Headlines:

- Gas and Electricity Wholesale prices are higher than last week

- EU Gas Storage levels are a positive 74% full

- We continue to see low levels of price volatility

Energy Overview

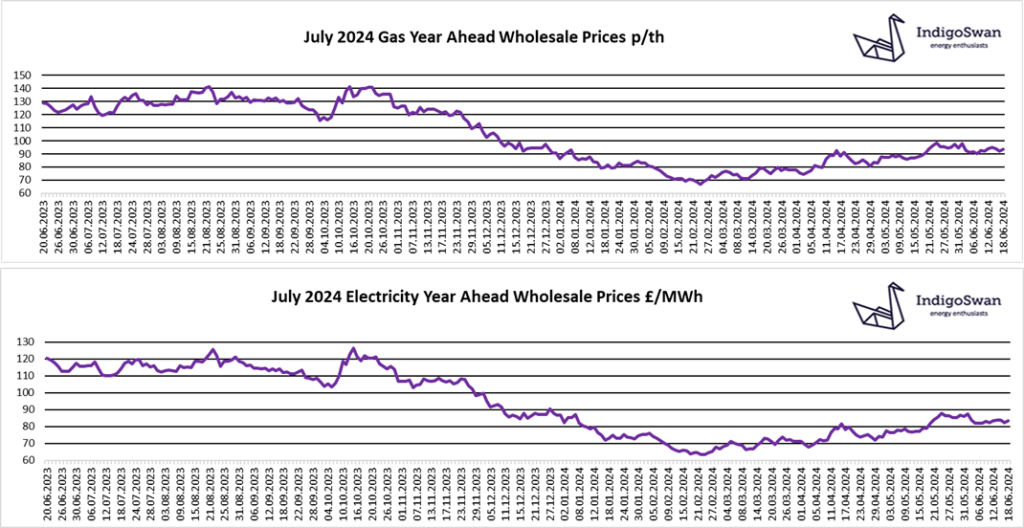

Gas and Electricity Year Ahead Wholesale costs are higher than last week, as the upward price trend continues, from the lows seen in February 2024. However, putting this into context, costs are still a fraction of those in 2021 / 2022 / 2023.

Gas flows from Norway have improved following the significant interruptions seen recently due to a fault. Prices initially increased, but soon fell back when it was confirmed the issue would be resolved within days. With Europe being heavily reliant on Norway for Gas due to the reduced flows from Russia, this event was a reminder how finely balanced the supply / demand relationship is and how interruptions have the potential to impact on energy prices. LNG shipments to Europe are lower due to a premium being paid by the Asian market.

EU Gas Storage levels are a high 74% full, which is comparable to last year, when stocks surpassed the target of 90% full by November. This is a big positive that gives confidence for winter 2024/2025, when demand will increase due to colder temperatures.

Over the last week we have seen a reduced contribution from Wind for Electricity generation, at 18%. With Imports from the continent via the Interconnectors down slightly at 21%, this meant a higher use of Gas at 25%.

We would encourage customers that have Gas or Electricity contracts ending in 2024, to discuss options with Indigo Swan and closely monitor the position.

If you enjoyed reading this blog, why not try one of our others: