Headlines:

- Gas and Electricity Wholesale prices remain similar to last week

- EU Gas Storage levels are a very positive 94% full

- Uncertainty as to price direction as we head towards the winter

Energy Overview

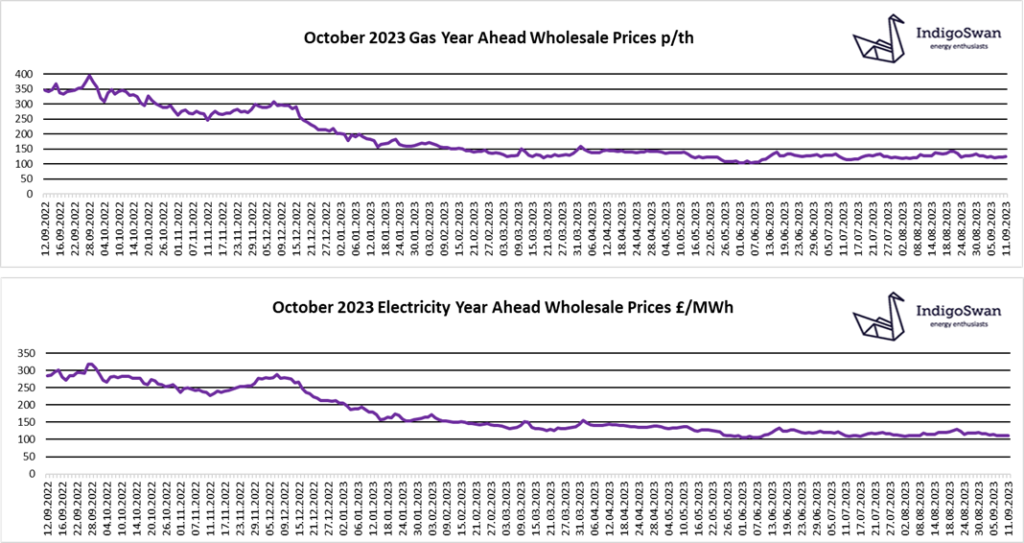

Gas and Electricity Wholesale costs are similar to those in last week’s report.

On the 8th of September, LNG workers in Australia started industrial action, which could impact on up to 7% of global supplies. Negotiations to find a settlement have so far failed, threatening prolonged disruption to deliveries to the Asian market. EU Gas Storage levels are 94% full, already exceeding the 90% target for November, limiting the strike’s impact on prices. However, this could change as we approach winter and competition increases for LNG from other sources, such as the US and Qatar. The Groningen Gas field is due to close by the 1st of October 2023, earlier than expected due to safety concerns. The Dutch government has said it could be utilised for one more year in the event of a Gas supply emergency.

Electricity prices continue to follow Gas, as it remains a major and reliable source of generation, at a very high 49% of supplies over the last week. The high temperatures meant increased Electricity demand for cooling and although there was improved Solar, Wind’s contribution was just 8%. This meant the use of Coal and underlines the importance of the 10% Imports from the continent via the Interconnectors.

There has been little price movement in 2023 compared to 2022, but they remain stubbornly high with little indication that this will change in the short term. Energy markets are overreacting to any industry supply issues which could potentially mean a period of volatility through the winter. For this reason, Indigo Swan are advising customers to review contracts that end in 2023 or early 2024.

If you enjoyed reading this blog, why not try one of our others: