Headlines:

- Very high Gas and Electricity Wholesale costs.

- Potential for further disruption to Gas imports from Russia.

- EU Gas Storage levels are an improved 70% full, compared to 57% last year.

Energy Overview

As of the 2nd of August, Gas and Electricity Year Ahead Wholesale costs were higher, when compared to last month’s report. The Oil price remains at $101 per barrel, although it did peak at $110 over the last month.

Prices continue to increase as Russia takes measures to reduce Gas supplies into Europe, creating concern and instability. The assumption is that this is in response to sanctions and the assistance being provided to Ukraine.

The Nord Stream 1 Gas pipeline is operating at just 20% of capacity due to maintenance, which is widely thought to not be required. A growing number of countries have had Gas supplies cut off as they refuse to pay in roubles, the latest being Latvia. EU member states are very aware that Russia could potentially stop flows of Gas coming into Europe at any time and so have introduced a voluntary requirement to reduce Gas consumption by 15% up until March 2023. This will become mandatory should the situation deteriorate, which may bring in the enforced rationing for industries, to preserve supplies for the likes of domestic heating and hospitals. EU Gas Storage levels are currently 70% full, with a target of 80% by November.

The Met Office forecast suggests we will see above seasonal norm temperatures at times in August, with little mention of strong winds, which would mean the continued high use of Gas for Electricity generation.

What does this mean for me?

Wholesale prices for 2022 remain very high when compared to recent years. Prices for 2023 and 2024 show better value. Generally, the Wholesale element makes up in the region of just 40% of the total cost of an Electricity bill and 60% for Gas, but these percentages are currently much higher, estimated in excess of 60% and 80%.

Increasing third-party costs are noticeable in Electricity contracts. These include Transmission, Distribution, Balancing and government policy levies, which ensure we have enough energy to meet demand and provide investment.

Over the next year, the way these charges are calculated will change, under the Targeted Charging Review. Energy suppliers can choose whether to fix Electricity contract costs, pass them through or leave that decision until a later date. This does allow for the possibility of a review of the Transmission and Balancing charges in some fixed price Electricity contracts, as the pricing method is due to change from April 2023.

Indigo Swan will be working closely with energy suppliers to best help all our customers through this worrying time, where there is a great deal of uncertainty as to developments in Ukraine and the impact they have on energy costs. Some suppliers are still hesitant to provide contract offers and they may be withdrawn at short notice.

We would advise looking at your options for contracts ending 2022. There is an opportunity to contract for two or three years to dilute the impact of the higher short-term costs.

Please contact us on 0333 320 0475 to discuss options or to get a latest update.

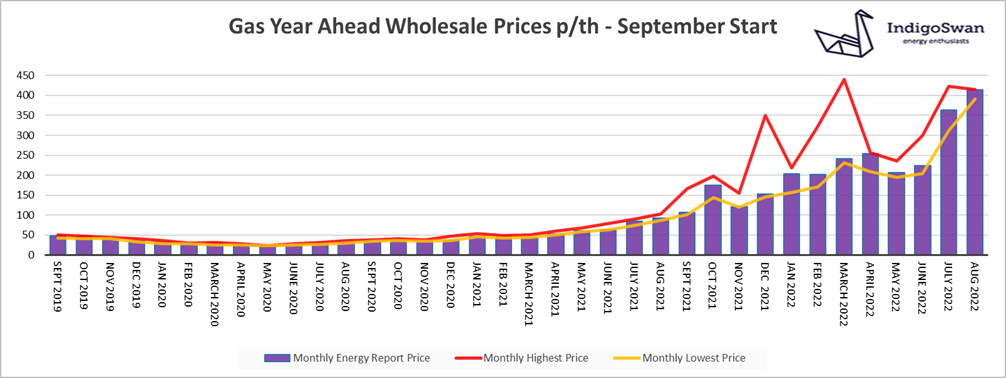

Gas market overview

On the 2nd of August, the Gas Year Ahead Wholesale cost was 414.27p/th, up from 363.23p/th in last month’s report and 353% higher than 2021. Prices for 2023 and 2024 are considerably lower.

Energy markets are very focused on Gas deliveries to Europe for this winter. With Russia providing in the region of 40-45% of supplies and few options of sourcing from elsewhere, there is the potential for considerable disruption and economic damage, should Russia choose to further reduce or cut off flows. In response, the EU has set a target that Storage levels should be 80% full by November, which are currently at 70%. They have also set a voluntary 15% reduction in Gas consumption up until March 2023, which may become mandatory, requiring state intervention to restrict Gas use by non-essential users, such as targeted industries.

LNG supplies into Europe have been high, which has provided some relief, but with a global competition for shipments and a limited capacity to receive and process them, they remain an unreliable and expensive option.

The use of Gas for generation remains very high, adding an additional pressure. This is due to a low Renewables contribution and supply issues across Europe, which includes the closure of a number of Nuclear reactors in France due to safety concerns.

Let us know if you would like us to research your options for 12, 24 and 36 month contracts.

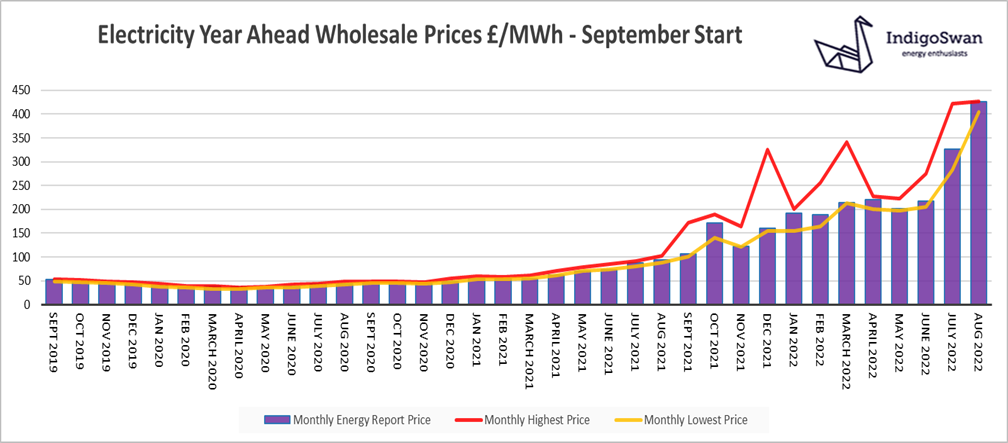

Electricity market overview

On the 2nd of August, the Electricity Year Ahead Wholesale cost was £426.60/MWh, up from £325.83/MWh in last month’s report and 354% higher than 2021. Prices for 2023 and 2024 are considerably lower.

Electricity prices continue to be driven by the high cost of Gas generation, which accounted for 46% of supplies in July. Wind’s contribution fell to just 16%, the lowest since September 2021. This reliance on Gas and the concern that supplies may be stopped by Russia, is likely to create volatility until political tensions ease.

Although we have an increased connectivity with Europe through Interconnectors, which allow Electricity to be imported or exported, the generation issues specifically in France, with the closure of a number of Nuclear reactors has meant a significant reduction of supplies coming into the UK. In July, these Interconnectors contributed just 5% compared to 15% in July 2021.

The National Grid has mechanisms in place to secure additional supplies or reduce demand. These do come at a cost premium, in the form of higher third-party charges within Electricity bills, but provide an element of stability to prices which otherwise may react even more dramatically.

Let us know if you would like us to research your options for 12, 24 and 36 month contracts.