Headlines:

- Gas and Electricity Wholesale prices are lower than last week

- EU Gas Storage levels are a very high 91% full

- Global events may create further price volatility

Energy Overview

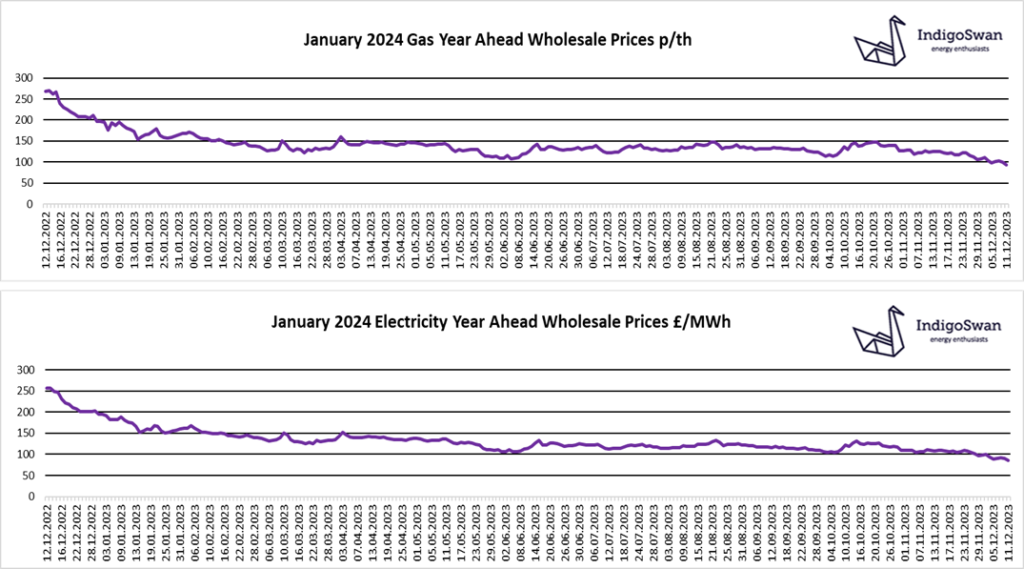

Gas and Electricity Wholesale costs are lower than last week.

We have seen a 9% reduction in Year Ahead Wholesale prices since last week’s report which illustrates the growing confidence felt by the energy industry and markets. EU Gas Storage is still above the level set for the start of November, from when it was expected that the colder temperatures and a higher heating demand would see Gas withdrawals. At 91% full, Europe should have more than enough Gas this winter, unless there is either a drop in supplies or a significant period of higher than usual demand. LNG deliveries have increased once more, providing crucial Gas as a replacement for the lower flows from Russia.

Over the last week, Gas has provided the most generation at 35%, meaning Electricity prices tracked Gas very closely. The contribution of Wind was up slightly at 31%, whilst Interconnectors provided a low 8% compared to 13% in November. The Demand Flexibility Service continues to help reduce Electricity demand at peak times rather than having to rely so heavily on the likes of Coal to generate for short periods, removing some of the strain on the network. Government schemes aim to prevent tight supply margins, power cuts and give the industry confidence which helps ease prices.

There is the potential that any event that impacts on the confidence in the delivery of energy supplies to meet demand could have a big impact on prices this winter. To manage risk, Indigo Swan are advising customers with contracts that end early 2024, to engage with us to review their positions.

If you enjoyed reading this blog, why not try one of our others: