Headlines:

- Gas and Electricity Wholesale prices are higher than last week

- Potential supply issues are adding pressure to prices

- EU Gas Storage levels are a positive 93% full, although lower than last year

Energy Overview

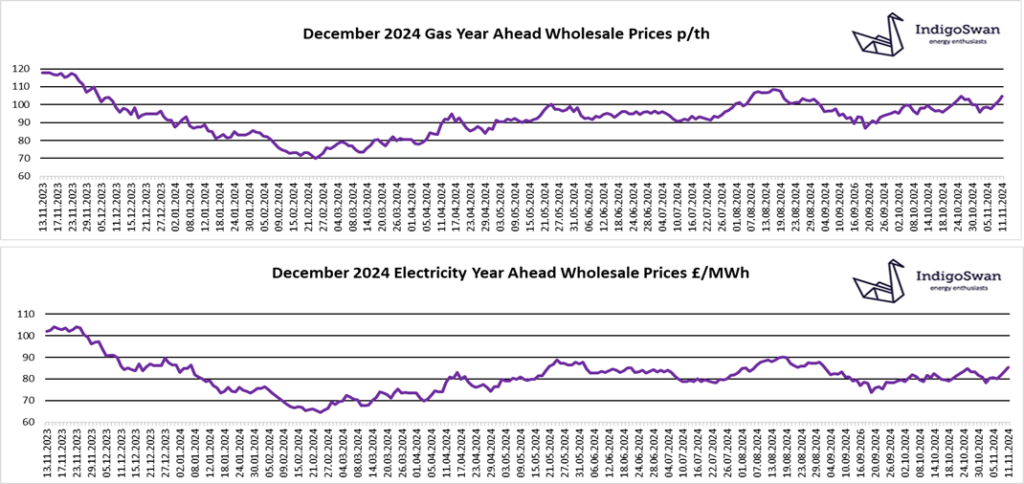

Gas and Electricity Year Ahead Wholesale costs are higher than last week. They show good value compared to most of 2021 / 2022 / 2023 when we saw most of the volatility, but are still double those in 2020, prior to Russia starting to withhold Gas supplies to Europe. Oil is slightly lower.

With cooler temperatures due here and in mainland Europe and with EU Gas Storage levels falling slightly to 93% full compared to 99% last year, energy markets have reacted. We may see the slower filling of Storage in 2025.

From January, Ukraine is ending the Gas transit arrangement with Russia, stopping some piped supplies entering Europe. Unless a solution is found, then Europe will become more reliant on LNG this winter to meet any additional demand. The focus for LNG deliveries has been Asia, where a price premium is being paid due to their unusually prolonged high temperatures and the need for air cooling. Europe is now in a much better position than when the Gas shortages started in 2021, as more infrastructure has been built to receive LNG shipments.

Although the threat of significant military strikes between Israel and Iran has eased, concern remains that an escalation may disrupt energy exports from the region.

Wind’s contribution to generation over the last week has been very low at just 13% as were imports from Europe at 12%, resulting in a very high use of Gas at 49%, which also has the added pressure from heating demand.

Some of the threats to supplies may not materialise and the more positive outlook could return, but due to the risks, we would encourage customers that have Gas or Electricity contracts ending in 2024 and early 2025, to discuss options with Indigo Swan and closely monitor the position.

If you enjoyed reading this blog, why not try one of our others: