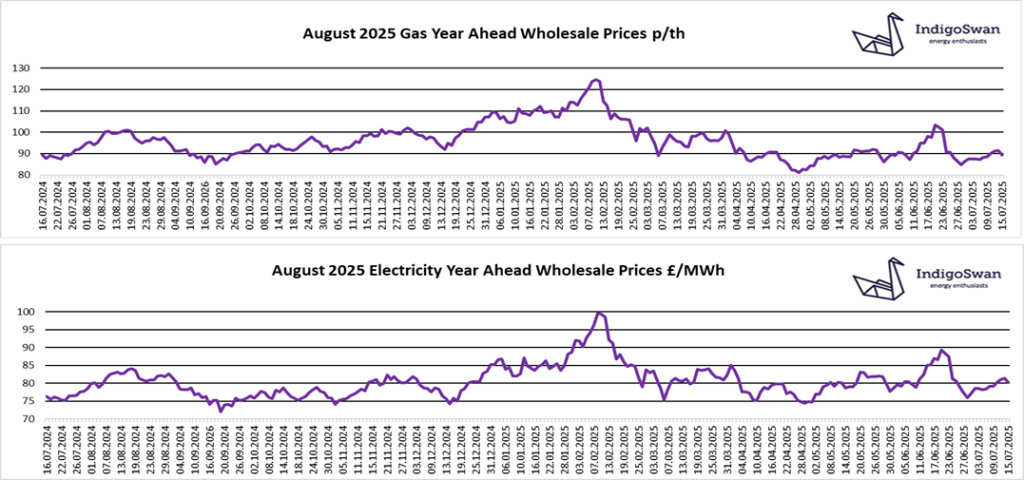

Gas and Electricity Year Ahead Wholesale costs are higher than those in last week’s report but are significantly lower than most of 2021 / 2022 / 2023, although higher than 2020. Oil remains at $69 a barrel.

Last week was another relatively quiet one, compared to the previous price fluctuations seen when tariffs were announced and during the period of conflict between Iran and Israel. Tariffs remain a big issue as they have the potential to impact on the global economy, changing energy demand forecasts and influencing prices higher or lower. If agreements are not made, then new US tariffs will begin from the 1st of August, likely followed by retaliation. More recently the US has said that unless a peace deal is in place within 50 days, then Russia’s trading partners will face 100% tariffs. This is largely aimed at the likes of India and China, who have been buying cheaper Russian exports, as other markets show solidarity with Ukraine. Russia’s economy relies heavily on Oil and Gas exports.

EU Gas Storage remains very low at just 63% full compared to 81% last year. With less Gas being available from Russia following the end of the Ukraine transit deal in January 2025, large quantities of LNG will be required. This means competing with Asia for shipments, which has the potential to inflate costs.

Wind generation fell sharply to 14% of supplies, compared to 24% the week before. This meant a small increase in the use of Gas at 24% and a significant increase in Imports from Europe via the Interconnectors, at 21% from 15%. The government has decided not to move ahead with Zonal pricing.

We would encourage those with energy contracts ending in the next few months and potentially further out, to engage with Indigo Swan and monitor positions closely.

If you enjoyed reading this blog, why not try one of our others: