Headlines:

- Gas and Electricity Wholesale prices are lower

- EU Gas Storage levels are 84% full

- Large numbers of LNG shipments to Europe

Energy Overview

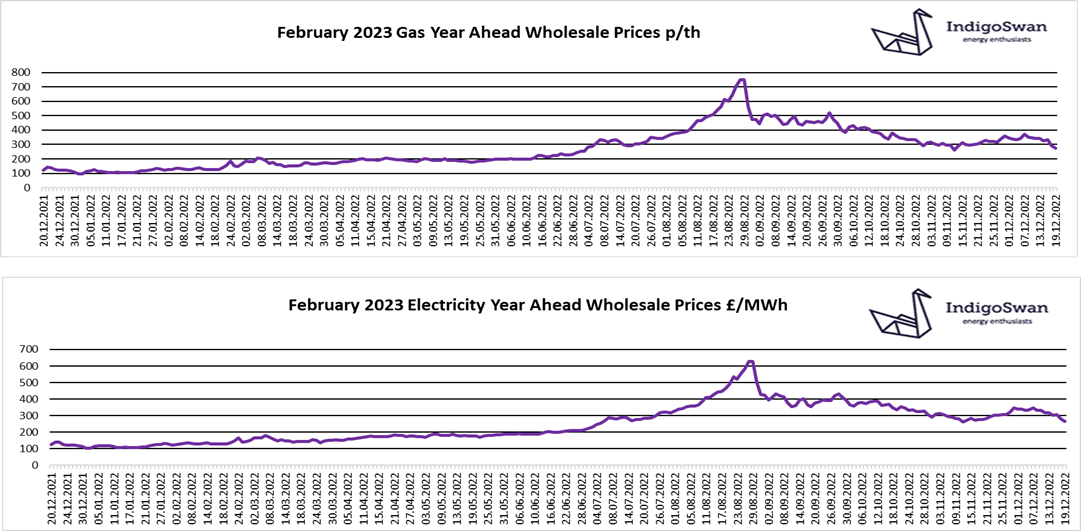

Since our last Energy Report, Gas and Electricity Wholesale prices are lower.

Costs for the remainder of 2022 and the first quarter of 2023 remain high. Although 2023 and 2024 show better value, there is still a premium, but does provide an opportunity to contract longer and reduce the shorter term % increases. The government’s Energy Bill Relief Scheme continues to provide a capped Wholesale cost for those that contracted from December 2021 and a discount for those not contracted. This started in October 2022 and runs until March 2023, and maybe extended for specific industries. Customers still need to monitor the markets for contracts from April 2023, when they may once again be fully exposed to costs.

The lower prices are reflecting the positive supply position due to a number of fundamentals. EU Gas Storage levels are 84% full, much higher than had been feared earlier in the year. Large numbers of LNG deliveries continue to be made to Europe with more due, with the likely resumption of shipments in late December, from the US Freeport LNG terminal. In the UK we are seeing above seasonal norm temperatures and a Wind contribution that was just 3% on the 12th, but more recently, 47%.

There remains some concern that with restrictions on the availability of Electricity imports from France due to the issues with large numbers of their Nuclear reactors, there could be very tight supply margins. However, the National Grid has secured additional generation and mechanisms to balance the network if required.

With the continued possibility of price volatility due to a great deal of uncertainty, we would advise looking at your options for contracts ending in 2023, having conversations with Indigo Swan about your specific requirements.

If you enjoyed reading this blog, why not try on of our others: