Headlines

- Below seasonal norm temperatures.

- LNG shipments may be heading back to Europe.

- Low Wind contribution.

Energy Overview

As of the 2nd of February, Gas and Electricity Year Ahead Wholesale costs are virtually unchanged, when compared to last month’s report.

The price of Oil has steadily increased over the last month, from $53 to $57 a barrel, the highest since February 2020. The Oil production cuts, immunisation programmes to combat the coronavirus, as well as more vaccines, are the main reasons for this. However, growing numbers of cases, lockdowns and vaccine availability are preventing the Oil price going too high.

January saw a heavy reliance on Gas for Electricity generation and a high heating demand, during the spells of below seasonal norm temperatures. Although Gas Storage levels have decreased, they are at, 2019 / 2020 levels.

Wind generation was down in January, meeting just 19% of the very high monthly Electricity demand. This meant a greater use of Coal generation at over 4% and Gas at 43%. There were some instances of warnings being raised of potential supply issues.

The Met Office forecast for the next month suggests a high chance of colder weather with snow for parts of the UK. There also appears to be less potential for a good Wind contribution, which may add pressure to prices.

What does this mean for me?

Wholesale prices for 2021 are high when compared to 2020, but are comparable to 2019 and lower than 2018. Prices for 2022 and 2023 show much better value. It should be remembered that the Wholesales element makes up in the region of just 40% of the total cost of an Electricity bill and roughly 60% for Gas.

Increasing third-party costs are noticeable in Electricity contracts. These include, Transportation, Distribution, and government policy levies. These ensure we have enough energy to meet demand and provide investment.

Over the next few years, the way some of these charges are calculated will change, under the Targeted Charging Review. Full details are not yet available. Initially the first change to Transportation costs was due April 2021, but with delays issuing price guidelines to energy suppliers, this has been postponed until April 2022. The planned change to Distribution charges is still set for April 2022. This does mean that the expected opening of some fixed priced contracts should not take place until 2022.

There has been recent pressure on 2021 prices due to higher demand and supply concerns, so there is potential for prices to fall, but this is by no means certain. With much better value in longer term contracts, we would advise looking at your options for contracts ending 2021. Be aware that suppliers have tightened their credit requirements and reduced their risk appetite. Good forward contract options can still be negotiated.

Please contact us on 0333 320 0475 to discuss options or to get a latest update.

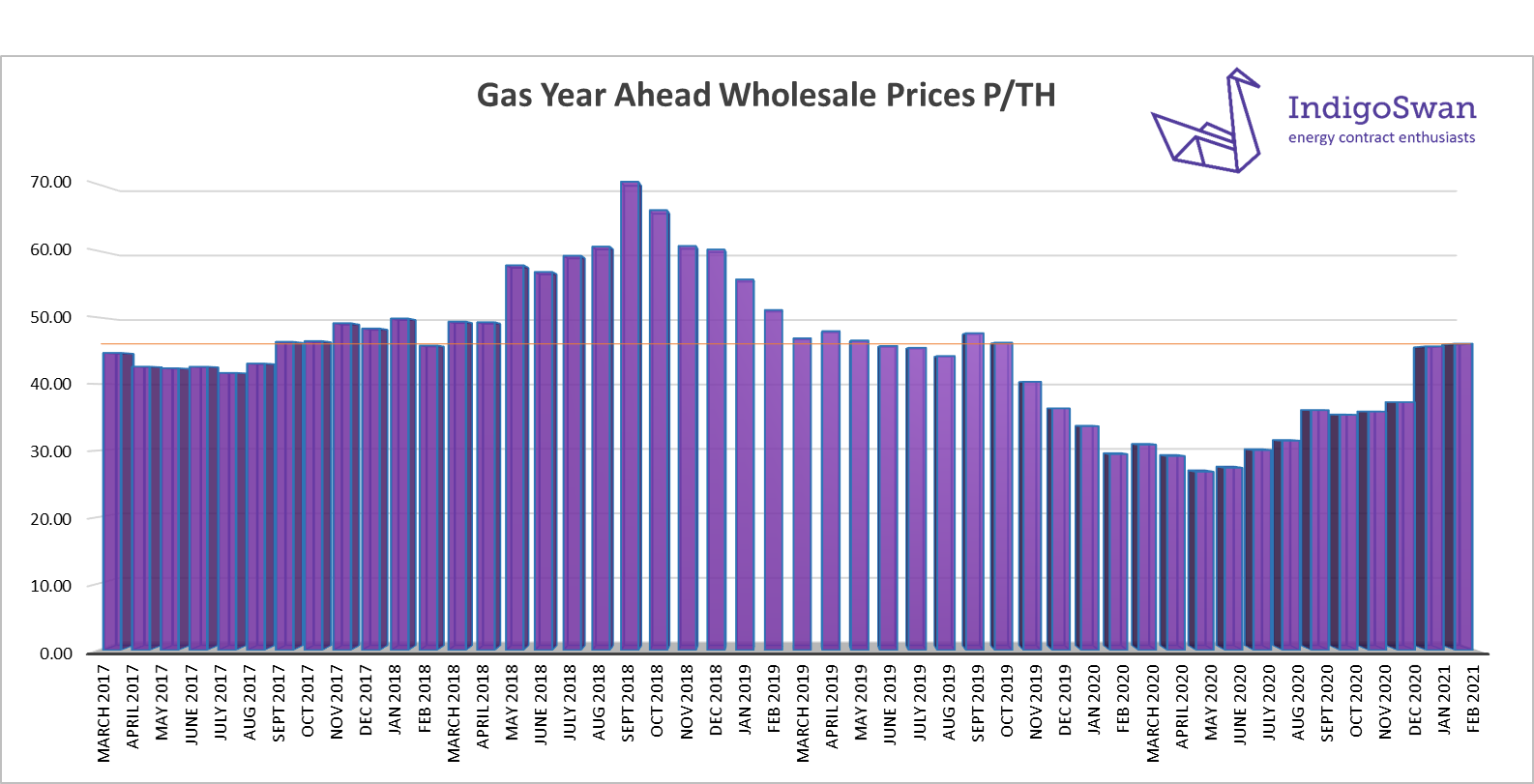

Gas Market Overview

On the 2nd of February, the Gas Year Ahead Wholesale cost was 46.05 (p/th), from 45.65 (p/th) in last month’s report and 56% higher than 2020.

The high heating demand placed a burden on Gas supplies in January as did the 43% contribution towards Electricity generation, due to lower Renewables and an increased Electricity demand.

These pressures did see the price of Gas reach over 50 (p/th) for a year ahead contract.

LNG deliveries have been heading to Asia due to a cold spell. With milder conditions and a falling price, it is hoped that more shipments will come to Europe, helping to support Storage levels.

With the colder weather on the way, this does impact on prices. The industry considers all aspects of supply and demand, with the resulting level of confidence, being translated into a lower or higher Wholesale cost.

Let us know if you would like us to research your options for 12, 24 and 36 month contracts.

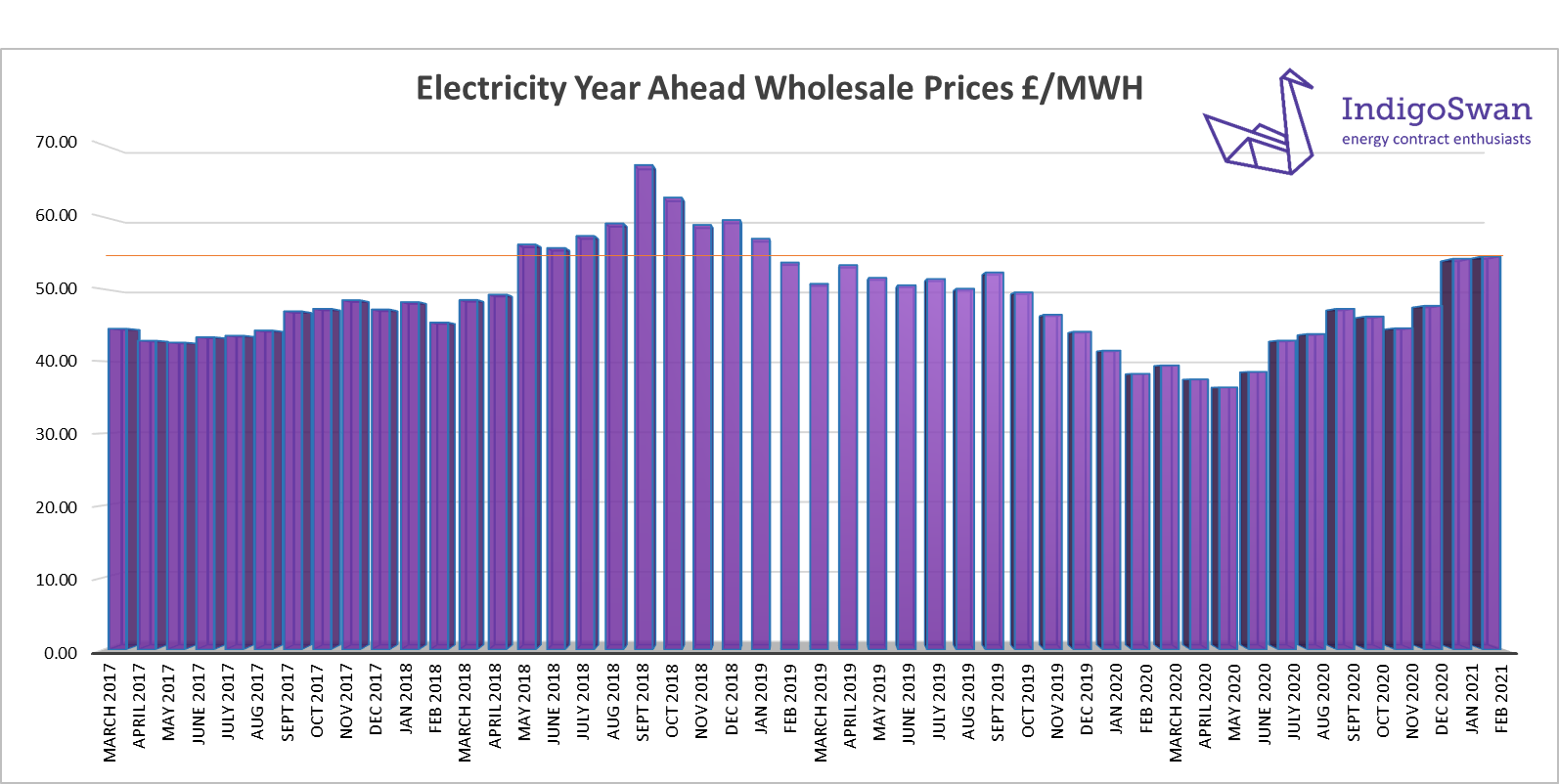

Electricity Market Overview

On the 2nd of February, the Electricity Year Ahead Wholesale cost was 54.54 (£/MWh), from 54.21 (£/MWh) in last month’s report and 43% higher than 2020.

January saw a high Electricity demand and a reduced combined contribution from Wind and Solar, of less than 20%.

In response, Gas generation increased to 43% from 39% in January, and Coal 4% from 2%. These more expensive forms of generation helped increase the Electricity Wholesale price.

The recent cold weather and the concern that Gas supplies may be tight over the coming months, has meant that 2021 Wholesale prices have risen, exceeding 58 (£/MWh) for a year ahead contract in January. Prices have eased slightly, but there remains the potential for volatility, with more cold weather on the way.

The industry remains confident that it can cope with changing demand patterns. Warnings were issued in January of potential tight supply margins, but the mechanisms the National Grid has in place, secure additional generation or reduce demand. These mechanisms do come at a cost, in the form of higher third-party charges within Electricity bills, but do provide an element of stability to prices which otherwise may react far more dramatically.

Let us know if you would like us to research your options for 12, 24 and 36 month contracts.