Headlines:

- Gas and Electricity Wholesale prices are lower than last week

- EU Gas Storage levels are a healthy 80% full

- LNG deliveries continue to arrive in Europe

Energy Overview

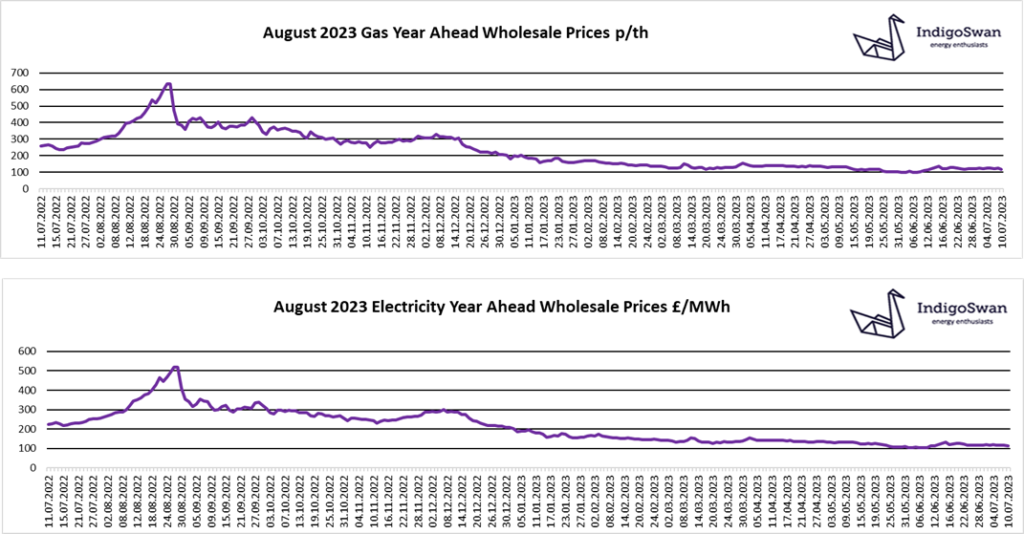

Since our last Energy Report, Gas and Electricity Year Ahead Wholesale prices are lower.

Prices are reflecting the more positive outlook for Gas supplies this winter, when compared to the considerable concern last year. With EU Gas Storage levels at 80% full against a target of 90% by November, the expectation would be that their very large Storage capacity should be ready to meet the additional seasonal demand. Competition from Asia for LNG deliveries has yet to have an impact on shipments to Europe, however that position could change. Europe is also still receiving Gas from Russia despite the well reported closure of Nord Stream 1 and sanctions which included Nord Stream 2. Should there be further supply disruptions and indications of colder than average temperature, this may add price pressure.

The cooler temperatures over the last week have reduced Electricity demand, due to less air conditioning. The contribution from Gas for generation was lower at 31% whilst Wind was up to 21% from a more recent average of 17%. A small amount of Coal was also required.

We continue to see large daily % swings in Wholesale prices for no clear reason, which underlines the degree of uncertainty and nervousness for this coming winter. Prices are in the region of 70% lower than July 2022, although there is still a premium against 2020 and early 2021 but it is generally considered unlikely that we will see those low levels for some time. Therefore, we would advise discussing your options for contracts ending in 2023 and early 2024 with Indigo Swan.

If you enjoyed reading this blog, why not try one of our others: