Headlines:

- Gas and Electricity Wholesale prices are lower than last week

- EU Gas Storage levels are a healthy 82% full

- Norway’s Nyhamna Gas processing plant came back online

Energy Overview

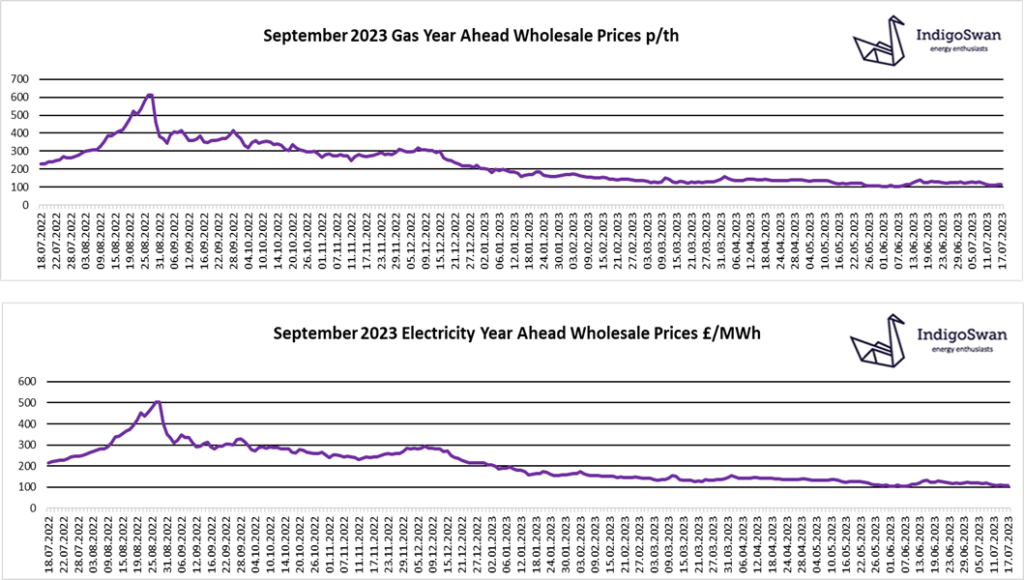

Since our last Energy Report, Gas and Electricity Year Ahead Wholesale prices are lower.

We are in a much more positive position than this time last year, when there were concerns that a shortage of Gas, due to reduced flows from Russia, may mean some restrictions in use through the winter. With the EU setting a target for Gas Storage levels to be 90% full by November and currently being a high 82%, energy markets are assuming supplies will be sufficient, unless there are further issues. Less LNG deliveries are being made to the UK due to our low Storage capacity, but they continue to head to Europe despite competition from Asia. Norway’s Nyhamna Gas processing plant came back online on Saturday following an extended outage, which had added some price pressure, as it also came with news that the Groningen Gas field would close October 2023, earlier than expected.

Electricity demand was slightly higher last week. Wind generation improved to 29% of supplies, whilst Gas remained similar at 32%. Imports from the continent were down as was the use of Coal, which is being retained for use during the winter, despite the wish to close.

Although the last week has seen a degree of price stability with a small downward trend, there remains the potential for large % swings with some nervousness remaining. Prices are in the region of 70% lower than July 2022, with a premium against 2020 and early 2021, but it is generally considered unlikely that we will see those low levels for some time. Therefore, we would advise discussing your options for contracts ending in 2023 and early 2024 with Indigo Swan.

If you enjoyed reading this blog, why not try one of our others: