Headlines:

- Gas and Electricity Wholesale prices are higher than last week

- EU Gas Storage levels are a very positive 89% full

- Uncertainty as to price direction as we head towards the winter

Energy Overview

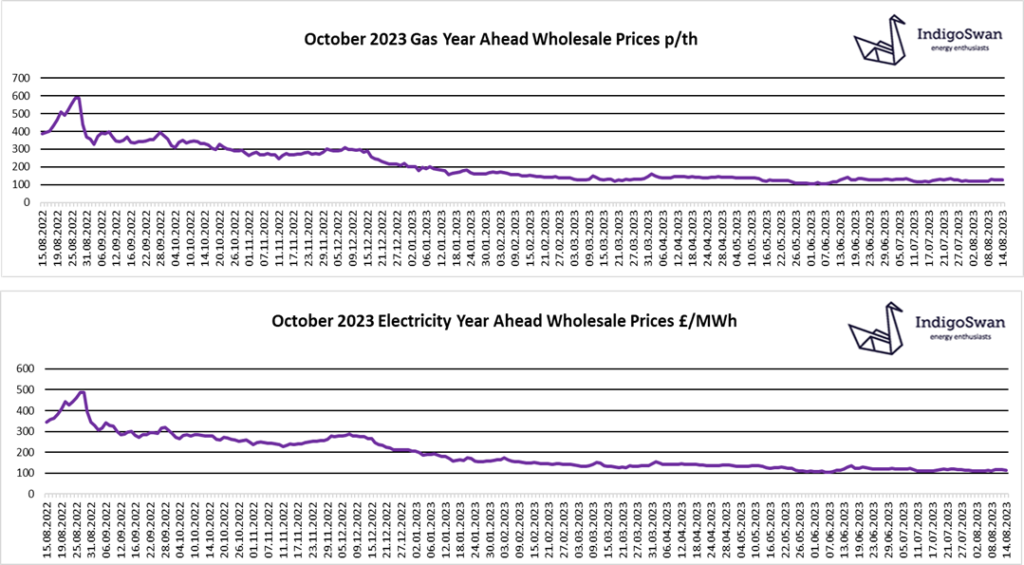

Since our last Energy Report, Gas and Electricity Year Ahead Wholesale prices are higher.

News that workers in Australia’s LNG industry may strike, caused a price spike last week, although there has been some price correction. Unless a resolution can be found, a vote will likely see industrial action, which would mean that many deliveries to Asia are impacted, putting pressure on other sources. LNG shipments continue to arrive in the UK and mainland Europe, helping to increase EU Gas Storage levels to 89% full and are likely to reach the 90% target two months early.

Despite the growing diversity of supplies, Gas remains a reliable source of generation which heavily influences Electricity prices. Over the last week Wind contributed 22%, down slightly from the previous week and Gas a higher 33%. The Interconnectors with the continent provided 14%, but these are potentially unreliable as French Nuclear reactors have a history of safety issues, as we saw in 2022, when some months we exported more than we imported. Hydro supplies from Norway through the North Sea Link can be impacted by low water levels.

Last week showed how nervous the energy markets are as we head towards the winter. Customer’s budgets are still being impacted by daily price swings which underlines the benefit of looking at the market for the best renewal options and either driving down the current supplier’s costs or switching. Indigo Swan are advising customers to review contracts that end in 2023 or early 2024 as there is a lack of clear price direction and the risk of increases as we head towards the winter, with possible supply and demand issues.

If you enjoyed reading this blog, why not try one of our others: