Headlines:

- Gas and Electricity Wholesale prices are lower than last month

- A more positive outlook this winter compared to last

- EU Gas Storage levels are a very high 84% full

Energy Overview

As of the 8th of January, Gas and Electricity Year Ahead Wholesale costs were lower than those in last month’s report.

The start of the year has seen prices fall to their lowest level in over two years, although they are still higher than what had been regarded as normal in 2020 and early 2021, prior to tensions with Russia.

Europe’s ability to cope with the additional supply demands for the remainder of the winter is looking positive, as Gas Storage is high at 84% full, despite the current cold spell. Although stocks have fallen from 94% last month, they were just 55% in 2022 when there were fears that shortages could result in supply restrictions to customers.

The conflict in Gaza has yet to have a significant impact on Gas and Oil supplies, despite the attacks on shipping by supporters of Hamas. Shipments have largely continued to use the shorter route through the Red Sea and the Suez Canal, with a number of nations providing naval security. There is the potential that further developments in the region could result in price volatility.

With Gas frequently providing over 30% of Electricity generation and being a flexible source of supply, the power price follows Gas. The opening of another Interconnector with Europe further reduces our reliance on carbon-based generation.

What does this mean for me?

The Energy Bills Discount Scheme (EBDS) replaced the Energy Bill Relief Scheme (EBRS) on the 1st of April 2023. It is designed to give all non-domestic customers, including the voluntary sector (such as charities) and the public sector (such as schools and hospitals) access to a phased in maximum discount when the customer’s wholesale cost exceeds the defined thresholds. This scheme lasts for 12 months until 31st of March 2024 and applies to contracts that were put in place on or after 1st of December 2021 and non-contracted arrangements. As with the EBRS, energy suppliers will automatically apply these standard discounts. The levels of assistance are less generous, but the price of Gas and Electricity is considerably lower than 2022. Those companies that are classed as Energy and Trade Intensive Industries (ETII) and Heat Networks, had to apply in July 2023 to receive a more attractive discount.

Since April 2023, customers may have seen higher Standing Charges on their Electricity invoices. There have been changes to the way some industry charges are calculated, under the Targeted Charging Review. This move is part of an attempt to recover more Electricity costs, such as Transmission and Balancing, through fixed fees. In theory this should give both the customer and the industry a more accurate way of managing finances.

Indigo Swan are working closely with energy suppliers to help all our customers understand and manage these changes.

Please contact us on 0333 320 0475 to discuss options or to get a latest update.

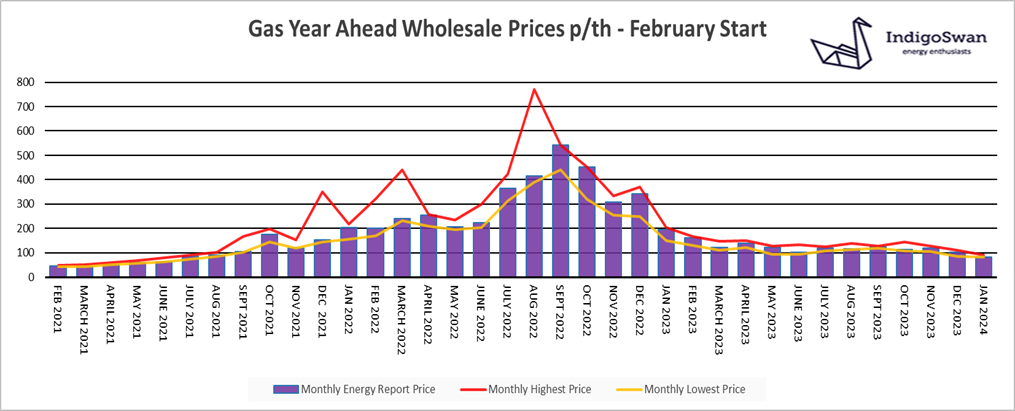

Gas market overview

On the 8th of January, the Gas Year Ahead Wholesale cost was 83.34p/th, down from 103.26p/th in last month’s report and 57% less than 2023.

There has been a decrease in EU Gas Storage, now at 84% full compared to 94% last month. The position is a positive one and some way from the concern that was built into prices in 2023, when fears of a very cold and prolonged winter, could have seen restrictions on supplies.

The low Storage capacity in the UK means we are reliant on LNG deliveries through the winter. This is also now the case for Europe due to reduced Gas flows from Russia. There was a concern that the attacks on ships through the Red Sea could see inflated Oil and Gas prices, but with little disruption, that has not materialised. Large numbers of deliveries continue to arrive from a range of sources, including the US.

Below seasonal normal temperatures this week will likely see an increase in Gas demand for heating and with businesses returning following the holidays, we would also expect more use of Gas to generate Electricity.

The current cold spell in Europe did initially have an impact on prices, but with the positive supply position, there is the potential for further decreases.

We would advise discussing your options for contracts ending early 2024 and closely monitoring those further out.

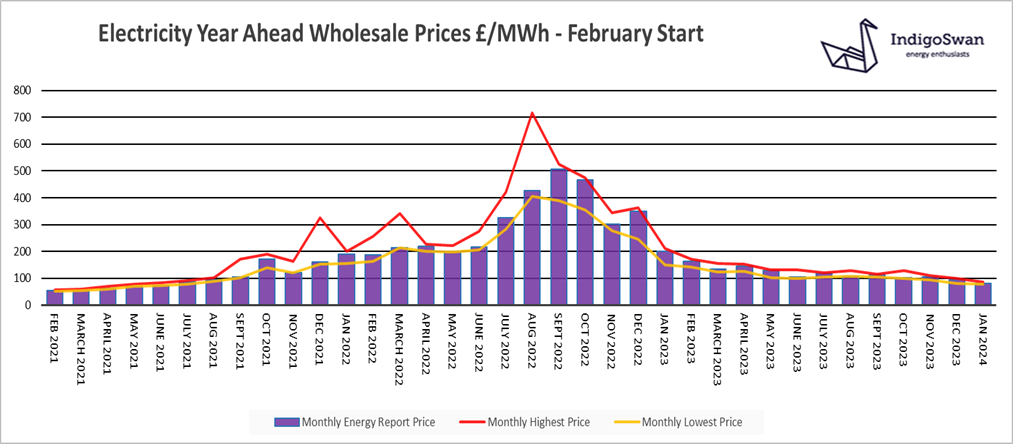

Electricity market overview

On the 8th of January, the Electricity Year Ahead Wholesale cost was £79.90/MWh, down from £93.65/MWh in last month’s report and 60% less than 2023.

As expected, Electricity use increased in December, although it was in the region of 5% lower than 2022, likely to avoid high energy costs and to reduce emissions. At some point the national demand will start to increase as, for example, more cars need to be charged and Gas heating is replaced by ground source heat pumps.

Gas provided 29% of generation, down from 34% in November, largely due to an increase in Wind at 35% of supplies. Over the last week this has fallen to 22%, but since the 29th of December we now have the additional Viking Link Interconnector with Denmark, which has helped contribute 14% of supplies from Europe. This is another tool to help us balance our Electricity network and avoid the need to build power stations and source more from carbon fuels, just to react to short term peaks.

The Demand Flexibility Service also helps reduce stress on the network over the winter period, by incentivising using less Electricity. This is indirectly replacing much of the benefit of Triads, which still exist in some regions but with a reduced benefit on previous years, as industry costs are now largely recovered through fixed fees.

We would advise discussing your options for contracts ending early 2024 and closely monitoring those further out.

If you enjoyed reading this blog why not try one of our others: