Overview

As of the 2nd November, Gas Year Ahead Wholesale costs were slightly higher and Electricity slightly lower, when compared to last month’s report.

The price of Oil had seen some gains but has since fallen back from $43 to $39 a barrel. Reduced production cuts by OPEC+, which includes Saudi Arabia and Russia, and more supplies being available from Iran and Libya, are contributing factors. There is concern for growth of the global economy, with rising coronavirus cases and increasing instances of measures, including the lockdown in England from Thursday 5th for four weeks. This week’s US election result may well impact on prices.

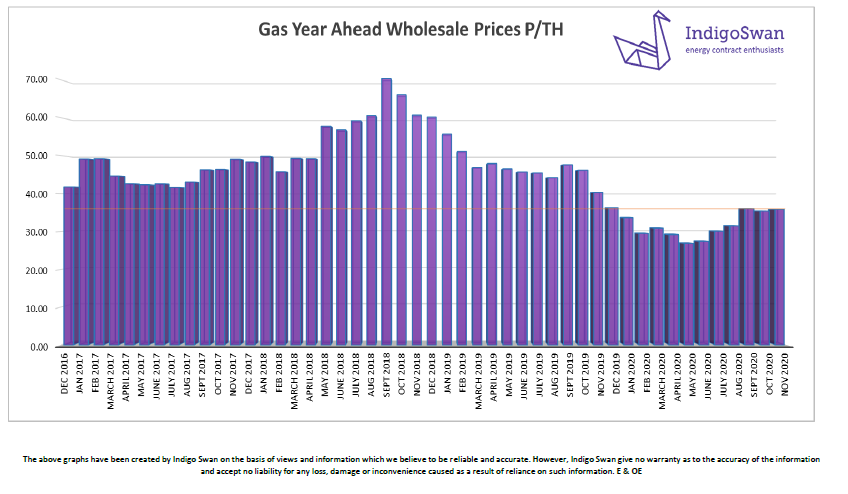

Gas Wholesale costs remain competitive, as illustrated by our graph. October saw a five-month low need for Gas for Electricity generation. There were some supply issues and low LNG deliveries, but despite this, UK and European Storage levels remain high.

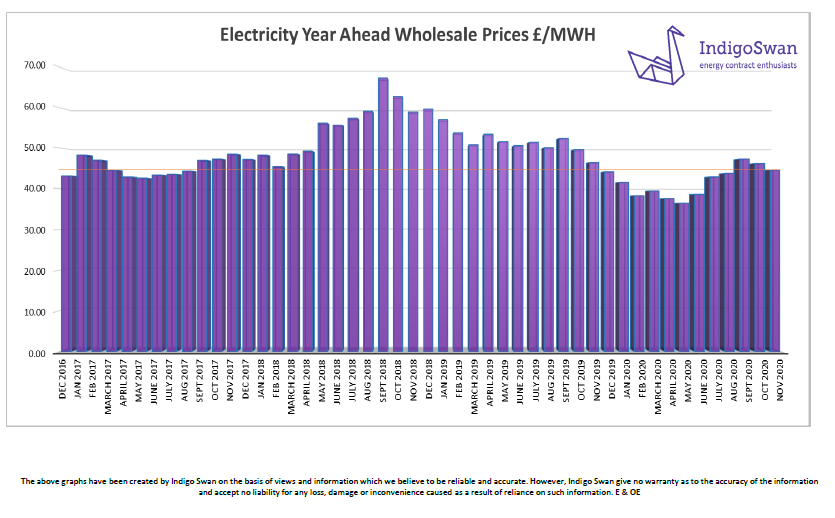

Electricity Wholesale prices are also competitive, lower than 2018 and most of 2019. There was an increased contribution from Nuclear and higher Imports. Combined Wind and Solar remained unchanged at 25%, although a period of very low levels did cause Gas and Electricity price spikes.

The Met Office forecast for the next month suggests average temperatures. Some night frosts will increase Gas use for heating. Generally settled conditions with higher winds isolated to the north, potentially requiring more support from Gas generation. This could pressure Gas and Electricity prices.

What does this mean for me…?

Wholesale prices still show good value. It should be remembered that this element makes up in the region of just 40% of the total cost of an Electricity bill and roughly 60% for Gas.

Increasing third-party costs are noticeable in Electricity contracts. These include, Transportation, Distribution, and government policy levies.

Over the next few years, the way some of these charges are calculated will change, under the Targeted Charging Review, full details are not yet available. Initially the first change to Transportation costs was due April 2021, but with delays issuing price guidelines to energy suppliers, this has been postponed until April 2022. The planned change to Distribution charges is still set for April 2022. This does mean that the expected opening of some fixed priced contracts should not take place until 2022.

We advise requesting supplier offers for all 2020 and early 2021 start contracts to compare against your current prices. Be aware that suppliers have tightened their credit requirements and reduced their risk appetite. There was evidence these positions were easing, but with the new lockdown, there may be renewed caution. Good forward contract options can still be negotiated.

Please contact us on 0333 320 0475 to discuss options or to get a latest update.

Gas Market

On the 2nd November, the Gas Year Ahead Wholesale cost was 35.85 (p/th), from 35.37 (p/th) in last month’s report and 11% lower than 2019.

Less Gas was needed in October for Electricity generation, at 36% of demand from 43%. Mid-month did see price spikes when this rose to 50% and 55%, on consecutive days. More recently this has eased, which has been reflected in lower Wholesale costs.

Low LNG deliveries were the result of production issues and a rising Asian LNG price, making it an attractive destination for shipments. There are a number of deliveries due here in the coming week, which may continue as happened last winter. These help us maintain high Gas Storage levels and absorb any additional demand for generation or heating.

Although we have seen lower temperatures, we still await a very cold spell, which typically has an immediate but short-term impact on Gas, and a knock-on effect on Electricity.

Let us know if you would like us to research your options for 12, 24 and 36 month contracts.

Electricity Market

On the 2nd November, the Electricity Year Ahead Wholesale cost was 44.57 (£/MWh), from 46.19 (£/MWh) in last month’s report and 4% lower than 2019.

Wind and Solar contributed 25% of generation in October, the same as September. The erratic nature of these supplies did mean that we saw a day at just 8%, requiring a greater need for Gas use and price spikes. As we head into the winter, the impacts could be more significant.

There were days when we needed Coal generation to support reduced supplies, but at less than 1% for the month. Nuclear and Imports returned to expected levels.

The industry remains confident that it can cope with changing demand patterns, which now includes a lockdown during winter months. There are mechanisms in place to secure generation or reduce demand. Although these mechanisms do come at a cost, in the form of higher Third-Party Charges within Electricity bills, they do provide an element of stability to prices which otherwise may react with far more volatility.

Let us know if you would like us to research your options for 12, 24 and 36 month contracts.