Headlines:

- Gas and Electricity Wholesale prices are lower

- EU Gas Storage levels are 57% full

- Large numbers of LNG shipments to Europe

Energy Overview

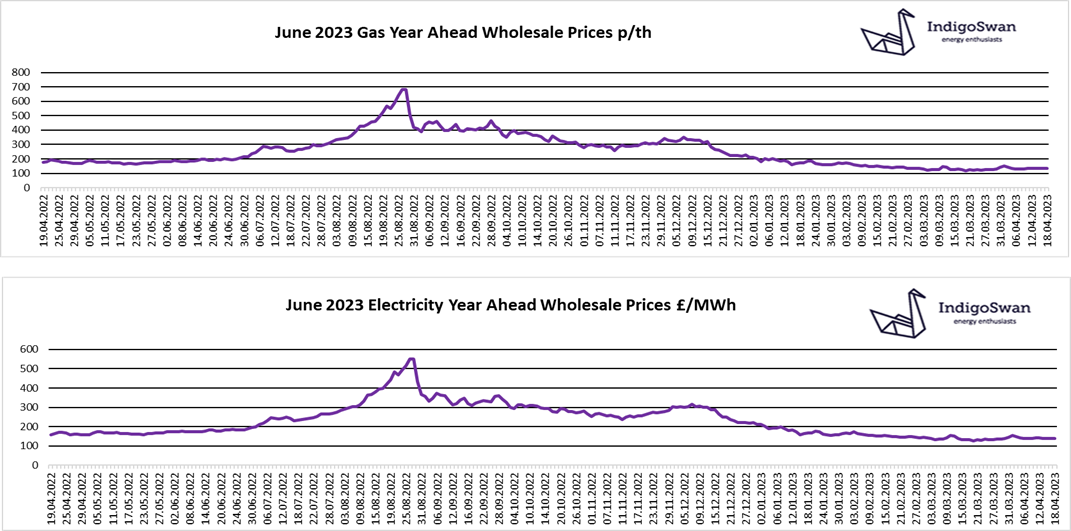

Since our last Energy Report, Gas and Electricity Year Ahead Wholesale prices are lower.

EU Gas Storage levels have increased to 57% full as the focus is on refilling stocks through the warmer months, in order to reach the target of 90% by November. News that the Chinese economy has grown faster than expected adds additional weight to the concern that some of the large number of LNG shipments that are arriving in Europe to replace the reduced Russian Gas flows, may head to Asia.

Wind’s contribution to generation has fallen to 19% over the last week, compared to the 25% – 30% seen in recent months. Electricity imports from the continent were 11%, compared to 15% in March. French industrial action is delaying maintenance work on their Nuclear reactors, which may impact on future flows. For much of 2022 we exported more Electricity than we imported, which added a price pressure. Gas power generation has increased at 39%, compensating for the lower winds and imports, with additional Gas demand for heating due to colder evenings.

As reported last week, there continues to be little price direction at the moment, following the large decreases over the last four months. The supply position is comfortable but there is continued concern that an unexpected event, which has not been factored into costs, could once again see increases. This was demonstrated by a cold spell, which helped to create upward price movement earlier this month. Prices are showing a premium on those seen in 2020 and early 2021, but with the possibility of an exaggerated market reaction and the pressure to put Gas into Storage, we would advise discussing your options for contracts ending in 2023 with Indigo Swan.

If you enjoyed reading this blog, why not try one of our others: