Headlines:

- Gas and Electricity Wholesale prices are higher

- EU Gas Storage levels remain high at 56% full

- OPEC announced further Oil production cuts

Energy Overview

As of the 5th of April, Gas and Electricity Year Ahead Wholesale costs were higher, when compared to last month’s report.

OPEC announced further Oil production cuts on top of those from last year, in an attempt to pressure prices higher. Russia also stated the intention to extend their cuts until the end of the year. Prices have rebounded from $73 per barrel over the last month to $85.

There has been a small reduction in the EU’s Gas Storage levels from 59% full to 56%. This is significantly higher than the 30% seen in both 2021 and 2022. The EU target for November 2023 is 90%, in readiness for the winter demand, which will require Gas injections through the warmer months. Large numbers of LNG deliveries are still being made to Europe, compensating for the lower Gas flows from Russia, some of which are instead being diverted to China, which may reduce their future demand for LNG.

As Gas is the main source of generation, the price of Electricity closely follows, despite the contribution from much cheaper Renewables. The growing diversity of supplies, which includes Nuclear and Hydro Imports from the continent, aims at reducing the reliance on expensive carbon sourced generation such as Gas and Coal.

What does this mean for me?

The Energy Bills Discount Scheme (EBDS) replaced the Energy Bill Relief Scheme (EBRS) on the 1st of April 2023. It is designed to give all non-domestic customers, including the voluntary sector (such as charities) and the public sector (such as schools and hospitals) access to a phased in maximum discount when the customer’s wholesale cost exceeds the defined thresholds. This lasts for 12 months until 31st of March 2024 and applies to contracts that were put in place on or after 1st of December 2021 and non-contracted arrangements. Those companies that are classed as Energy and Trade Intensive Industries (ETII) will receive a more attractive discount once applied for. As with the EBRS, energy suppliers will automatically apply these standard discounts. Although the levels of assistance are lower and are based on a high wholesale cost, the price of Gas and Electricity is considerably lower than levels seen in 2022. Please see our Blog for more details.

From 1st of April there were further changes to the way some charges are calculated, under the Targeted Charging Review. Energy suppliers can choose whether to fix Electricity contract costs, pass them through or leave that decision until a later date. This does allow for the possibility of a review of the Transmission charges, and Balancing in some fixed price Electricity contracts, where BSUoS was previously recovered through the Wholesale element.

Indigo Swan will be working closely with energy suppliers to help all our customers through this time of uncertainty.

Please contact us on 0333 320 0475 to discuss options or to get a latest update.

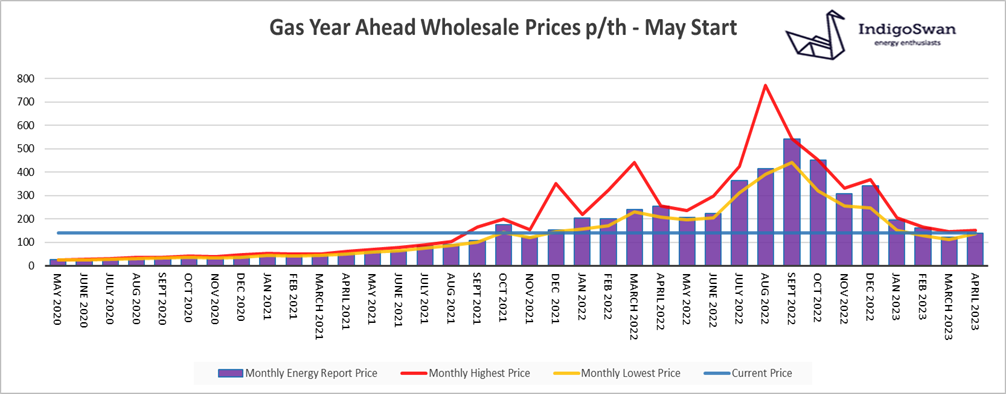

Gas market overview

On the 5th of April, the Gas Year Ahead Wholesale cost was 139.82p/th, up from 122.30p/th in last month’s report and 45% less than 2022. Prices fell as low as 114.44p/th during the period.

This increase is largely due to the below seasonal norm temperatures in recent days and the additional and unexpected demands for heating. Despite this, UK and EU Gas Storage levels remain high. Large numbers of LNG shipments continue to be made to the UK, some of which have been diverted from France, due to industrial action at their terminals. The US Freeport facility has reported that it is fully operational which should allow further shipments, as LNG continues to compensate for the reduced flows from Russia. The price being paid by Europe is higher than that by Asia, so there remains the potential for supplies to be diverted to China, as their economy grows after COVID restrictions.

The EU has a Gas price cap in place to help avoid the high costs seen in 2022, which will also create an element of price stability in the UK due to the global relationships for energy prices.

The recent increases are a demonstration that there remains the possibility of price volatility from cold spells, the war in Ukraine and Gas shipments heading away from Europe, as well as any unexpected global events which may impact on supplies.

Let us know if you would like us to research your options for 12, 24 and 36 month contracts.

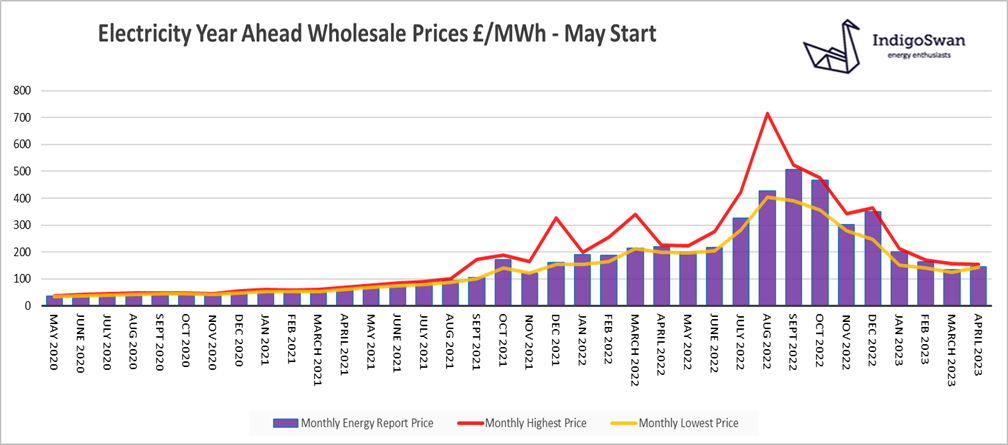

Electricity market overview

On the 5th of April, the Electricity Year Ahead Wholesale cost was £145.60/MWh, up from £133.50/MWh in last month’s report and 34% less than 2022. Prices fell as low as 125.74p/th during the period.

March saw an increase in Electricity demand and in the amount of expensive Gas that was required for generation, at 36%, compared to 35% in February. The contribution from Wind was down at 25% and has fallen further so far in April to just 20% and there remains considerable uncertainty as to the levels for the remainder of the month.

With one of the last UK Coal generators closing in April, which had been used as a backup supply for times of peak demand, this underlines the importance of a diverse range of new energy sources, to compensate for the erratic nature of renewable supplies. The return of French Nuclear generators has contributed to large Imports, via the interconnectors with the continent, despite additional safety concerns. For much of 2022 we Exported more than we Imported and there remains the risks that French strikes and maintenance may disrupt these supplies.

The National Grid has mechanisms in place to help avoid power shortages and has taken additional steps to make generation available on demand. These measures do come at a cost premium, in the form of higher third-party charges within bills, but provide an element of stability to prices which otherwise may react even more dramatically.

Let us know if you would like us to research your options for 12, 24 and 36 month contracts.

If you enjoyed reading this blog why not try one of our others: